Smithville staff say revenues are stronger than expected; 2026 budget to include bond-funded utility projects

Loading...

Summary

Smithville staff told the board the nine-month budget picture is stronger than the adopted projection, narrowing the city’s expected 2025 deficit and setting the stage for a 2026 budget that relies on certificates of participation and bonds to fund several large water and wastewater projects.

Smithville staff told the board during a work session that revenues through mid-August are outpacing earlier conservative projections and that a combination of stronger sales/use tax, permit activity and interest income has narrowed the city’s projected fiscal gap for the current year.

Rick, finance staff member, said the city’s year-to-date projected revenues were “just under $7,300,000” at the nine-month mark and that sales tax receipts as of Aug. 15 were about $1,440,000 while use tax was approximately $900,000. He told the board the 2025 adopted budget had assumed roughly an $810,000 deficit but that, based on current trends, staff now expects that shortfall to shrink to about $153,000 by year end.

The update matters because it frames a proposed 2026 budget that staff presented to the board. The draft for next year shows roughly $22 million in total proposed revenues and $33 million in proposed expenditures, driven largely by major water and wastewater capital projects that staff plan to fund in part through certificates of participation (COPs) and other bond issuances.

City staff stressed that the city’s budget approach remains conservative on both revenues and expenditures. The finance presentation highlighted several revenue drivers this year: sales tax growth tied to commercial development, use tax gains from online and large retail activity, an uptick in permit receipts driven by larger commercial projects, and higher-than-expected interest income. The presenter said those factors have repeatedly offset conservative estimates in past years and have helped maintain the city’s reserves.

Staff also highlighted uncertainty tied to the recently enacted senior property tax freeze. Clay County assessor data provided to the city on the same day shows about 20% of parcels preliminarily qualify for the freeze; staff said the county data is preliminary and that the city will not know the full revenue impact until the county finalizes rolls and taxpayers’ annual applications are filed. “We’ll continue to monitor that closely,” the presenter said.

On utilities, staff described a multi-year capital program and said five to six large water and wastewater projects are planned to begin or continue in 2026 and will be included in the COP/bond financing. The presentation listed specific projects that staff intend to bond when they reach construction—items shown on the project list include 140 Fourth Street, Smiths Force Main, Maple Avenue work, River Crossing and the Stonebridge lift station. Staff said a separate large placeholder—an expansion or major upgrade to the wastewater treatment plant—remains in the long-range (four- to five-year) plan and was shown as a $14–15 million placeholder in planning documents.

Staff warned that many capital projects move between years depending on engineering and reimbursements. Several planned projects previously budgeted for 2025 were pushed into 2026, including the Commercial Street sidewalks and portions of the Railroad Trail Phase 1. Staff noted that reimbursements from outside funders are a major timing factor and that the city often budgets full project costs in a single year even though work and drawdowns typically span multiple fiscal years.

The presentation included several proposed new operating items for 2026: a new standalone parks position (estimated at about $92,000), a GIS/IT technician split between administration and utilities (roughly $41,000 per department), a $25,000 lease payment for a mini excavator (leasing rather than purchasing), and a $20,000 wellness stipend program (up to $300 per employee). Staff also recapped a vehicle-replacement transfer of $485,000 that was made in July and said fleet management will continue to be actively managed across departments.

Staff outlined a proposed public-safety half-cent sales tax set to begin collections Oct. 1, with first-year receipts estimated at about $700,000; the city plans to use that fund largely for police staffing, equipment and an animal-control position. The finance update noted no water/wastewater rate increase planned for the Nov. 1 billing cycle; staff said a rate study and updated master plans are scheduled for late 2025 and early 2026 and any rate changes would be considered after those studies are complete.

On long-range capital, staff presented a five-year capital outlook that totaled approximately $67.7 million in today’s dollars. That number includes bonding assumptions for large utility projects and placeholders for major items such as the wastewater treatment plant work. Under staff projections—if all projects proceed on schedule—the utility fund reserve policy target (20%) could be at risk in later years, which informed the proposed use of COPs and bonds.

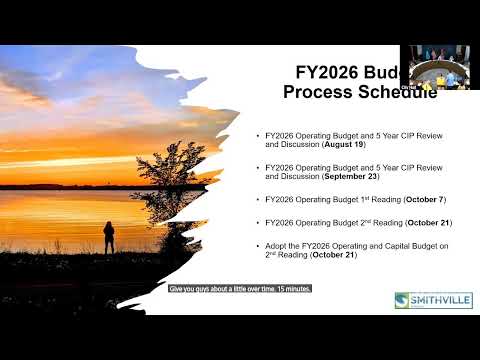

Board members asked clarifying questions about the timing of tax receipts, the mechanics of when new construction becomes taxable, reimbursement timing for projects, and how the senior freeze would affect future levy-setting. Staff advised a conservative approach to projections until county assessor numbers are final and recommended proceeding with the board’s planned timeline: finalize the draft budget in September and bring the first reading in October with adoption to take effect Nov. 1 if no substantial changes are requested.

During the work session the board also directed staff to begin developing an RFP for a strategic planning process and for staff to prepare procedures for allocating a planned outside-agency assistance fund if the board chooses to include that in the final budget. Staff said these processes should be ready to implement shortly after the fiscal year begins so eligible expenditures or projects can start in early November.

The work session concluded with a motion to adjourn; a second was made, and the board voted to adjourn the work session. Staff will return with an updated draft and additional materials at the board’s September meeting and plans to bring the budget forward for two readings in October with an anticipated effective date of Nov. 1, 2026.

Ending: The budget work session gave the board an early look at 2026 priorities and financing plans; staff emphasized conservative assumptions, continuing uncertainty around the senior property tax freeze and the role of bond financing for major utility projects as they develop the final document for the October readings.