Tariffs, supply-chain pinch points and rare earth licensing raise risks for Michigan auto jobs, experts say

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

University of Michigan and Federal Reserve Detroit analysts told the CREC that tariffs and related policy actions could cut U.S. light-vehicle production, cost Michigan thousands of jobs and create new supply-chain vulnerabilities, including rare-earth processing controlled by China.

Speakers at the CREC on May 20 warned that new tariffs and retaliatory measures could reduce U.S. light-vehicle production, increase vehicle prices and raise substantial risks for Michigan's auto-dependent labor market.

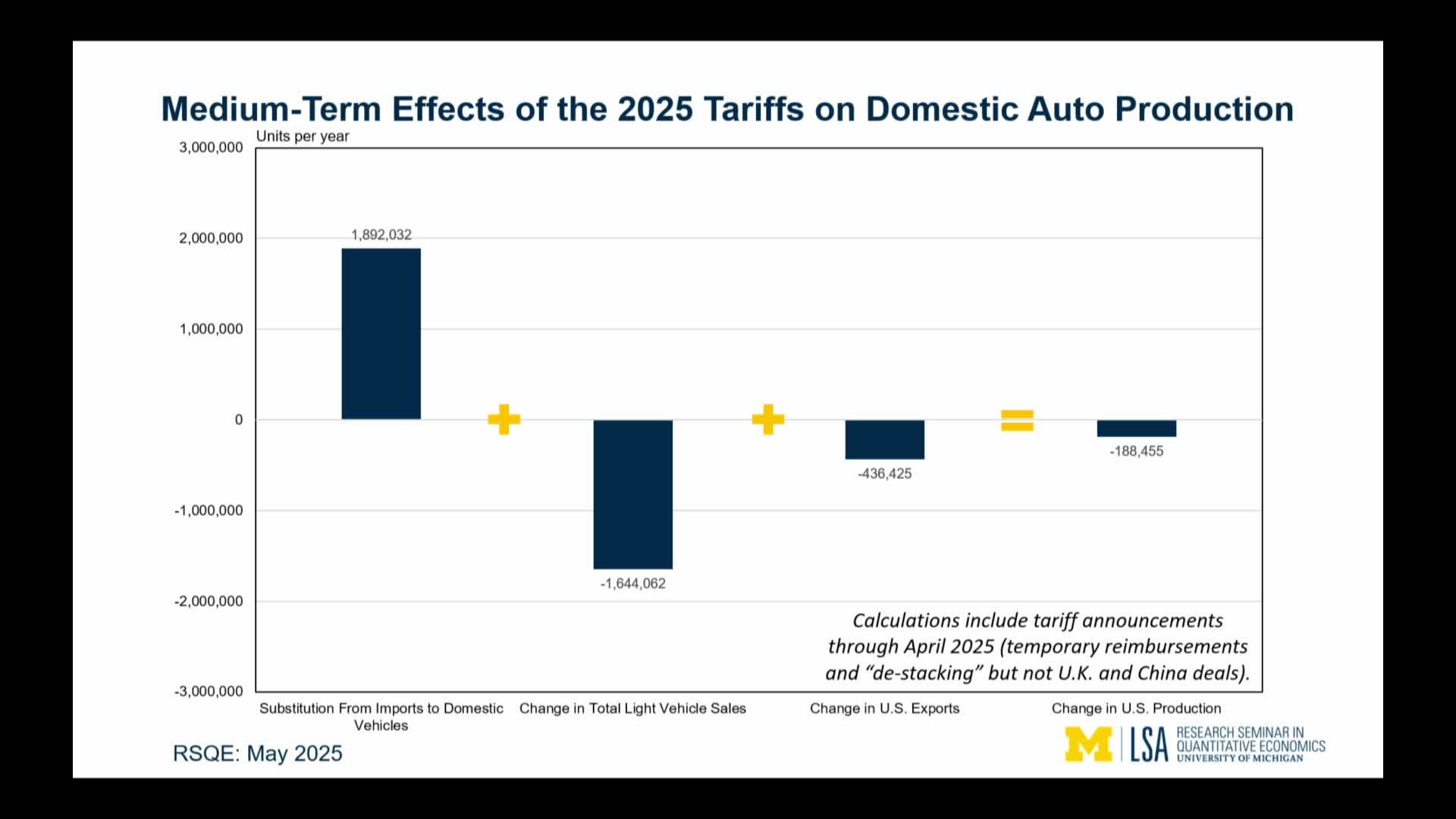

Gabe Ehrlich of the University of Michigan's RSQE presented a model of tariff effects that accounted for consumer substitution, higher domestic production costs and retaliatory tariffs. "We estimate that the tariffs will reduce U. S. Light vehicle production by nearly 200,000 units per year," Ehrlich said, noting an estimated average effective tariff on imported vehicles of about 21.6 percent and an estimated domestic production cost rise of roughly 5.7 percent under the scenario he used.

Ehrlich translated that modeling into Michigan impacts: a 1.8 percent decline in domestic auto production would roughly equal a loss of about 3,300 direct auto-sector jobs and, using the center's multiplier, about 13,000 total statewide job losses if effects pass through proportionally.

Kristen Gajek, automotive policy advisor at the Federal Reserve Bank of Chicago's Detroit branch, described near-term supply-chain fragility and policy details that could amplify impacts. She highlighted licensing of rare-earth exports and processing dominance in China, saying, "China controls 92% of the processing for these minerals," and added that licensing can be dynamically revoked, creating a pinch point that reaches beyond auto motors to electronics and defense supply chains.

Gajek and other presenters emphasized the uneven effects across the Michigan auto sector. Michigan is disproportionately concentrated in full-size pickup and large SUV production, the higher-margin vehicles that have supported the state's manufacturing footprint; however, Gajek warned that higher costs, lost incentives and faster automation could blunt reshoring benefits. She noted that some firms are accelerating automation bids to manage labor and cost pressures.

Both presenters cautioned that assumptions matter: Ehrlich framed his results as medium-run (three-to-five-year) impacts that could be larger in the short run if suppliers fail before adjustments occur. Gajek stressed that partial tariff reimbursements and exemptions will affect timing and magnitude, but the evolving policy mix leaves large upside and downside risks for Michigan production, employment and revenue.

CREC principals and staff will use these analyses when updating revenue forecasts and considering the state's exposure to national trade policy shifts.