Private markets drive strong returns; pension fund posts double‑digit year-to-date gains

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Consultants told the board the pension fund returned about 10–11% year to date, private equity distributions lifted private-market multiples, and private debt and real assets are maturing; private markets remain a focus in pacing and manager monitoring.

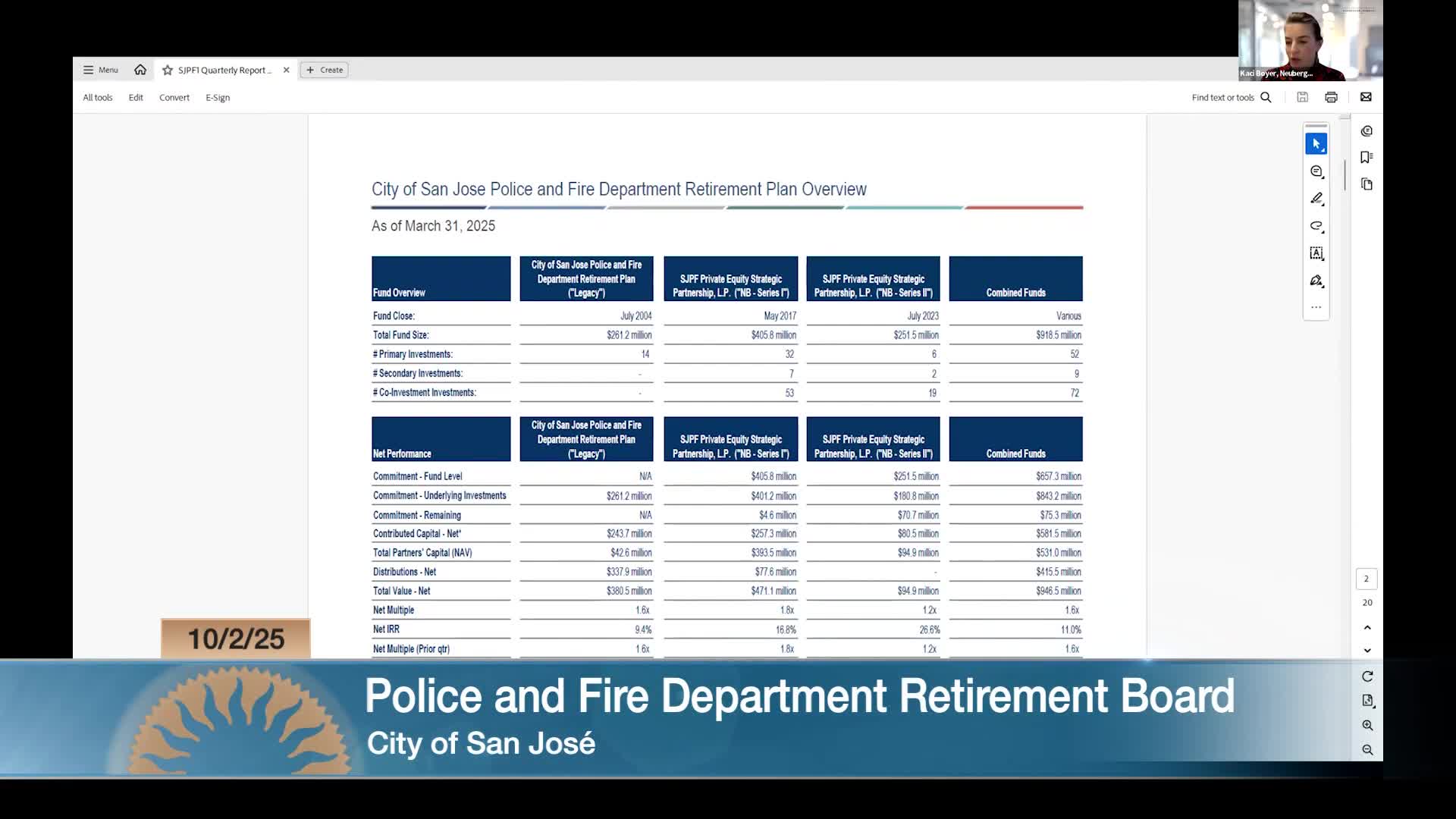

Investment consultants briefed the board Thursday on second-quarter private- and total-portfolio performance and said returns through the latest available quarter were strong. The pension plan’s total-fund returns were described by consultants as roughly 10% for the trailing 1‑year period and about 6% for the quarter ending June 30; the health care trust returned 11.1% over the trailing year. Private equity distributions since Q1 returned more than $10 million to the program and lifted reported net multiples in Series 1 and Series 2 portfolios, the consultant said.

Makita (consultant name per transcript) and staff highlighted that private equity realizations were returning to the market after a low-exit period and that a recent value-buyout fund sale of a health-tech company produced an ~8x return for that holding, contributing to distributions. Private debt and real assets showed signs of maturity: private debt contributions were now smaller than distributions and the private debt allocation was below target, while the real assets program had a 12% IRR and has become more geographically diversified.

On the total-fund side, consultants reported market-driven performance: global equities and emerging markets led gains in Q2 and Q3; the plan’s five-year annualized return ranked roughly in the mid‑30th percentile among peers and volatility was below peer medians. The consultants identified a small watch list of managers with relative underperformance (Artisan Global Opportunities and GPG global emerging markets were discussed) and said they are monitoring those managers’ fee negotiations, positioning and recent results. Trustees asked questions about vintage-year diversification, pacing for new private-market commitments, and whether higher distributions reduce near-term pacing; staff said they monitor distributions and manager pipelines continuously and can recalibrate pacing annually. No portfolio policy changes were adopted at the meeting.