Proposal to impose 1% county grocery tax fails in 3–3 committee tie

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

A proposal to establish a 1% county grocery retailer and grocery services occupation tax for unincorporated areas resulted in a 3–3 tie in the finance committee and failed to pass; proponents said it restores revenue that had been diverted to the state.

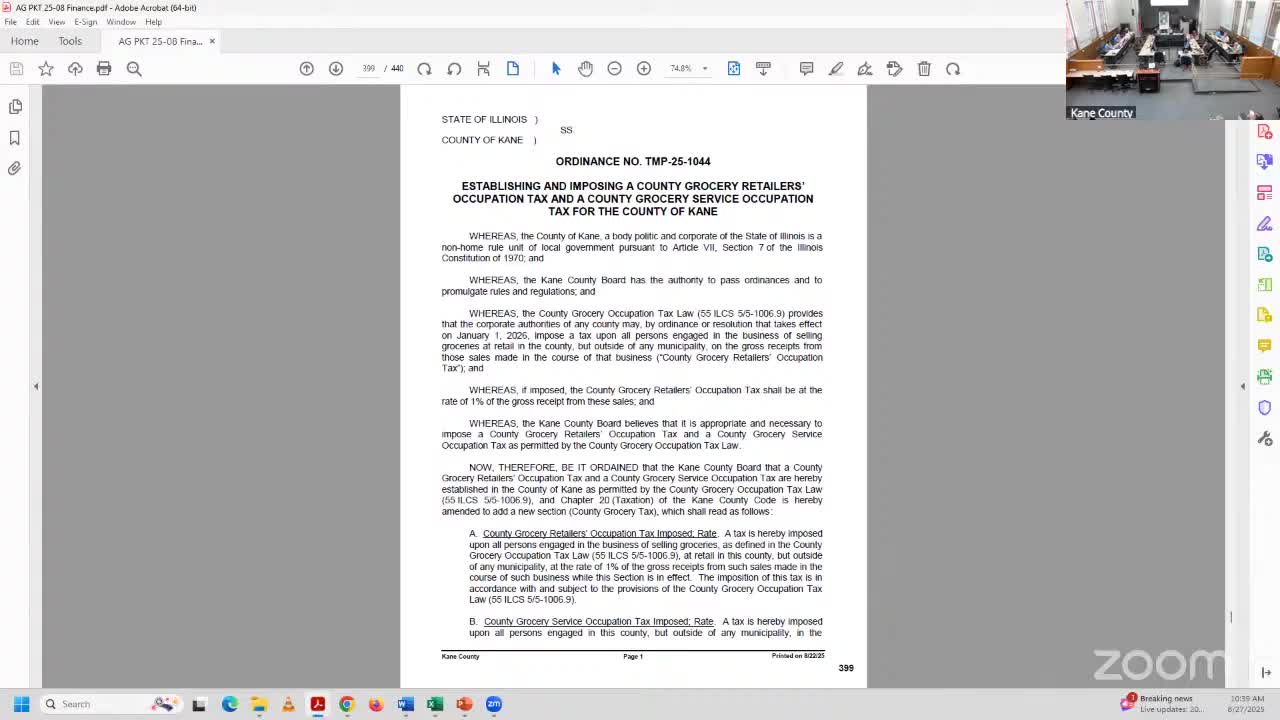

KANE COUNTY, Ill. — The Finance and Budget Committee on Aug. 27 voted on an ordinance to establish and impose a 1 percent grocery retailer’s occupation tax and a 1 percent grocery services occupation tax in Kane County’s unincorporated areas. The measure resulted in a 3–3 tie and failed to advance from the committee.

Supporters framed the tax as a revenue restoration: committee members said the county previously shared in this revenue stream but that state law changes had removed the local share, so adopting the tax would keep the revenue local rather than diverting it to the state. One member said the county and neighboring jurisdictions have adopted the levy.

Opponents and questions: Several members said they worried about how the new revenue would be used and requested stronger guarantees that proceeds go to the general fund and county priorities. The county’s assistant state’s attorney said the county board can direct where locally collected revenue is appropriated in its ordinance, although state law could later change that allocation.

Outcome: Because the vote was tied, the ordinance did not pass committee. At least one committee member asked that the issue be considered by the executive committee even after the tie vote.

Why it matters: A grocery tax affects many residents and local retailers and would yield recurring revenue; but it is politically sensitive, and committee members expressed competing concerns about fiscal need versus imposing additional local taxes.