Centerton council adopts impact-fee ordinance after months of debate

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

The Centerton City Council on March 11 approved Ordinance 2025-02 establishing impact fees on new development after staff presentations, developer input and public comments; the ordinance will take effect after the required 30-day waiting period.

The Centerton City Council on March 11 adopted Ordinance 2025-02 to set impact fees on new development, approving the measure by roll call after an extended staff presentation and public comment period.

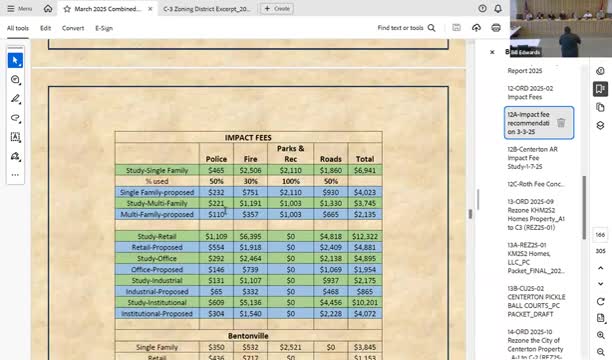

City staff framed the measure as a way to recover costs of growth-related infrastructure. Anthony, a city staff member who led the presentation, said he spoke with neighboring cities and developers while shaping the proposal and noted the study team "recommendation was to throw out fire altogether" before the staff refined the proposed rates. He told council members he favored spreading fees across categories rather than eliminating a category entirely.

Why it matters: Centerton has fast population growth, expanding subdivisions and major commercial proposals. Council and several speakers said impact fees are intended to ensure new development helps pay for roads, water and public-safety capacity rather than shifting the burden to existing taxpayers.

Discussion and public comments focused on several points: whether fees should be collected at permit issuance (the "front end") or after occupancy, how fees affect smaller builders and buyers, credits for developer-funded road or utility work, and a proposed review timeline. Anthony told the council the city staff recommends collecting fees at the front end to reduce the risk of nonpayment later and said finance staff will need to create separate accounting funds for each fee type.

Multiple builders and a large local developer, Gavin Edwards, who identified himself as "developer of Big Sky" and a longtime local builder, told the council most builders expect some fee and can accept a moderate, predictable charge. Gavin Edwards said, "I think the impact fee is needed." Several builders and staff also noted that the timing and availability of sewer capacity is the more immediate constraint on new construction.

A member of the public, Chris Mooney, asked the council to focus zoning decisions on land use, but in his remarks he also raised concerns about compatibility of commercial uses along a two-lane, higher-speed corridor — comments staff and council referenced while discussing potential nonresidential impacts and credits.

Key technical points recorded in the meeting: staff said developer contributions for direct improvements can be credited against impact-fee obligations (for example, the presentation suggested large nonresidential projects could see credits that reduced modeled fees from roughly $500,000–$650,000 toward about $400,000 when they invest in roadwork). Councilors and staff discussed a three-year review of fees and whether a land-use attorney should review the final ordinance before implementation.

Formal action: A motion to adopt Ordinance 2025-02 carried on a unanimous roll call vote (Thompson, Cowger, Henson, Reed, Hagen and Miles voting yes). The ordinance is subject to the 30-day waiting period required before taking effect. Staff said, if adopted, the city would create individual impact-fee accounts and report revenues and expenditures to council monthly.

The council and staff repeatedly emphasized that the fees and administration are not final technical settings; staff recommended sending the ordinance and fee schedules to a land-use attorney for review and returning to council with any recommended legal refinements. Councilors also noted the city could adjust rates later (requiring a new study to increase rates) and that staff will monitor collections and bring the topic back as part of routine financial reporting.