Proposal to Change Retirement Contribution Rules Sparks Debate

July 16, 2024 | Select Committee on Pension Policy, Joint, Work Groups & Task Forces, Legislative Sessions, Washington

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

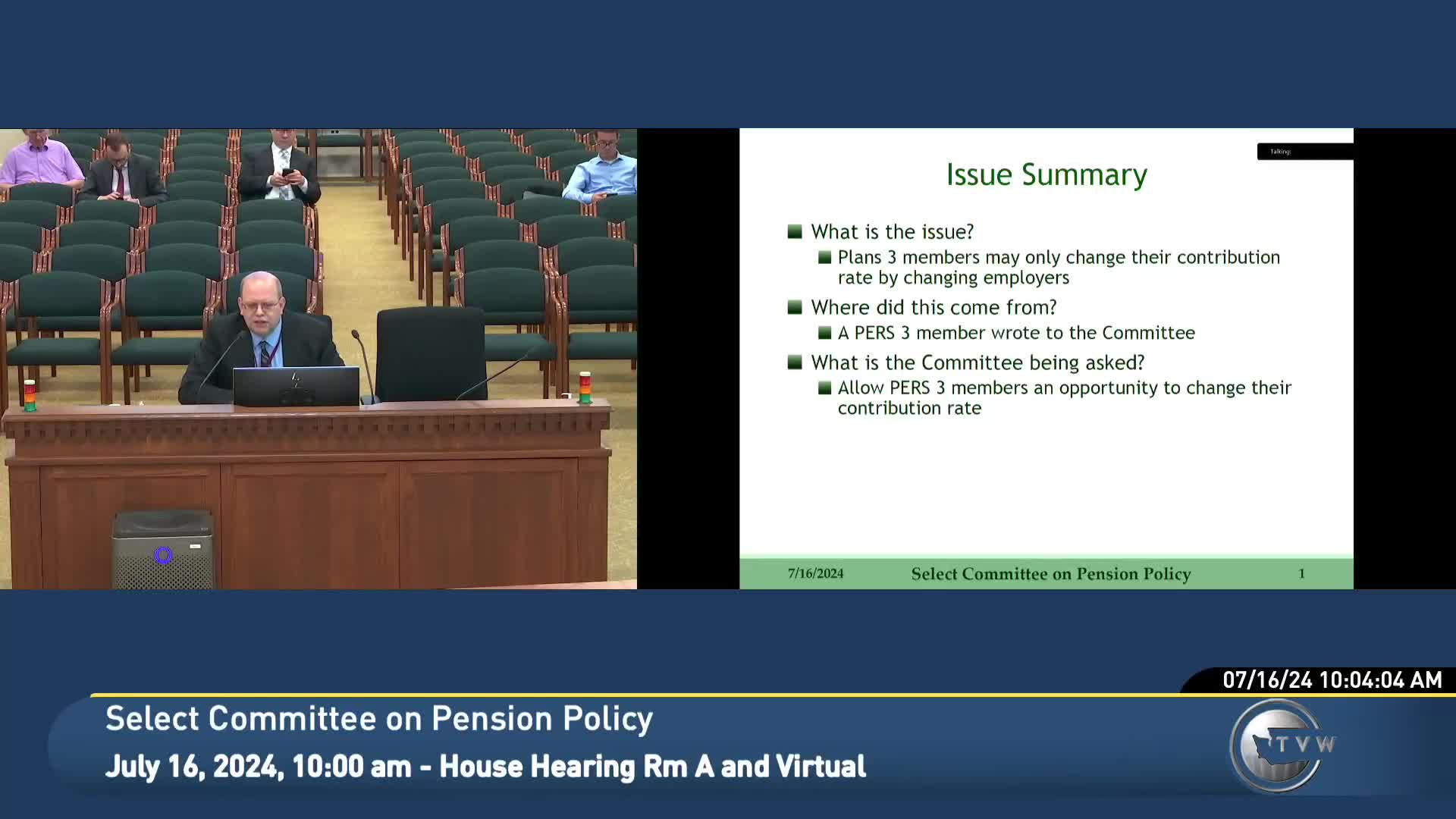

The meeting provided a comprehensive overview of PERS 3, which is a hybrid retirement plan combining both defined benefit and defined contribution components. Members initially select their contribution rates, which range from 5% to 15%, but once chosen, they cannot change these rates without switching jobs. This policy applies across various sectors, including public employees and teachers.

The discussion highlighted the tax implications of the plan, noting that Washington's retirement plans are tax-qualified under IRS regulations. This status allows members to make pretax contributions and defer taxes on investment earnings until distribution, providing significant financial benefits.

Historically, the IRS has disallowed annual member rate changes for PERS 3 and School Employees' Retirement System (SRS) 3 members, a decision that has remained consistent over the years. Although the Teachers' Retirement System (TERS) 3 initially had the option for rate changes, this was revoked after IRS review.

In response to the recent inquiry about the possibility of changing contribution rates without changing employers, tax counsel advised that such a change would likely jeopardize the plan's tax-qualified status. As a result, the committee is considering its next steps, which could include taking no action, requesting further briefings on the tax advice, or adding the issue to their work plan for future discussion.

The meeting underscored the ongoing challenges faced by PERS 3 members and the complexities of navigating IRS regulations in retirement planning.

View full meeting

This article is based on a recent meeting—watch the full video and explore the complete transcript for deeper insights into the discussion.

View full meetingSponsors

Proudly supported by sponsors who keep Washington articles free in 2025