Delafield board upholds $732,000 assessment for 1614 West Shore Drive

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The City of Delafield Board of Review on May 29 sustained the assessor’s 2025 valuation of 1614 West Shore Drive after property owners argued deferred maintenance and lakefront quality warranted a cut to $610,000.

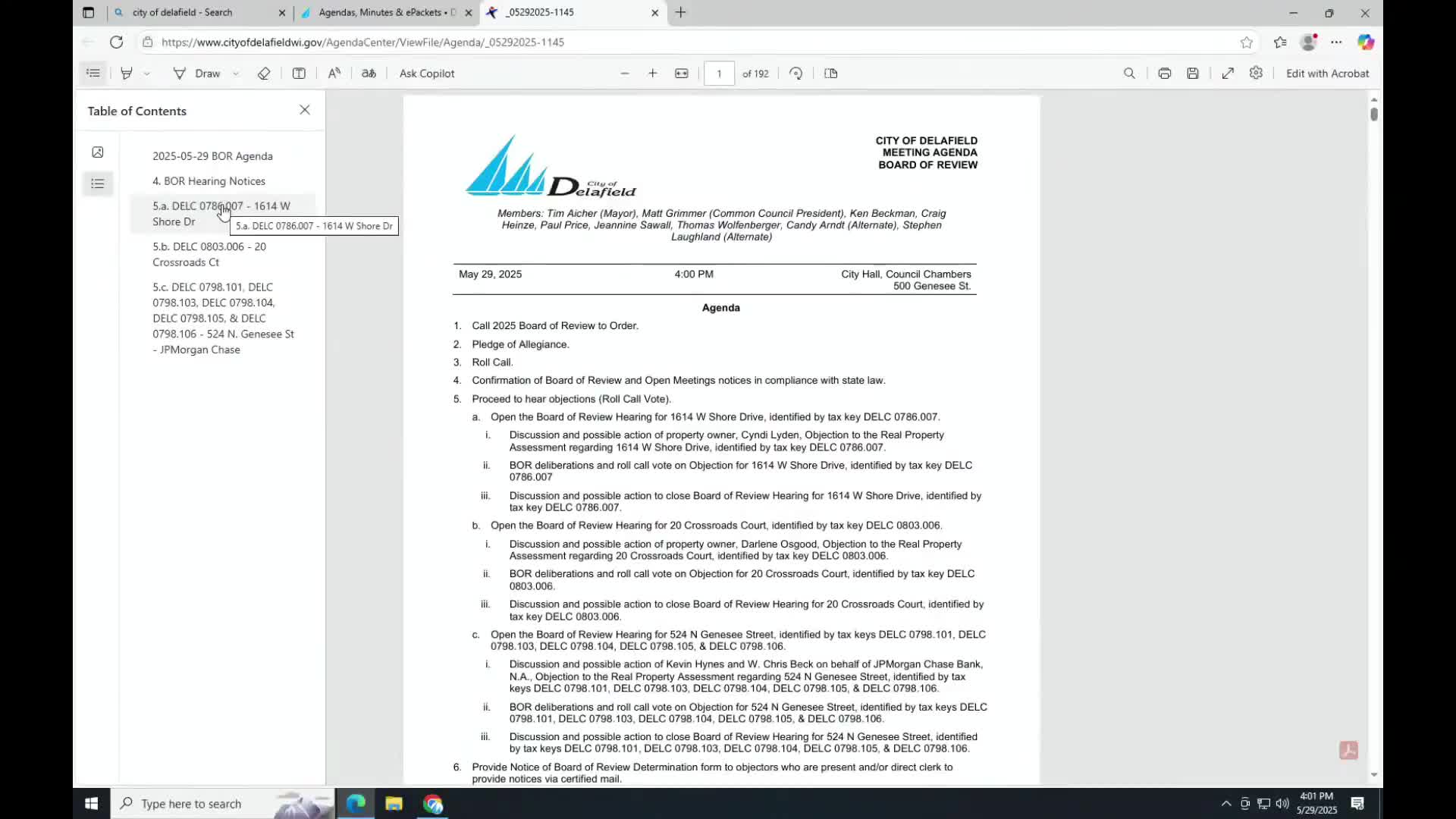

The City of Delafield Board of Review voted May 29 to sustain the 2025 assessed value of 1614 West Shore Drive (tax key DELC0786007) after hearing an objection from owners Cindy Lyden and Paul Rumler.

The owners asked the board to reduce the total assessment from $732,000 to $610,000, citing deferred maintenance and the property’s location on a “mucky” section of Lake Nagawicka. Owner Cindy Lyden told the board, "there's a lot of deferred maintenance," and said she calculated a $95,000 reduction for roof and chimney repairs and then allocated the remainder to the land.

The board’s finding summarized the assessment as of Jan. 1, 2025: land $506,100 and improvements $225,900 for a total assessment of $732,000. Assessor Cal Magnan explained the city’s reevaluation used a market-based cost approach and that the city’s comparables are computer-generated rather than hand-selected, noting ‘‘there were no inspections done for any of the properties in the city of Delafield for the reevaluation.’’ He also said the subject property had been graded C-minus with an interior rating of fair.

Members of the board questioned the owners about comparable sales and repair estimates. Lyden said she had contractor "napkin" estimates but not formal bids; the board noted she had not submitted recent local sales data or an appraisal for the property. Several members observed that the assessor’s process already reflected condition and location adjustments: the assessor reported the citywide average increase was about 40% from the reevaluation while this property’s increase was 31%.

After deliberation the board unanimously adopted a motion exercising its judgment under Wisconsin statute 70.47(9)(a) to determine the assessor’s valuation was correct. The roll call vote in favor: Mayor Tim Eicher; Alderperson Grimmer; Ken Beckman; Craig Hines; Tom Wolfenberger; and Steven Laughlin. The board advised the owners of appeal rights and provided the determination form.

The board’s decision notes it based the ruling on the evidence presented at hearing, the assessor’s use of statutory assessment methods and the lack of local comparable sales or contractor bids to substantiate the owners’ requested reduction. The board closed the hearing and returned the matter to the assessor’s valuation as of Jan. 1, 2025.

Less critical details: Lyden described family and long-term ties to West Shore Drive and asked the board to consider the household’s circumstances; the board noted those statements but based the decision on assessment evidence and statutory procedures.