County finance outlines IT internal billing; commissioners ask for service-level agreements

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

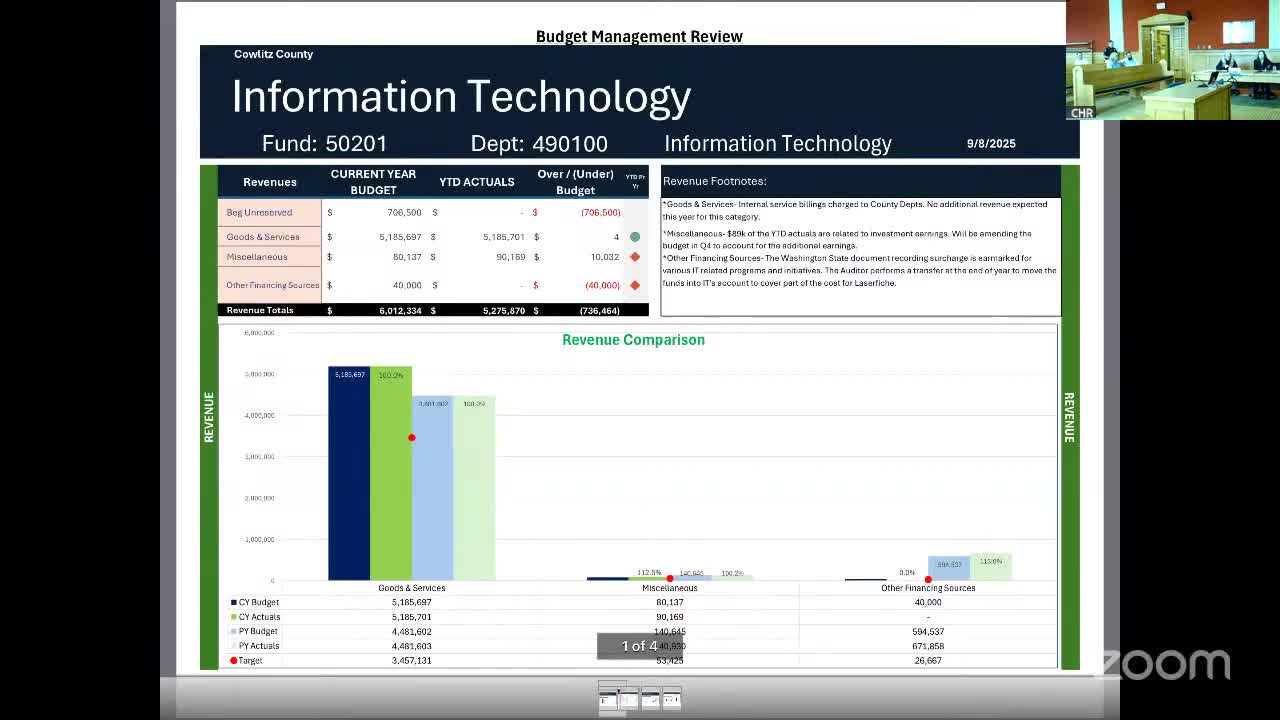

Finance staff told commissioners the IT internal service billing line fully collected and described the allocation methodology; several commissioners urged formal service-level agreements between departments.

At a Cowlitz County Board of Commissioners meeting, finance staff said the county has collected the full annual internal-service billing for information technology and described how those charges are allocated across departments. The discussion prompted commissioners to ask for written service-level agreements to set performance expectations between internal service providers and user departments.

Finance manager Susie Moon said the goods-and-services line that includes internal IT billings “has a budget of, just over 5,100,000.0, and we've brought in, that entire budget.” Cathy Baxter, the county finance director, attended the presentation to answer budget questions.

Commissioners pressed on how internal charges are calculated and whether internal providers are held to standards similar to outside vendors. “I think we should have expectations between people inside the county that provide service and the people that depend on that service,” Commissioner Raider said, arguing that internal providers should be held to measurable standards. Moon and Baxter said the budget office and department heads would present the IT allocation methodology at an upcoming budget workshop.

In the meeting commissioners and staff described the IT allocation formula: about half the charge is allocated by number of devices and half by head count in each department, applied against total IT costs. Moon said roughly 50% of IT costs are personnel and 50% software subscriptions and licenses, with other expenses included.

Staff also noted other internal service charge types: risk-management assessments, industrial-accident contributions, motor pool charges for departments that use county vehicles, and facilities allocations. Baxter said roughly 10 county units are treated as internal-service departments.

The commissioners asked whether written agreements or penalties for nonperformance exist between departments; staff said they were not aware of existing internal service-level agreements and that establishing them could be done as a project coordinated with user groups. Baxter and Moon agreed to present cost-allocation details and related materials in the county’s first budget workshop the next day.

The presentation did not include any formal vote or adoption of a new policy; commissioners directed staff to include the allocation presentation on the budget workshop agenda and to pursue discussion of performance expectations between internal providers and users.