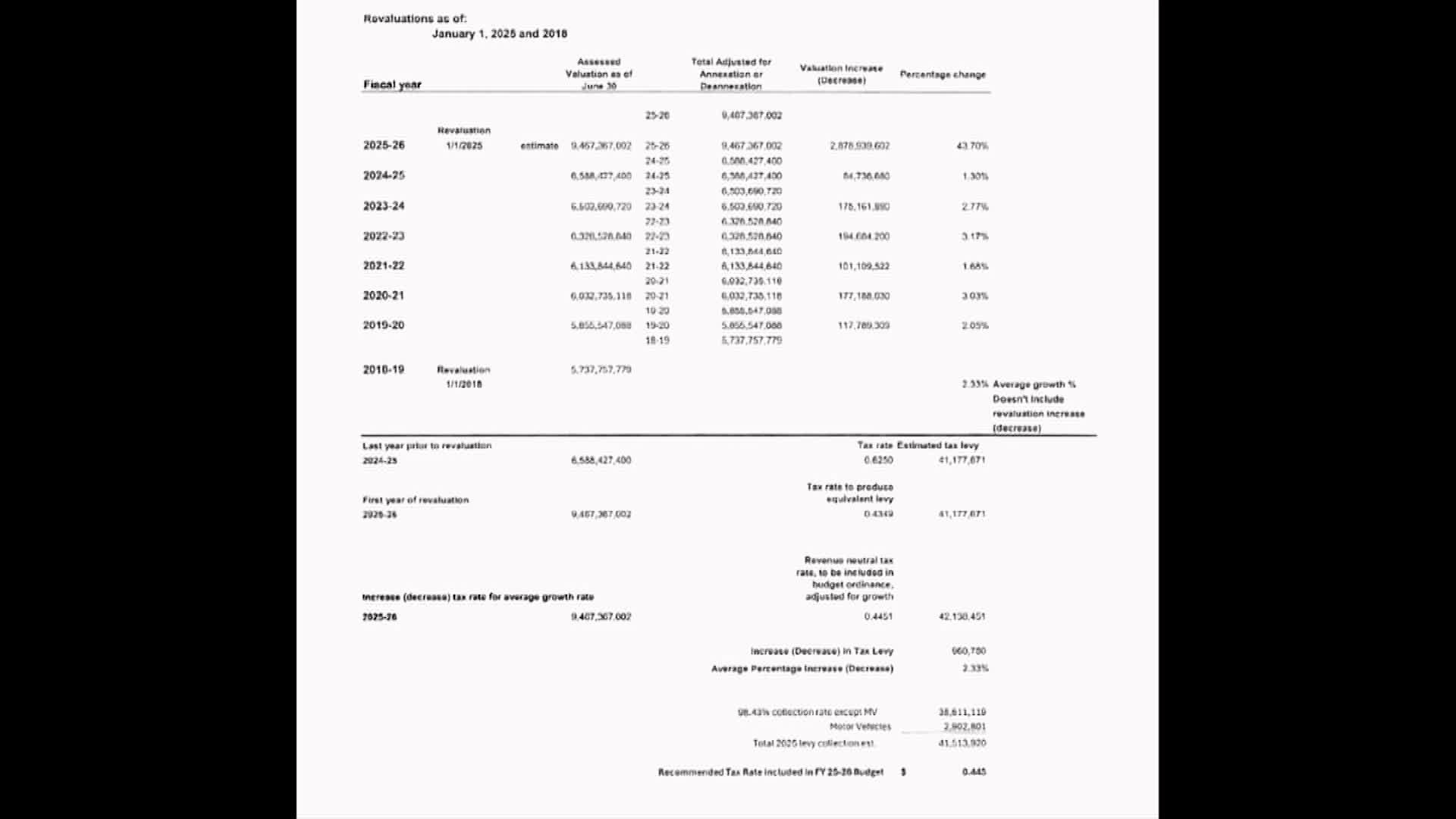

Beaufort County staff: certain sales tax articles and lottery proceeds will largely fund school capital and debt

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

County staff outlined four county sales-tax articles, their split with local schools, and how lottery proceeds combine with restricted sales taxes to pay school debt service and cash capital.

County staff explained how four local sales-tax collections and lottery proceeds flow to Beaufort County schools and county operations. Anita walked commissioners through article 39, 40, 42 and 44 sales-tax lines and the legal restrictions on two of them.

What was presented: Anita said the county retains 100% of article 39 (county sales tax), and staff estimated article 39 receipts of about $6.3 million for fiscal 2025–26. For article 40, Anita said state rules require giving 30% of revenue to schools for school capital; staff estimated article 40 at about $4,000,002.91, of which roughly $1.3 million would go to the schools. For article 42, she said 60% must go to schools; staff estimated article 42 receipts at about $3.5 million, with about $2.1 million required to go to schools.

Lottery proceeds and school debt: Anita said annual county lottery proceeds are about $480,000. She compared restricted sales-tax plus lottery proceeds to the county’s school debt service and cash capital requests and presented a restricted total of roughly $3,000,008.76 (sum of the percentage distributions and lottery proceeds). She explained that restricted dollars “can either be cash capital or debt service.” In the presentation staff showed school debt service and recommended cash capital amounts and noted that the restricted pool of funds is nearly fully allocated to either pay school debt service or provide cash capital to schools, with approximately a $75,000 difference in the year presented.

Why it matters: two sales-tax articles are legally restricted for school capital and therefore reduce the county’s flexible revenue. Commissioners asked whether lottery proceeds and sales-tax amounts would fully cover bonds; Anita said the lottery money alone is smaller than total debt service and the county uses the restricted sales-tax receipts plus lottery proceeds to make required payments.

Ending: Staff recommended commissioners review the restricted-sales-tax worksheet in the packet; the budget workshop did not adopt any changes to sales-tax policy — it was an informational briefing ahead of later budget decisions.