Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

City staff outlines Bay City budget process, fund types and reserve policy

Summary

A city finance presenter walked commissioners through the annual budget calendar, fund accounting, reserve policy and key revenue and expenditure categories ahead of the 2025–26 budget cycle.

At the Feb. 3 Bay City City Commission meeting, a staff member presented “Budget 101,” an overview of the city’s annual budget process, fund accounting and key policy limits for the coming fiscal year.

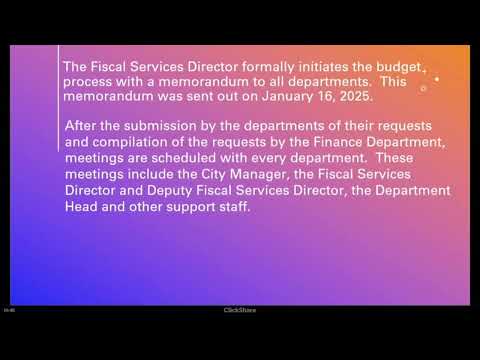

The presenter said the city charter requires the city manager to prepare and submit an annual budget and capital program to the commission and noted a 2004 resolution setting the delivery timing for the proposed budget. The presentation described a process that begins with a January memo from finance, department-level submissions in New World Financials, personnel cost compilations by Human Resources and a line-by-line review of departmental submissions with the city manager ahead of a City Manager Proposed Budget delivered in April.

Why it matters: the presenter said the commission follows a fund-balance policy that aims to keep the general fund reserve between 15% and 20% of the prior year’s amended expenditures. For the coming fiscal year the presenter said that range would…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat