Committee warns Cook County tax delays strain cash flow; staff proposes 6‑month treasury benchmark for investments

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

Committee members said recurring Cook County property-tax payment delays are disrupting District 200 cash flow and limiting investment opportunities. Finance staff proposed changing the monthly investment benchmark from a one-year treasury bill to a six-month T-bill and adding additional short-term benchmarks for context.

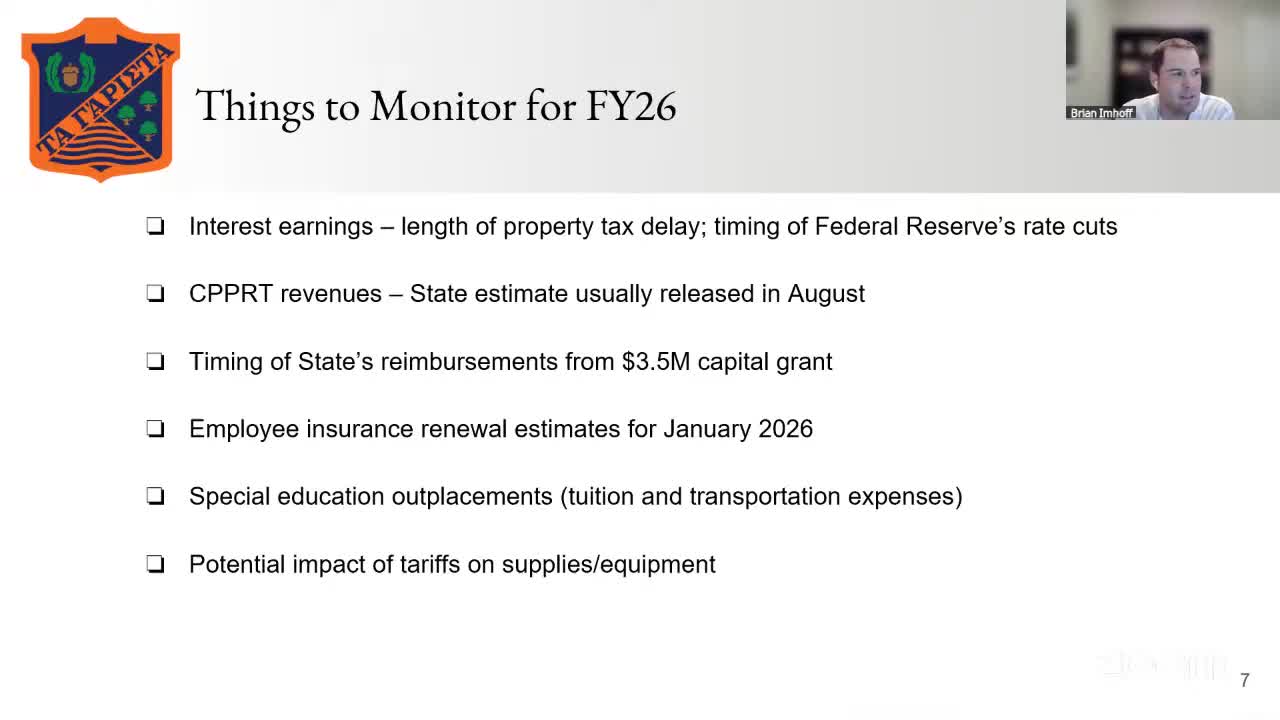

Members of District 200’s Community Finance Committee raised concern on Aug. 12 about repeated delays in Cook County property-tax distributions and discussed steps to manage short-term cash and investment benchmarking. Brian, a finance staff member, said the district is currently in a holding pattern for new investments while it waits for property taxes to arrive; the majority of investment purchases normally occur in August–September and around March, when property-tax receipts are largest. He recommended changing the packet’s investment benchmark from a one‑year treasury-bill rate to a six‑month T‑bill rate to better reflect the shorter investment horizons staff expects because of cash-flow timing. A committee member described the cause of recent county delays as an accounting and technology upgrade at the county that has pushed bills and distributions later and criticized the county’s sparse communications about timing. The member said the county has not provided clear penalties or remediation and that the irregular schedule has created borrowing and investment challenges for taxing bodies. The nut graf: Staff emphasized that when property-tax receipts arrive late, the district’s ability to invest funds for longer terms is constrained; committee members suggested adding three benchmark lines (three‑month, six‑month and one‑year T‑bill rates) to the monthly report to provide context for performance comparisons. Practical implications: The committee discussed trade-offs among fund balance, short-term borrowing and debt issuance timing. One member said that if the district can access affordable short-term liquidity (for example, a line of credit or expedited bond sale), it may not need as large a cash reserve. Another member said the district should document levy recapture capacity and other legally available revenue options for transparency when making decisions on fund-balance targets. Ending: Staff said they will bring a revised treasurer’s report showing the additional benchmarks and will return with more detailed cash-flow and levy-capacity information at upcoming committee meetings.