Chicago Public Schools presents FY26 budget that preserves school funding, ties city pension reimbursement to new revenues

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

Chicago Board of Education officials presented a balanced FY26 budget proposal Aug. 19 that they say protects school budgets and labor contracts while closing most of a $734 million shortfall, but conditions reimbursement to the city for municipal non‑teacher pensions on new state or local revenue.

Chicago Board of Education officials presented a balanced FY26 budget proposal Aug. 19 that they say protects school budgets and labor contracts while closing most of a $734 million shortfall, but conditions reimbursement to the city for municipal non‑teacher pensions on new state or local revenue. Mike Sadowski, Chief Budget Officer for Chicago Public Schools, told the board the district is proposing a $10.25 billion budget that "fully protects this level of school funding from the previous year."

The budget matters because CPS said failing to protect school funding would reverse recent gains and risk midyear cuts and layoffs. Sadowski said the proposal closes $165 million of earlier gaps and still requires $569 million in additional strategies to balance FY26; the package CPS brought forward includes $126 million in additional reductions away from classrooms, $149 million in added revenues, $29 million in accelerated debt‑refunding savings, $90 million in one‑time sources and a $175 million condition on making a municipal pension reimbursement.

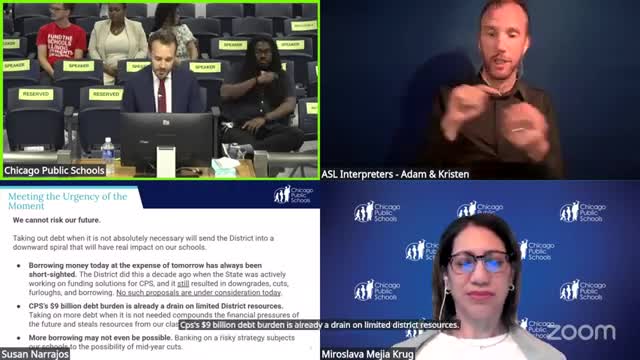

CPS framed the plan as protecting students and staff while avoiding the kind of high‑cost borrowing and downgrades the district suffered after operating‑fund borrowing in the 2010s. "Taking out debt when it is not absolutely necessary will send the district into a downward spiral," Sadowski said. Finance chief Miroslav Krug warned that additional operating borrowing could trigger credit downgrades, substantially raise borrowing costs and reduce future capital and refinancing savings.

Key numbers and assumptions in the proposal cited by CPS officials: the FY26 deficit before new actions was $734 million; $165 million in earlier spring reductions; $126 million of additional central‑office and other reductions to reach stakeholders' goal of protecting classrooms; $45 million of higher-than-projected state evidence‑based funding (moving CPS back into tier 1 of the formula); a $79 million increase in the district—s assumed TIF surplus from the city; $29 million of accelerated bond refunding savings; $65 million taken once from the district—s debt service stabilization fund; and $25 million in philanthropic carryover—all together intended to avoid furlough days and additional classroom cuts.

On the contested municipal pension matter, Sadowski said Illinois law requires the city, not CPS, to fund the Municipal Employees— Annuity and Benefit Fund (MEABF), and the FY26 proposal makes any CPS reimbursement "contingent upon additional FY26 state revenue, additional FY26 TIF surplus revenue, or other local revenues above our budgeted assumptions." He added that the budget "allows for CPS to reimburse the city for MEABF with new state or local revenues, unlike the FY2025 budget that did not allow for this possibility."

CPS officials emphasized the risks of additional operating borrowing. Krug described past downgrades and said market penalties could add 145–160 basis points in recent months; he and Sadowski explained that taking short‑term loans to cover operating gaps could increase future deficits and force steeper cuts. "Borrowing for operating expenses would send district in a downward spiral of credit downgrade, higher interest rates, and steeper cuts to staff, programs and services in the future," Krug said.

Board members asked for clarity about the TIF assumption and the projected borrowing costs. Sadowski and Krug said the extra $79 million in TIF assumed for FY26 came from recently surplused TIF balances and that the calculation follows the city's publicly published TIF surplus rules and the state TIF statute. When asked about contingency plans if TIF surplus were lower than assumed, CPS leaders said they had exhausted structural and one‑time tools and stressed the need for new state or city revenue to avoid borrowing.

Sadowski closed by saying the district will present the balanced budget for board approval at the Aug. 28, 2025 board meeting. He said the plan "funds all of our contractual commitments to our labor partners, delivers on the promise to stabilize school budgets," and includes only borrowing that provides savings or is necessary for capital.

For now the proposal is a staff recommendation; the board scheduled a formal vote at the Aug. 28 meeting. Questions from board members during the hearing focused on the durability of the TIF assumption, the tradeoffs of using one‑time reserves, and the credit risks of additional operating borrowing.

Provenance: presentation and Q&A during the FY26 budget hearing on Aug. 19, 2025; key remarks by Mike Sadowski and Miroslav Krug are recorded in the hearing transcript.

What happens next: CPS staff will present the finalized FY26 budget for board consideration on Aug. 28, 2025; any vote and final funding decisions will be recorded in the board minutes.