Get AI Briefings, Transcripts & Alerts on Local & National Government Meetings — Forever.

Muskegon County auditor issues clean opinion; general fund balance rises to $17.5 million

Summary

An external auditor presented an unmodified (clean) opinion for the year ended Sept. 30, 2024, and reported a $854,203 net increase in the county general fund, leaving an ending fund balance of $17,545,009 and an estimated 26.6% reserve level.

An external audit of Muskegon County’s financial statements for the year ended Sept. 30, 2024, returned an unmodified — or “clean” — opinion, the county’s auditor told commissioners on April 22.

Paul Matz, a partner at the county’s audit firm, told the Board of Commissioners that the audit found no reportable findings or significant deficiencies in internal controls and that the county’s financial statements are “accurately stated in all material respects.” Angela Koschevsky, Muskegon County finance director, introduced the presentation and fielded follow-up questions.

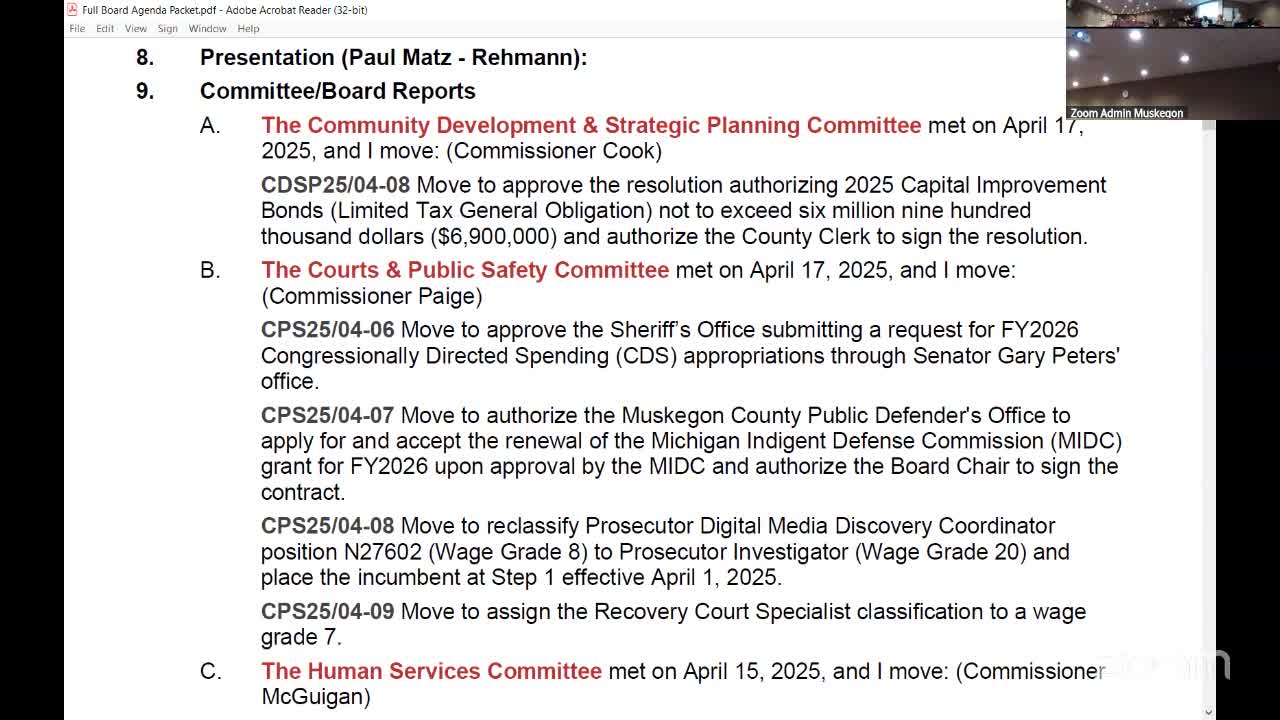

The auditor highlighted two places in the financial report for board review: a transmittal letter on page 3 summarizing accomplishments and a management’s discussion and analysis section beginning on page 18 that offers a concise, finance-focused overview. Matz pointed commissioners to the statement of revenues, expenditures and changes in fund balance (page 38) and said the general fund showed a net increase in fund balance of $854,203 for the year, producing an ending fund balance of $17,545,009. He noted the county’s target range for minimum unassigned fund balance is 14 to 19 percent and said the county’s rate at the end of fiscal 2024 was about 26.6 percent.

Matz also described the budgetary comparison schedules, which show the original budget, the final amended budget and the actual results, and said the actual increase in fund balance was an improvement over the final budget projection. He added that the audit includes compliance testing for federal funds administered by the county and that no compliance exceptions were identified.

Koschevsky and Matz both praised county staff for preparedness, saying the audit work began on the agreed start date and the finance team was responsive to requests. A commissioner complimented Koschevsky’s leadership since she took the finance director role.

No formal board action was recorded during the presentation; the report was given for the board’s information and review. Commissioners were encouraged to read the transmittal letter and management’s discussion and analysis for more narrative context.

The auditor said the full financial statements run more than 200 pages and include HealthWest as a separate presentation. He invited commissioners to request more detail on any specific item.

The county provided printed copies of the financial statements to commissioners at the meeting.