Oswego TIF shows budgeted deficit for 2026; village relies on loans and future development to cover obligations

Loading...

Summary

Staff told trustees the Hudson Crossing TIF is budgeting a deficit in 2026, carries outstanding interfund loans of about $11 million, and depends on development — including a delayed senior living project and parking garage increment — to meet debt service.

Village staff told trustees at a Committee of the Whole workshop that Oswego’s Tax Increment Financing (TIF) fund is budgeting a deficit for fiscal 2026 and will continue to rely on interfund loans and future development‑generated increment to meet debt obligations.

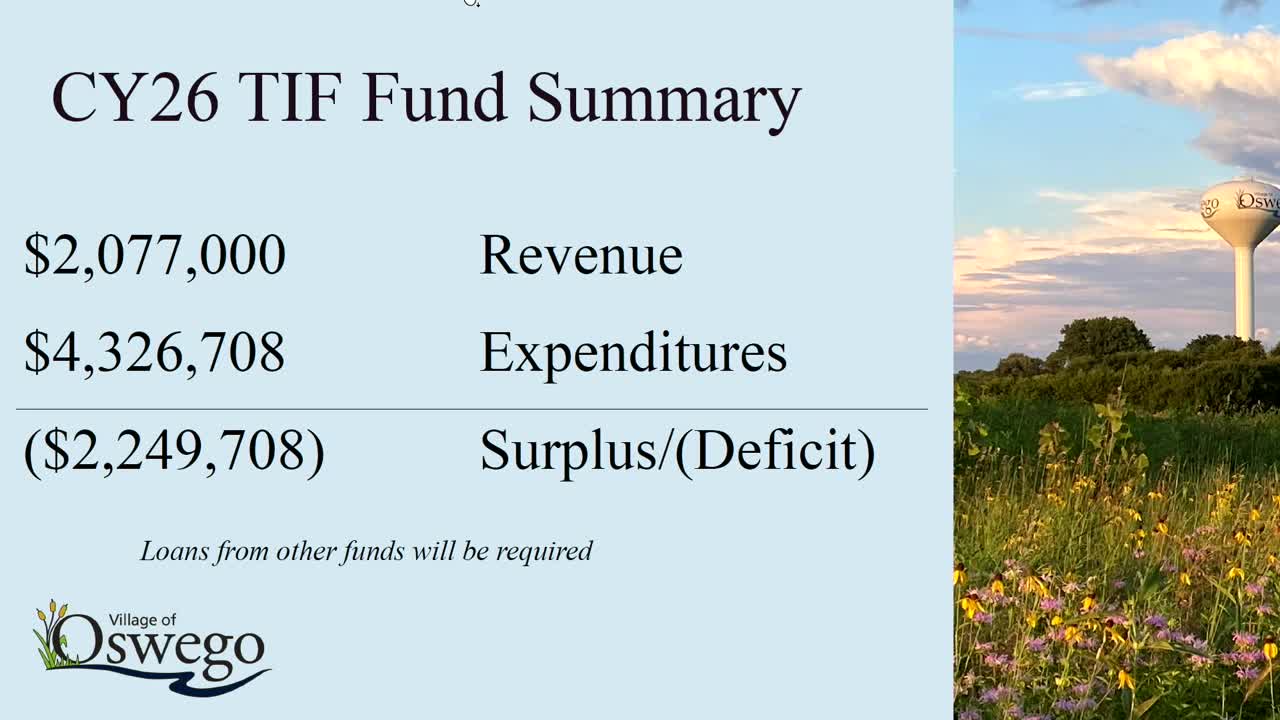

Andrea (staff member) said the TIF fund’s revenue for the year is estimated at just over $2 million while expenditures are about $4.3 million, producing a planned deficit. She explained the TIF was created “to encourage development in blighted and underdeveloped areas” and described the TIF as covering infrastructure that has been advanced before the increment to pay for it has materialized.

Key figures and mechanics: Andrea reported the TIF is starting with an $11 million beginning fund balance and that there are outstanding loans in the TIF of just over $11 million, most notably loans from the capital fund. She said 2026 debt service payments total just over $1.3 million and that bond obligations related to the South Parking Garage (Series 2019 bonds) mature with final payments in December 2041.

On sources of payment, Andrea stated that “the increment from the reserve at Hudson Crossing makes the bond payments,” and added that when increment falls short the second reserve party (identified in the presentation as a backstop) has issued checks to cover gaps in prior years.

Trustees pressed for projections on whether existing development outside of the Shodine property (the presentation discussed Hudson Crossing / Shodine reserve increment) will generate sufficient increment to repay the roughly $11 million in outstanding loans. Andrea said projections based on current development — without the second parking garage and without the senior living center — do not clearly show repayment, but that the addition of those developments “would potentially add to a surplus.”

On the senior living project, staff said it is delayed and not under village control; when completed, it is projected in the presentation to generate about $500,000 per year in TIF increment. Trustees and staff noted the senior facility is privately developed and that delays are a matter between project ownership and the contractor rather than a village action.

Other TIF projects discussed included: - Second parking deck: the village will own and maintain two floors; operationally the 2026 budget includes a modest operational increase (about $7,200). The presentation referenced construction photographs and a projected completion in 2026. - Downtown silo parking and lighting: a project budgeted at $275,000 with an expected $250,000 DCEO grant; the project is intended to add approximately 25 parking spaces, programmable LED lighting on the silo/granary, and other exterior improvements funded via a TIF beautification grant. - TIF participation in water main replacement on Main Street: staff said about 5% of the water main replacement project falls within the TIF district and would be eligible for TIF funding for that portion.

What trustees asked for next: Trustees requested follow‑up projections for the TIF at the end of its life (what surplus, if any, would remain after loans are repaid). Andrea said she did not have that figure at the workshop and that staff would follow up with a projection.

Ending: The presentation emphasized the “if not for” rationale for the TIF — that without TIF financing many of the downtown parcels would remain underdeveloped — and reminded trustees that the timing of development and tax assessments affects when increment becomes available to make debt payments.