Article not found

This article is no longer available. But don't worry—we've gathered other articles that discuss the same topic.

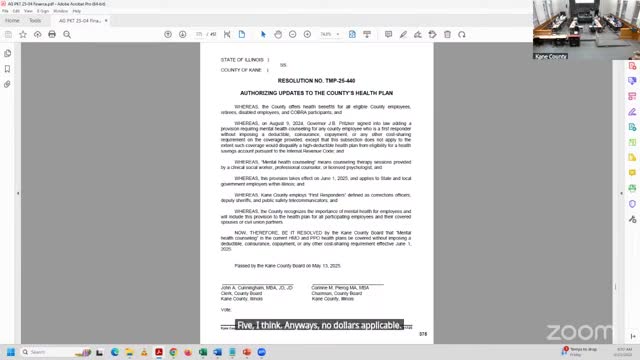

Kane County committee approves mental‑health coverage expansion to county health plan; debate over scope and cost

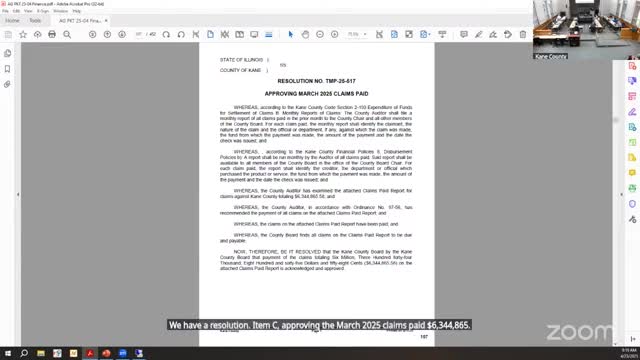

Finance director warns Kane County general fund gap could exhaust reserves by 2027

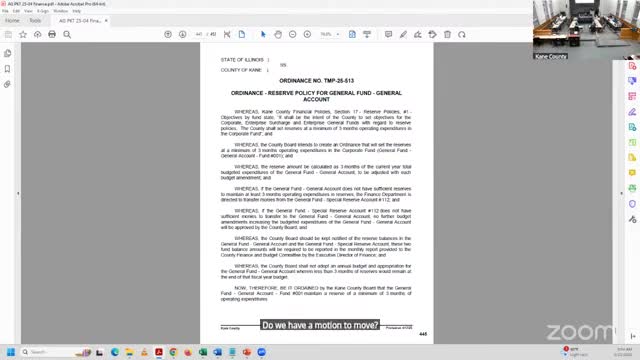

Kane County finance committee adopts 3-month general fund reserve ordinance amid concern over emergency access

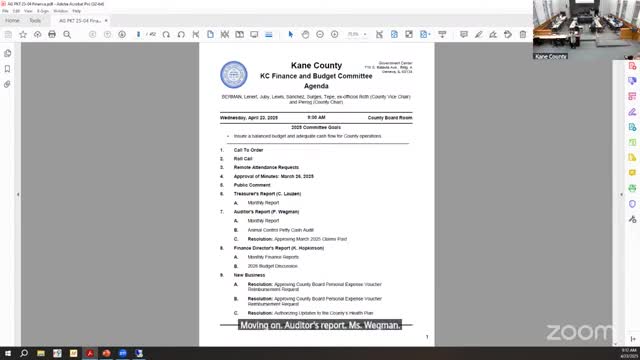

County auditor finds control gaps in Animal Control petty cash; recommends written petty‑cash policy and reconciliations