County budget staff to base next draft on voter-approved tax rate, commissioners agree

Loading...

Summary

County budget presenters recommended basing the upcoming fiscal-year budget on the voter-approved tax rate rather than the no-new-revenue rate; commissioners discussed fund-balance limits, contingency accounting and potential cuts to cover a roughly $400,000–$600,000 projected shortfall.

County officials said they will prepare budget projections using the “voter-approved” tax-rate scenario rather than the lower “no new revenue” calculation, after a discussion about how that choice affects available revenue and required cuts. The meeting focused on how to present expenses that will be paid from existing banked funds, reimbursements expected after expenditures, and the county’s year-end fund balance.

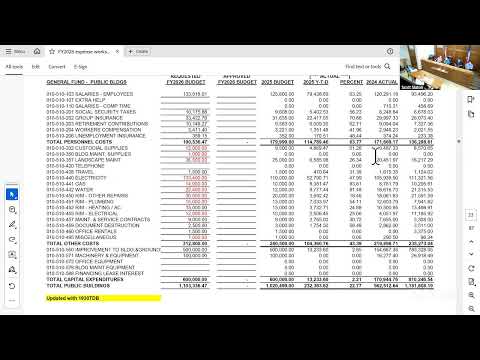

Why it matters: the tax-rate baseline governs how much recurring revenue the county projects before using reserves, contingency or one-time funds. Choosing the voter-approved rate raises projected general-fund revenue by roughly $1.5 million compared with the no-new-revenue calculation, according to the presenter’s worksheet.

Budget staff outlined three revenue scenarios: a no-new-revenue rate that would produce about $18.0 million for the general fund; a voter-approved rate that would produce roughly $19.2 million; and the current effective rate, near 30 cents per $100 valuation. Staff noted assessed valuation changes, frozen taxes (tax ceilings for certain seniors), and an allowance for delinquency when estimating levy receipts.

Commissioners discussed the composition of the revenue picture. The presenter said some line-item expenditures shown in the draft budget will be paid from money already on deposit (for example ARPA and other restricted funds), producing a timing mismatch between budgeted expenses and the receipts that financed those expenses. Commissioners asked staff to clarify which budgeted expenditures are funded from prior-year receipts or reimbursements, and which are recurring obligations.

The group reviewed projected budget increases including a 3% personnel cost step, planned new positions, and other recurring expense increases. Staff estimated roughly $500,000–$800,000 in expected cost increases across regular accounts and noted the voter-approved rate scenario would cover a significant portion of the new personnel costs.

Several commissioners said they prefer to start budgeting using the voter-approved rate so the court can see the smallest amount of cuts required; others emphasized conservative trimming and asked that contingency and fund-balance assumptions be explicit. Staff also said the county’s audited fund balance was approximately $12 million at the end of the last fiscal year, but that the usable portion and the effect of planned transfers (for example to the Paul Michael building) needed clarification.

The court did not take a formal vote during the workshop. Instead, commissioners reached an operational decision to use the voter-approved rate for the next draft and asked staff to: (1) identify and segregate expenditures that will be paid from existing restricted or one-time funds; (2) show contingency and fund-balance assumptions clearly; and (3) return with revised detail that reflects those clarifications.

Looking ahead: staff said they will meet with the auditor and accounting staff to reconcile transfers and fund accounting under the new software, then present updated numbers at the next workshop. No ordinance or formal tax-rate action was taken at the meeting.