State auditor staff review reporting templates, submission deadlines and where to find forms

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Utah State Auditor's Office staff reviewed the state reporting system, budget and financial-report templates, and submission deadlines for local governments, and pointed attendees to the office's updated Local Government Resource Center for forms and guides.

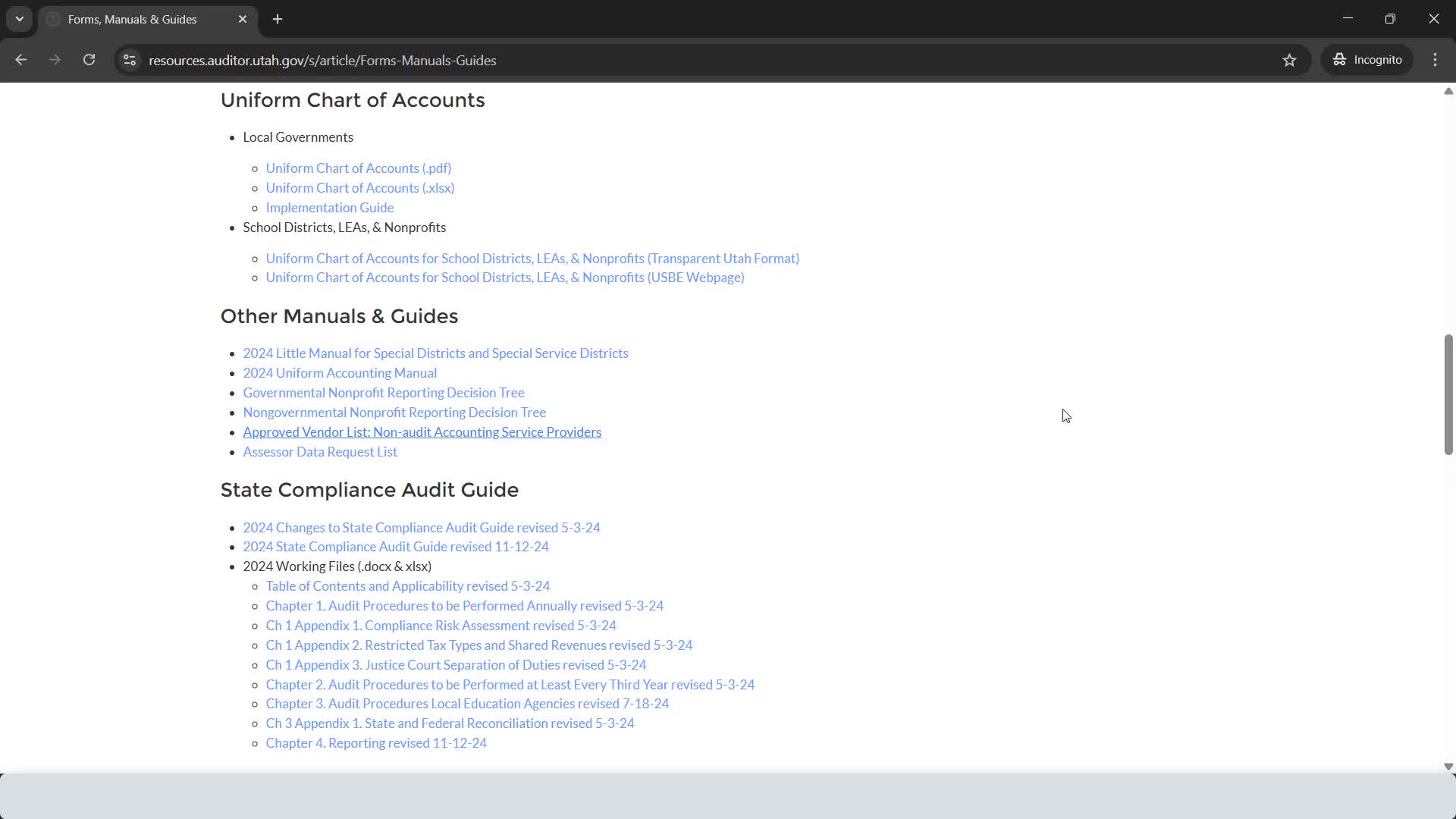

Utah State Auditor's Office staff told local government clerks and officials at a compliance training that the office's Local Government Resource Center on auditor.utah.gov is the primary location for reporting templates, guidance and FAQs and that many forms are updated each May after the legislative session.

The resource center contains the forms, manuals and guides for budgets, financial reports, financial certification, fraud risk assessments and impact-fee reporting, among other materials, the presenter said. "This is the local government resource center, and this website is a great website to bookmark," the presenter said.

The training explained differences in report types based on entity size. Small financial surveys are for entities with revenue or expense totals below $350,000; larger entities typically use templates or export from accounting software. The presenter advised using the office's templates when possible because they reflect the format required by state code and have built-in calculations.

On budgets the presenter demonstrated the auditor's municipal and special-district budget templates and emphasized the common error of not including three years of comparative data: budget year, current year and prior year. The special-district template was described as available for download but not mandatory if an entity's accounting software can export the required fields.

Staff reviewed submission locations in the state reporting system and recommended that entities update contact information in that system at least annually so the auditor's office has current primary and finance contacts. The presenter also noted the deposit and investment report is handled through the treasurer's office and provided Anne Pedroza's email for questions about that submission.

On deadlines, staff said calendar-year entities should submit reports in June (with July as a grace period), receive 60-day delinquency notices in August and hold notices in October if still missing; fiscal-year entities (July 1'June 30) have parallel deadlines with reports due in December, a grace period in January, 60-day notices in February and hold notices in April. Budgets must be filed within 10 days after adoption and no later than the start of the fiscal year.

Staff noted the compliance dashboard (transparent.utah.gov/compliance) shows current status for an entity and can be used to download evidence of compliance. They also recommended preferred upload formats (PDF, Excel, Word) and warned that image files are bulky and harder for reviewers to read.

Ending: Staff offered phone and email help and said training materials and a short state-reporting tutorial video are available on the resource site for step-by-step instructions.