Health plan costs surge as officials propose major increases

June 05, 2024 | Portage County, Wisconsin

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

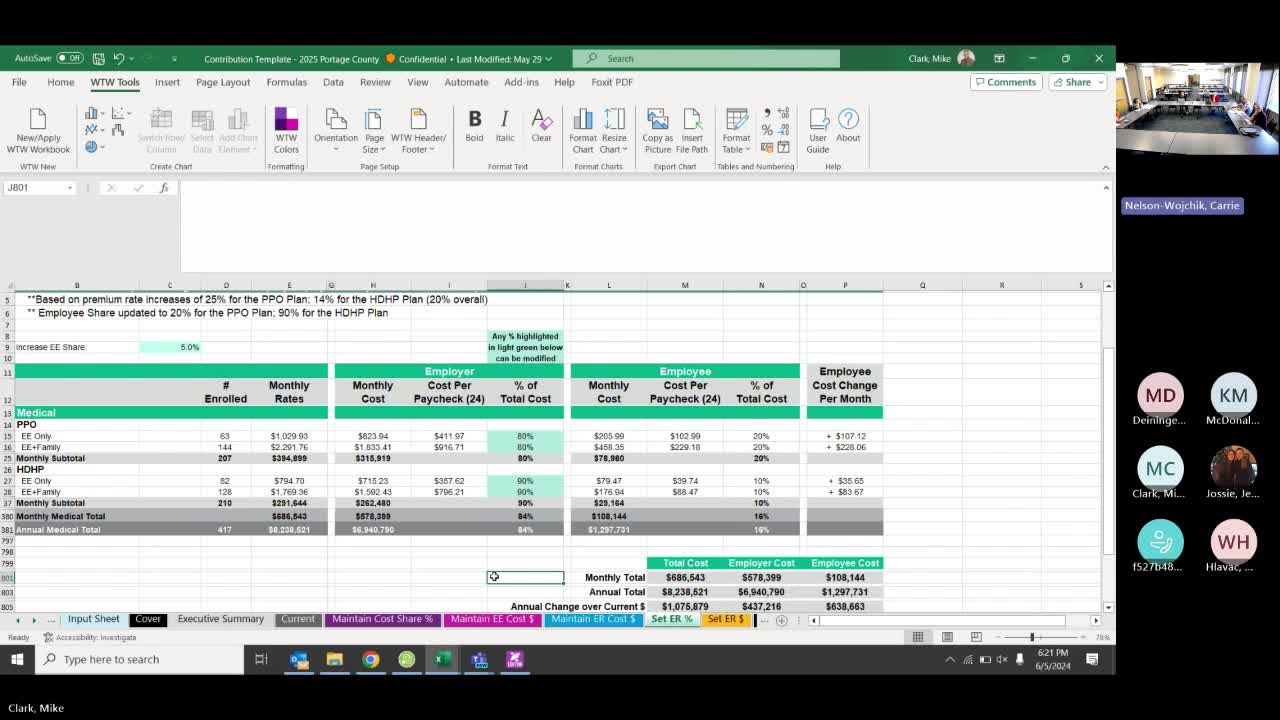

During the discussions, some members expressed concerns about the impact of these increases on lower-paid employees who rely on the PPO plan. One official noted the importance of ensuring that employees can afford necessary medications, highlighting the delicate balance between cost-sharing and employee welfare. There was also a suggestion to consider an even higher cost share for the PPO plan to incentivize employees to switch to the high deductible option, although this idea was met with caution due to potential financial strain on lower-income workers.

The committee acknowledged that the proposed changes would only bring the reserves to a minimum safety net of three months, prompting discussions about the need for ongoing monitoring of the financial situation. Officials emphasized the importance of making informed decisions based on data, particularly given the recent fluctuations in health care costs.

The motion to increase contributions was ultimately approved, with members agreeing to reassess the situation in the coming months. Additionally, a motion was made to maintain the Health Savings Account (HSA) contributions at the same level, although further details on this aspect were not fully discussed during the meeting.

Overall, the meeting underscored the challenges faced by the committee in balancing budgetary constraints with the health care needs of employees, particularly in a climate of rising health care costs.

View full meeting

This article is based on a recent meeting—watch the full video and explore the complete transcript for deeper insights into the discussion.

View full meetingSponsors

Proudly supported by sponsors who keep Wisconsin articles free in 2025