Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

House Revenue Committee hears estate tax options; LRO warns threshold, portability changes can materially affect revenue

Summary

Legislative Revenue Office staff briefed the House Committee on Revenue on May 20 about how changes to Oregon's estate tax exclusion, portability, and rate structure would affect state revenue, timing of receipts and administrative requirements.

The House Committee on Revenue on May 20 heard an informational briefing on estate tax policy options that could substantially change state revenue collections, the Legislative Revenue Office told lawmakers.

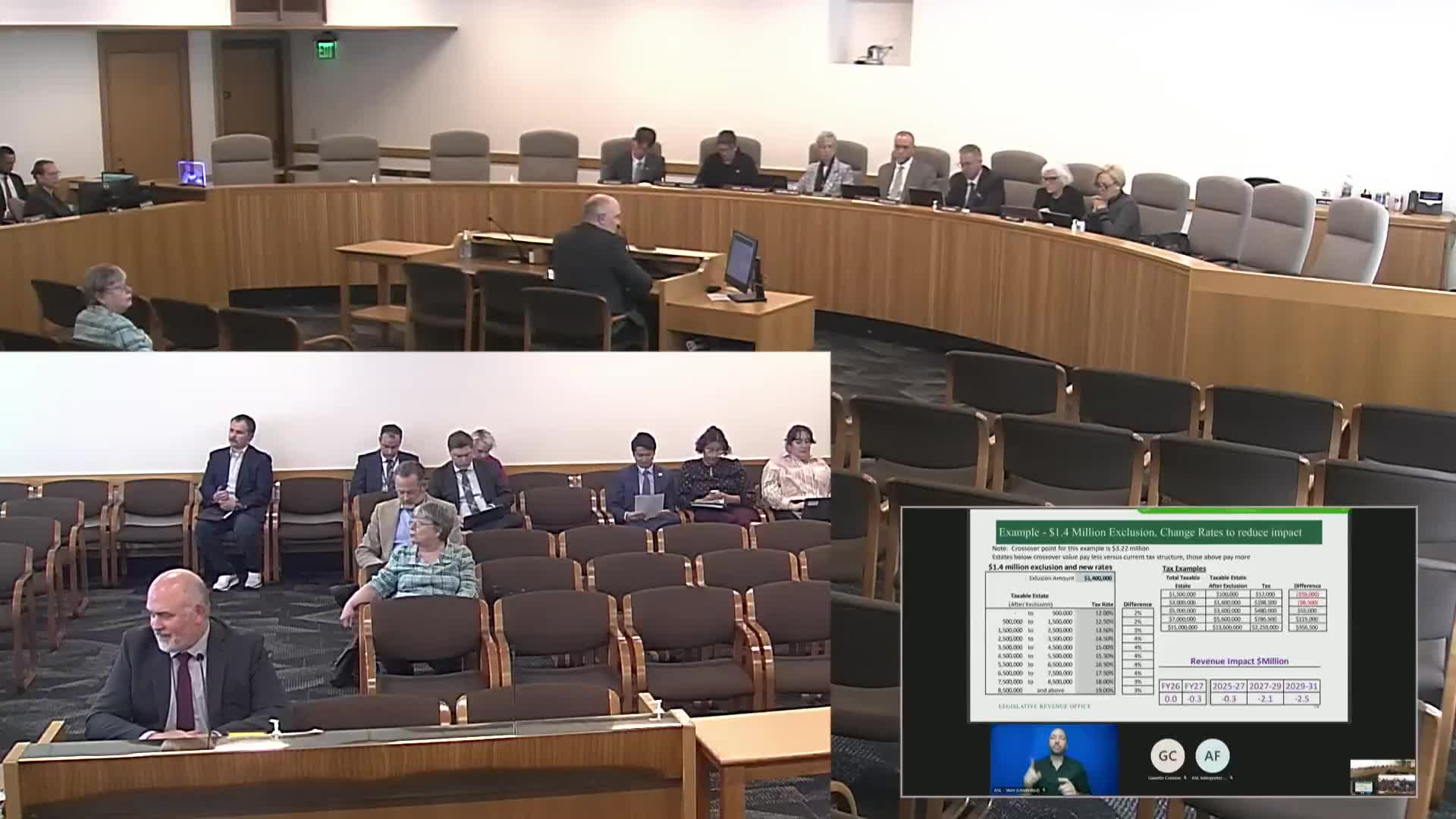

John Hart of the Legislative Revenue Office said the state's current estate tax includes a $1,000,000 exclusion and that changing that exclusion or indexing it for inflation would affect taxpayers across the distribution and change revenue materially. "If the threshold is increased by $100,000 that first $100,000 reduces revenue by about 5.7%," Hart said, noting each additional $100,000 produces smaller reductions.

The briefing matters because revenue from the estate tax does not flow to the state general fund immediately after a policy change. Hart said estate tax returns are due 12 months after a decedent's death, with an automatic six-month extension often used; in his modelling, roughly 35% of liability tied to deaths in a calendar year arrives in the first…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat