Longmont staff present 2026 budget with revenue pressures; staff recommend incremental-policy changes

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

City finance staff presented a 2026 proposed budget that uses fund balance to cover a projected gap as sales and use tax have weakened while property tax reassessment boosted revenues; staff proposed technical policy changes including raising the development-revenue baseline and moving utility-billing operations out of the general fund.

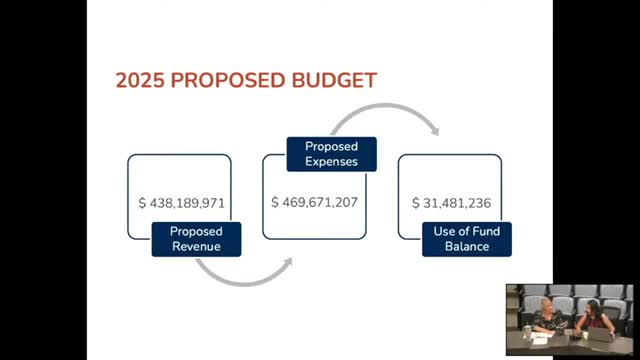

Longmont Finance staff presented the city’s proposed 2026 budget at the Sept. 2 council study session, describing a mix of revenue headwinds and one-time policy choices that produce a $520.2 million expense plan supported by $476.3 million in projected revenues and a planned draw of $43.9 million in fund balance mostly for capital programs.

Sandra Cifuentes, budget manager, and Theresa Moy, chief financial officer, told council that sales and use tax collections are weaker than in prior years and that use tax — the tax tied primarily to construction permits — was down sharply through midyear. “Our performance through June is not really looking too great. We are up 1.9% in sales tax but down significantly 21% in use tax for a combined overall decrease at this point of 1.4%,” Moy said. The proposed 2026 budget assumes modest improvement and projects combined sales and use tax growth of roughly 0.5 percent for 2026.

Property tax is projected to rise in 2026 because 2025 is a reassessment year. Cifuentes said part of the new property-tax revenue adopted during the 2025 budget was held as one-time money; staff proposed allocating $1.2 million of new ongoing property-tax revenue to cover recurring costs and reserving $770,000 as one-time funding pending final county certified values.

A major bookkeeping component of the budget is carryover: Cifuentes said about $196.9 million of the revised and adopted 2025 budget is carryover for multi-year capital projects, grants and bond funds, and additional appropriations so the revised 2025 budget grows in total to $704.9 million when carryovers are included.

Structural and policy recommendations: Staff proposed several technical and policy changes to smooth revenue volatility and better match ongoing service demands. Notably, they recommended raising the “incremental development revenue” baseline used to decide which new permit-driven revenues are treated as recurring from 200 new dwelling units to 300. “The three-year average is 624 permits, new dwelling units,” Cifuentes said; staff argued the higher baseline better reflects recent development trends and reduces the risk of treating volatile development revenue as permanently recurring.

Other recommended changes and budget moves include: - Moving utility-billing operations and the associated administrative transfer from the general fund into a dedicated Utility Billing/CIS fund, which reduces the general fund’s ongoing expenses by roughly $2 million but preserves the revenue transfers from utilities to the new fund. - Increasing the broadband franchise fee from 1 percent toward 4 percent as a financial-policy change; staff estimated a revenue gain of about $715,000 (a policy for council consideration). - Adjusting staffing and reserves. Staff proposed using $3.5 million of fund balance to strengthen general-fund reserves and projected that, absent any use of the stabilization reserve, general-fund reserves could be fully funded to policy levels in 2026.

Public-safety and budget pressures: Moy and staff warned the public-safety fund is under pressure because it depends on sales and use tax and because personnel costs make up the large majority of the fund’s ongoing expenses. Attachment E in the council packet showed a 10-year pro forma indicating fund-balance drawdowns if sales-tax growth does not exceed the conservative assumptions in the pro forma.

Annexation note: Council also directed staff earlier in the session to pursue enclave annexation of two unincorporated dispensaries inside the city. Finance staff said the annexation and a proposed concurrent code change would shift previously uncollected local sales and use tax into city funds (general fund and restricted funds such as public safety and open space) and that staff would return with revenue estimates and a budget impact analysis.

Next steps: Staff said council would receive the IGAs (PRPA documents) for review next week and would continue budget work through the fall; precinct-level certified property values and September/October sales-tax returns will determine some of the final revenue assumptions before adoption.

Sources: Presentation and Q&A by Sandra Cifuentes and Theresa Moy at the Sept. 2 Longmont City Council study session; budget attachments in the council packet.