Keller ISD board approves 2025 tax rate to preserve state funding; trustees debate no-new-revenue option

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The board approved a flat total tax rate of $1.0852 per $100 of assessed value after a lengthy discussion about losing copper pennies and the timing constraints of the state funding process.

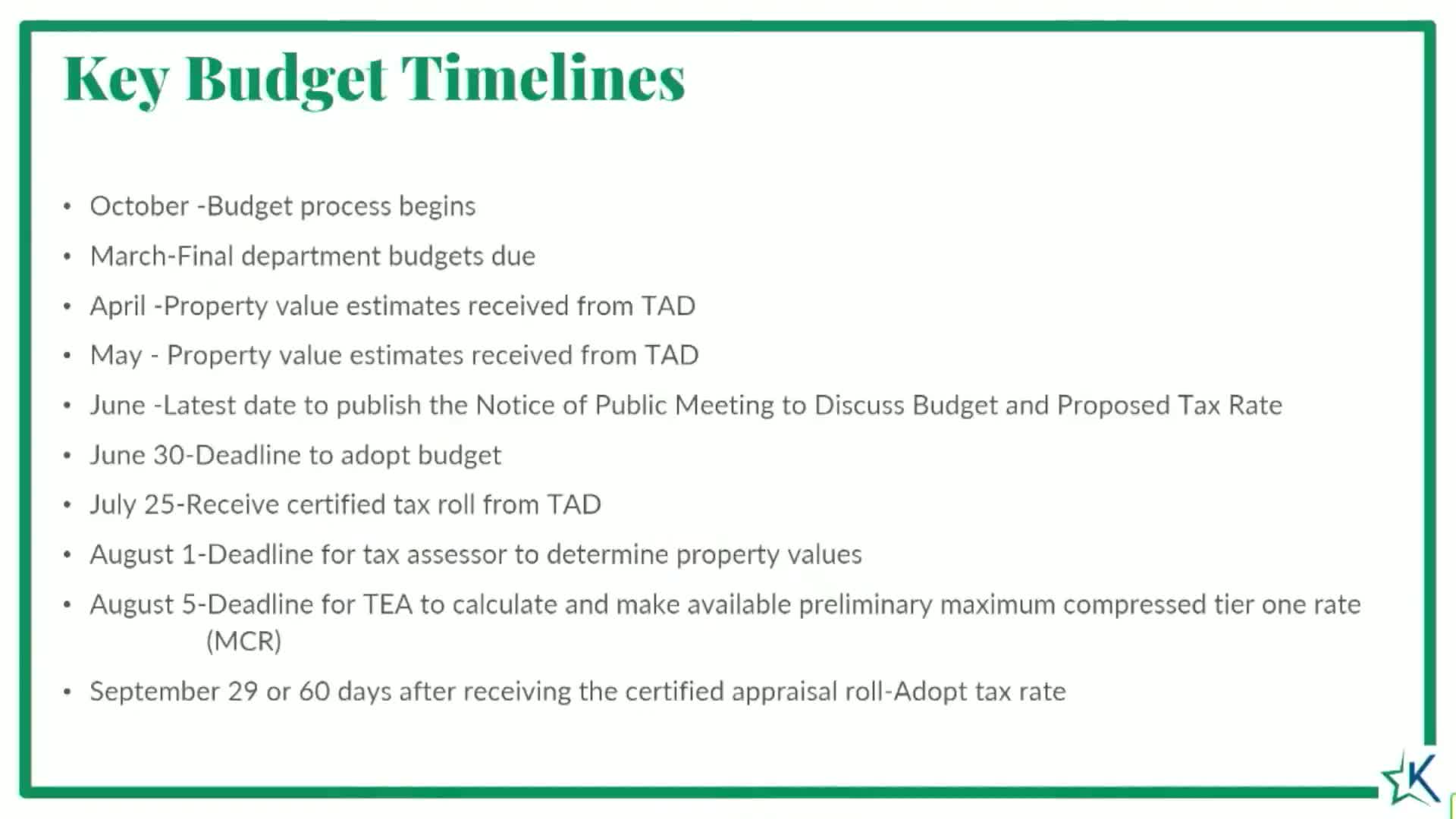

Keller ISD trustees voted to adopt the district’s proposed tax rate for fiscal year 2025–26 at a total rate of $1.0852 per $100 of assessed valuation — an M&O (maintenance and operations/enrichment) rate of 0.7552 and an I&S (interest and sinking) rate of 0.33 — keeping the rate flat with the prior year.

Chief Financial Officer John Allison reviewed the state funding and tax-rate mechanics before the vote, noting Keller’s maximum compressed tax rate (MCR) is 0.6169 for M&O under the state formula. Allison explained that lowering the district’s tax rate below the MCR would cause the district to forfeit copper pennies (enrichment revenue) and could reduce locally available revenue by an estimated $8 million under current assessed valuations.

Trustees debated whether to pursue a “no new revenue” rate to lower taxes for residents. Opponents argued that going below the MCR would permanently forfeit copper pennies and cause long-term funding loss; proponents said the board should pursue a plan that demonstrates cost reductions before asking voters to restore pennies later. Trustee comments included concerns about timing: several trustees urged earlier budget-parameter conversations so a no-new-revenue result could be planned in the budget process rather than imposed after the budget is adopted.

After discussion, the board voted to adopt the proposed tax rate; meeting minutes record the vote as 5 in favor and 2 opposed. Administration said adopting the rate as proposed preserves current state funding levels and supports the budget adopted for 2025–26.

CFO Allison and administration also told the board that adjustments to the I&S portion affect the district’s ability to refund bonds and that any meaningful tax-rate change would have to be planned earlier in the budget cycle to avoid creating a deficit.