Article not found

This article is no longer available. But don't worry—we've gathered other articles that discuss the same topic.

Talent staff to add splash pad design costs and pursue OPRD grant for Chuck Roberts Park

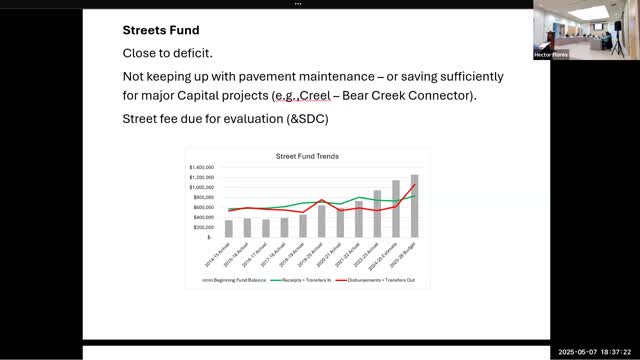

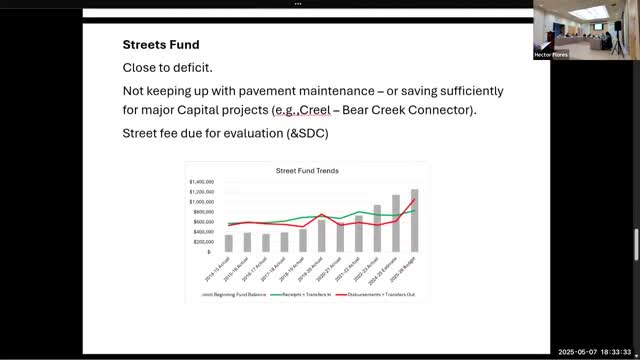

Talent's pavement program underfunded; committee told city is not collecting enough to maintain preventive maintenance

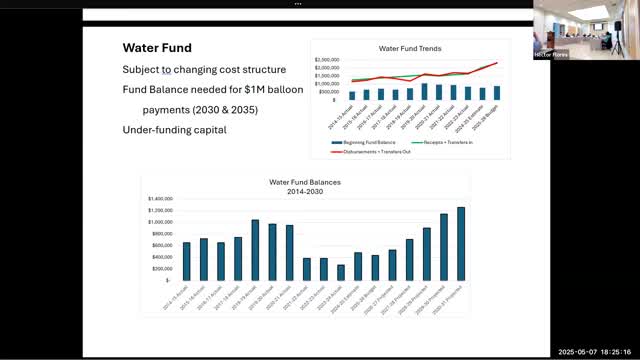

Budget officer flags two large water-fund balloon payments; staff to propose reserve options