Charter commission proposes new accountability rules for entities that receive voter‑approved levies

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

One ballot issue would require entities that seek voter‑approved income or property tax money to meet one of four governance accountability options — elected by city voters, elected by school district voters, appointed by council, or a council‑approved alternative — before a levy can appear on the ballot.

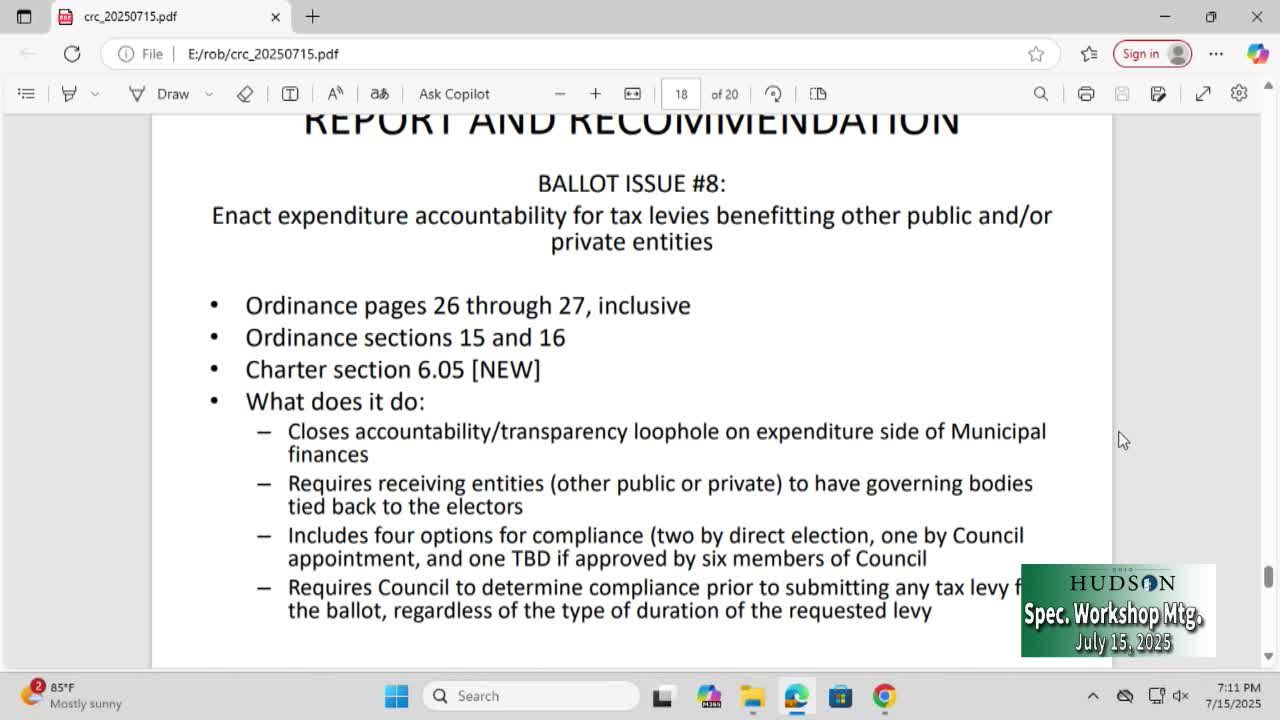

Ballot issue 8, as presented July 15 by the Charter Review Commission, would set new charter conditions for entities that seek public money raised by voter‑approved income or property tax measures.

The commission framed the proposal as a response to public questions about accountability for outside entities that receive city‑raised tax dollars. Rob Kegler said the commission “peeled the onion” to consider both revenue inflows (for example, income tax receipts that were designated to the school district after flood response, and property tax money that funds the Hudson Library and Historical Society) and expenditure outflows — money the city would send to another entity.

Under the proposed charter language, any entity that requests voter‑approved income or property tax revenue would have to meet one of four governance options for its governing board: (1) the governing board is elected by the electors of the city; (2) the governing board is elected by the electors of the school district (which the commission noted is predominantly city voters); (3) the governing board is appointed by Hudson City Council; or (4) council may approve an alternative governance structure by six affirmative votes if council finds it provides sufficient accountability to Hudson electors for the term of the levy.

The commission explained the requirement would be tied to the term of a levy so council could review whether an alternative approach worked when the measure next returned to the ballot. The proposal lists the four options to give councils and prospective levy sponsors a clear menu of accountability mechanisms.

Why it matters: the rule is intended to increase direct accountability of entities that receive city‑raised tax dollars by ensuring their governing structure links back to Hudson electors or is approved by council. The change could affect the way the city and outside organizations structure boards when they seek voter support for levies.

Council response and next steps: council members asked for clarifying materials about logistics — for example, how an association library’s board election process differs from a school board election — and asked staff to include detailed, voter‑facing explanations before the November election. The commission emphasized council would have discretion under option four to approve alternative accountability structures if at least six councilmembers supported the approach; that approval would apply only for the term of the levy.