County leaders weigh one-time purchase vs. recurring costs, tap special funds to lower budget shortfall

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Commissioners discussed using dedicated special funds and one-time general-fund spending to address courthouse space needs while clarifying that recurring expenses must not be shifted onto the general fund permanently.

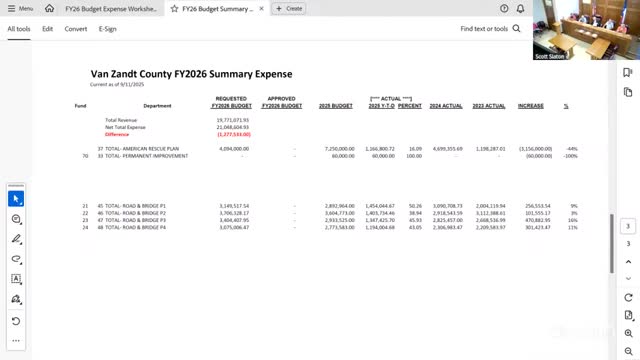

County leaders debated using one-time general-fund dollars or dedicated special funds to acquire a building (referred to in discussion as the Paul Michael Building or the South Trades Ace Boulevard building) for space needs, while several commissioners and staff identified special-purpose funds that could be used to reduce recurring general-fund expense.

The judge characterized the building purchase as a one-time expense that could be paid from the general fund while cautioning against placing recurring expenses on the general fund. "It's a one-time deal ... and then you regenerate that," the judge said, arguing that maintenance and recurring items should be paid from dedicated funds where appropriate. Commissioners clarified that the Paul Michael Building was not included in the operational expense numbers shown in the draft budget but that the general fund could be used if staff determines sufficient unassigned balance.

Staff and commissioners identified several special funds and dedicated revenue sources that they reallocated or proposed to use to lower the general-fund shortfall: the county clerk—s records fund for clerical salaries related to records management, an economic-development fund received from the comptroller to support committed incentive payments, law-library funds drawn from court fees, and other restricted funds such as ARPA. The judge said he had credited salary lines with SB 22 funds in the sheriff—s budget, which changed year-over-year comparability.

Why it matters: Using existing restricted or special-purpose funds for expenses that fall within each fund—s permissible uses can lower the general fund deficit without cutting services, but the judge cautioned the court to avoid treating dedicated funds as a permanent revenue source for recurring obligations.

Next steps: Staff will finalize whether the general fund can support a one-time building purchase and will prepare exact accounting transfers that move qualifying costs from the general fund into allowable special funds (for example, clerk records, law library, economic development).

Ending: Commissioners asked staff to present final general-fund and special-fund balances and present the purchase option and accounting transfers at the next budget workshop.