Board discusses Principal high‑yield product swap, pauses manager change and asks consultants to return with options

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Consultants told the Elevate Pension Board Principal merged the plan’s prior high‑yield product into a replacement vehicle on Feb. 28; trustees asked consultants to present manager options and to evaluate core‑plus alternatives before making a change.

The Elevate Pension Board received an update on its high‑yield allocation after Principal moved the plan’s prior high‑yield product into a new Principal high‑yield fund on Feb. 28.

Tom and Jonathan, the board’s investment consultants, told trustees the swap reduced the urgency of the previously authorized manager search but did not eliminate the need to evaluate alternatives. Tom described the change as a forced consolidation: the prior product “ceased to exist” and was “merged into the new Principal high yield fund” on Feb. 28.

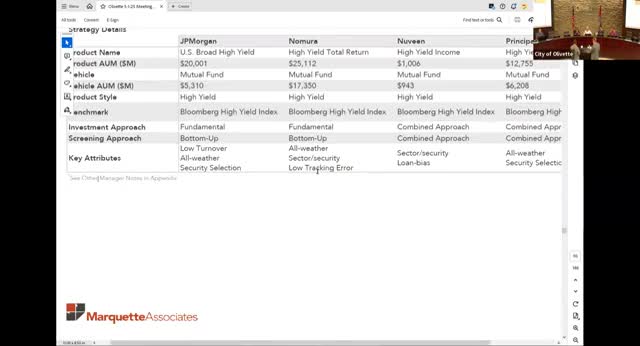

Consultants presented a short list of candidate managers for a replacement high‑yield sleeve: JPMorgan, Nomura, Nuveen and Principal (the newly available Principal vehicle). They discussed differences among the strategies, including relative allocations to syndicated bank loans (Nuveen’s vehicle showed the largest loan bias in the materials) and differences in average quality and duration (Tom noted Principal’s newer high‑yield vehicle has an average duration near seven years and average quality around B+ on the materials presented).

Board members asked whether Nomura or Nuveen materially outperformed Principal over multi‑year horizons. Consultants said Nomura has been a historical return leader on the presented time frames, while Principal’s new vehicle has been “holding its own” and typically exhibits lower volatility in some periods. The consultants cited gross/net return differentials and fee levels: Principal’s new vehicle was presented at about 67 basis points in the slides, against Nomura at about 54 basis points; consultants reminded the board that reported returns are net of fees.

After discussion the board did not select a new high‑yield manager at the meeting. Instead, trustees directed the consultants to return with detailed manager options and to expand analysis to include core‑plus strategies as a potential alternative allocation. One consultant summarized the direction: “Why don't you guys come back with some options there, and we can look at it as a whole…and the core plus.”