Miami County studies competing insurance proposals; commissioners ask staff for clarifications before choosing provider

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

At a study session, staff reviewed three responses to a county RFP for workers' compensation and property/casualty coverage. Commissioners asked for follow-up on bonding, medical malpractice, deductible buy‑downs and retroactive dates and did not make a selection.

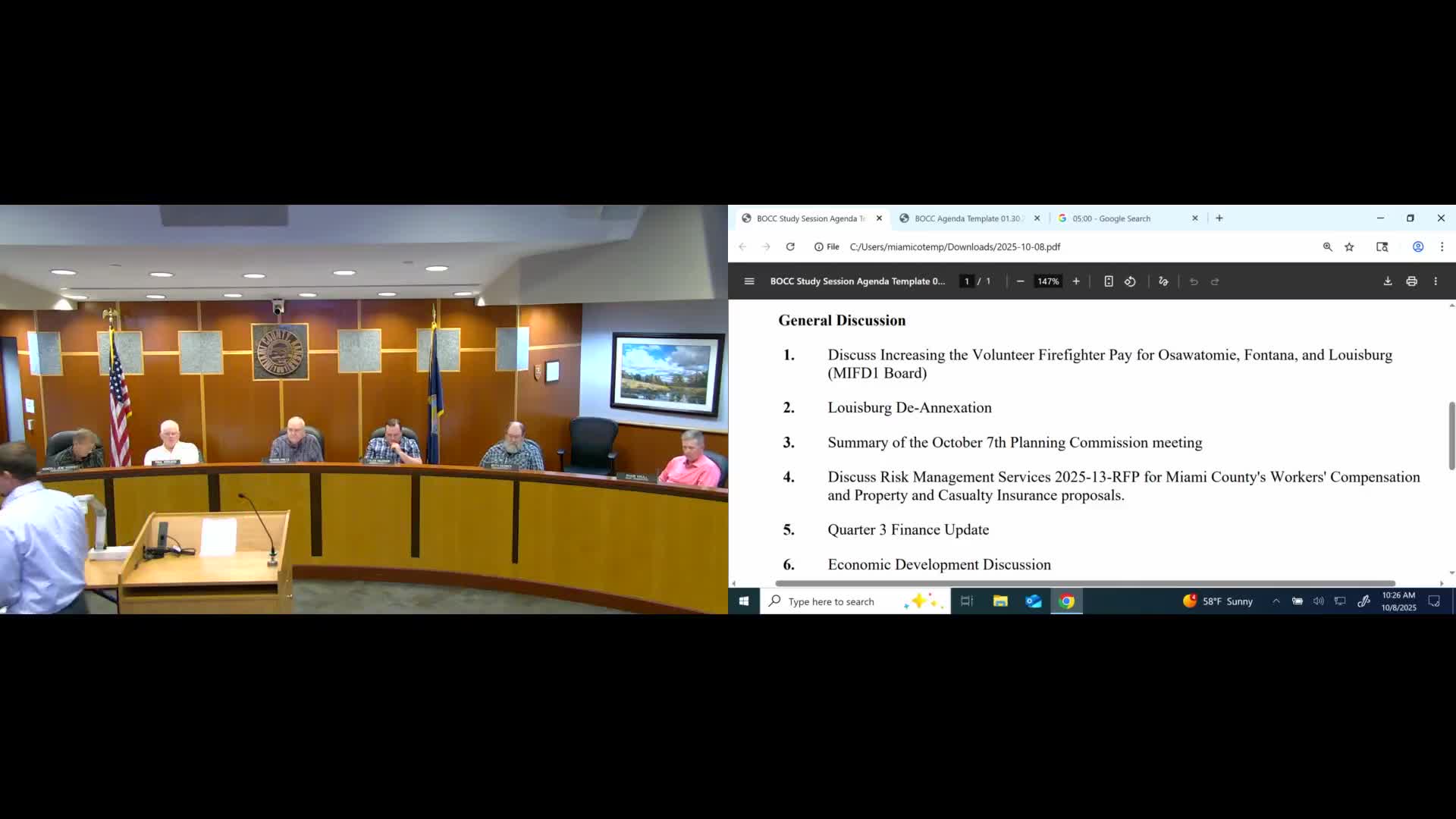

Miami County officials on Tuesday reviewed three proposals received in response to the county's request for proposals for workers' compensation and property and casualty insurance and asked staff for cost and contract clarifications before making any selection.

Assistant Finance Director Sydney Ming summarized the bids, saying the county received offers from two pools and one commercial carrier and that the proposals differ on limits, deductibles and ancillary coverages. Ming said the county received an initial proposal from "Kaye Work" (presented in the meeting as K Camp/K Works) and an offer from Elliot/EMC; she said the K Camp proposal included a $211,742 workers'comp option at a 1,000,000 limit and the Elliot proposal included a $220,580 workers'comp option, and that the two property/casualty proposals quoted roughly $568,000 and $551,056 respectively.

The board focused on several contract details that staff flagged as material differences. Commissioners asked staff to confirm: whether Elliot'EMC's property quote would pay replacement cost versus actual cash value for high value county buildings, the cost to "buy down" a per‑location wind/hail deductible to a flat $25,000, whether debris‑removal limits met the county's RFP requirement, whether bonding for elected officials is included, and whether medical malpractice endorsements cover county nurses and EMS personnel.

Colin Holt House, representing K Work, highlighted services that the county would receive from the pool, including in‑person training and small annual reimbursements such as post‑offer/preemployment testing reimbursement and jail training reimbursement; he asked commissioners to weigh service differences as well as premium. K Camp'affiliate David Luke emphasized that the pool'based proposal includes replacement‑cost coverage and other programmatic services tailored to public entities.

Commissioners pressed staff about several numeric differences in the proposals: the courthouse valuation used in bids (presented at $16,000,000), whether debris removal would be limited to $250,000 or be available up to multi‑million dollar blanket limits, and a reported supplemental cost of about $68,000 to buy down large deductibles to $25,000. Sydney Ming said staff would request specific supplemental cost sheets and confirm retroactive dates for claims‑made coverages.

No motion or vote was taken. Commissioners instructed staff to seek written clarifications from each respondent and to report back with: (1) the final cost to buy down large deductibles to the flat $25,000 option and how much that changes the premium; (2) whether an insurer'proposed policy provides replacement cost or actual cash value on each high‑value building listed in the RFP; (3) whether bonding for elected officials and medical malpractice endorsements are available and at what additional cost; (4) confirmation of debris removal sublimits and how they relate to the county'wide blanket limits; and (5) the retroactive date on claims‑made coverages.

The board scheduled no formal selection at the study session and left procurement decisions to a future meeting after staff provides the requested clarifications.

Ending: The county will not make a change in coverage without further written clarifications from the bidders; staff committed to return with supplemental pricing sheets and contract language for the board's review before any award.