White Plains unveils $219.5 million proposed budget; tax rate to rise 2.49%

Loading...

Summary

Budget Director Jim Arnett presented the proposed FY2025–26 operating budget to the Common Council on April 22, outlining a $219.5 million spending plan, a proposed tax rate increase of 2.49% and targeted use of fund balance and grants to limit new tax burden.

Budget Director Jim Arnett presented the White Plains Common Council an overview of the proposed fiscal year 2025–26 operating budget on April 22, telling the council the plan would require adoption by May 30 under the city charter and that a public hearing is scheduled for the council meeting on Monday, May 5.

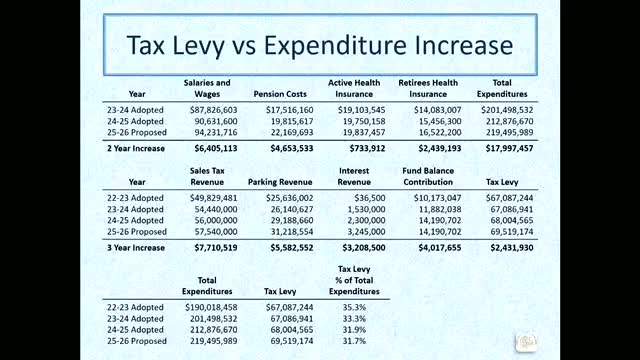

Arnett said the proposed total expense appropriations are $219,500,000, a 3.1% increase from the current year. He said the city is proposing a tax rate of $250.27 per $1,000 of assessed value — an increase of 2.49% — and that the leap in the rate stems primarily from a decrease in the total assessed base. Arnett said the typical homeowner with a median assessed value of $13,500 would pay about $82 more per year if the budget is adopted as proposed.

The proposal, Arnett said, continues the city’s practice of staying within the New York state property tax cap and maintains the city’s long-held credit standing: “the city has maintained a double A‑1 credit rating since 1988,” he said. He told the council the proposed tax levy without exceeding the cap would be 3.4% (about $2.4 million); the budget as proposed increases the levy by roughly $1.5 million, leaving a potential rollover of about $600,000 into the next year under the tax-cap rules.

Why it matters: the council must adopt a final budget by May 30 under the city charter; the rate and levy determine local property-tax revenue and the share of residents’ bills attributed to the city portion of taxes.

Key revenue and expense items Arnett said property taxes account for about 32% of the budget and sales tax about 26%; together with parking revenues those three sources make up roughly 70% of general fund receipts. He said the city is budgeting conservatively for sales tax (budgeted at $57.5 million for 2025–26 after a projected $58.6 million in 2024–25) because of economic uncertainty despite recent strong receipts.

Arnett identified a new recurring revenue line this year: estimated cannabis sales tax revenues of $680,000, which he described as a conservative estimate based on recent quarters. He also said the proposed budget uses about $16,000,000 of fund balance made up of undesignated funds and amounts set aside for tax certiorari settlements.

Salaries, staffing and benefits Salaries and employee benefits make up over 74% of the proposed budget, Arnett said. The proposal adds five positions (three police officers and two firefighters); the city lists 912 total positions with 860 funded in the proposed budget, a net decrease of 10 funded positions from the 2024–25 adopted budget but an increase of one in the proposed count compared with earlier estimates.

Pension and debt service Arnett told the council pension costs increased an estimated 11% for both police/fire plans and the Employee Retirement System and that those combined pension and salary expenses account for a large portion of the recent spending growth. The general fund transfer to the debt service fund is proposed at $14.8 million for 2025–26, an increase of $600,000 driven by the timing of principal payments from a late bond sale in the prior fiscal year.

Grants and capital items Arnett said the city continues to seek grants to offset tax-funded expenses. He named two NYSERDA grants included in the 2025–26 budget: one for purchasing two electric police vehicles and another for installing heat pumps at the city garage. He said some NYSERDA funding is also being used for capital projects.

Council questions and clarifications Councilman Morton asked for the fiscal-dollar equivalent of a 1% change in the tax rate; Arnett responded that the comparable dollar amount has varied historically and worked through recent levy figures with the council in discussion. Morton also asked about the stabilization fund; Arnett said the tax‑stabilization balance was $8.6 million at year end (June 30, 2024) and estimated it could decline to roughly $6.5 million by the end of the current fiscal year, depending on usage.

Arnett closed the presentation and invited follow-up questions from the council ahead of the May 5 public hearing.

Ending: The council’s formal review continues at the public hearing on May 5; the budget must be adopted before May 30 under the city charter.