Oak Harbor staff outlines three business-and-occupation tax options to fund marina, parks and public safety

Loading...

Summary

City staff presented three thresholds for a local business-and-occupation (B&O) tax, with projected annual revenues ranging from about $793,000 to $1.87 million depending on the threshold; staff said revenues could help pay for marina dredging, a parks-and-recreation facility and police facility needs.

David, a city staff member, presented three options for a local business-and-occupation (B&O) tax during an Oak Harbor online informational session. He said the tax would be a local option that requires council approval and described estimated revenues, exemption rules, filing cadence and an example implementation timeline.

The presentation matters because council members have identified several capital and maintenance needs — including marina dredging and repairs, a potential new parks and recreation facility and deferred maintenance at the police station — and staff told attendees they are exploring local revenue options to help pay for them.

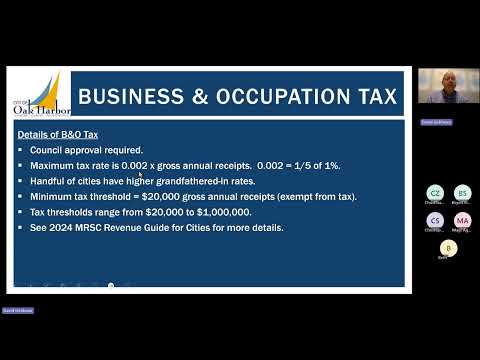

Staff explained the B&O rate would follow the state cap for most jurisdictions: 0.002 of gross annual receipts (one‑fifth of 1 percent) unless a city had a grandfathered higher rate. Three threshold options were shown:

- Option 1: Exempt the first $5,000,000 of gross receipts. Based on Department of Revenue data, that threshold would apply to 27 businesses (about 1.2% of Oak Harbor businesses) and generate an estimated $793,000 annually. The largest single business under this estimate would pay as much as $132,000 per year; the median annual tax among the 27 businesses was shown as about $11,121.

- Option 2: Exempt the first $1,000,000 of gross receipts. That threshold was estimated to apply to about 178 businesses (8.2% of businesses) and generate roughly $1.3 million annually; the median annual tax in that cohort was shown as about $1,664.

- Option 3: Exempt the first $100,000 of gross receipts. Staff estimated this would affect about 555 businesses (about 26% of businesses) and raise about $1.87 million annually; the typical (median) annual tax for affected businesses was shown as about $800.

David emphasized the numbers are estimates and depend on real‑time business earnings and the threshold chosen. He said the city built the state‑required exemptions and deductions into the draft code language and would follow state rules for late fees, underpayments and appeals (Revised Code of Washington provisions apply to administrative processes).

Staff described filing and payment mechanics: returns would be proposed as quarterly, with returns due 30 days after the end of the quarter, and the city would prefer electronic payments. The presentation noted some cities allow businesses that expect to remain under the threshold to file a one‑time exemption attestation to avoid submitting a return every quarter.

On taxable items and exemptions, David read state guidance: investment income and some other items are exempt, but “no exemption is permitted by the state for amounts received as commissions on real estate sales,” meaning real estate sales commissions would be subject to the B&O tax under state law. He also cited MRSC (Municipal Research and Services Center) research that B&O taxes are often unpopular with businesses because they are assessed on gross receipts rather than net income.

Staff proposed giving businesses a preparation window if the council approves a tax: roughly six months between passage and the effective date, and then the first quarterly return would be due after the end of that initial quarter (staff used example dates to illustrate how the timing would work). David said the council would still need to decide whether to pursue the tax and that staff are also exploring other funding mechanisms, such as a port district for marina funding and state or federal grants for capital projects.

Attendees asked practical questions. A resident who identified herself as a realtor asked whether a brokerage or individual agents would be taxed; staff responded that commissions are taxable under state law. Another attendee asked about timing and location for a parks and rec facility; staff said the city has a state‑funded feasibility study underway to determine optimal siting and public input opportunities.

No formal council vote occurred at the informational session; staff said they would notify attendees if and when the council schedules a B&O discussion or decision and publish agenda materials and minutes.

The presentation repeatedly cautioned that the revenue figures were estimates based on Department of Revenue data and that the council must adopt any local tax and related municipal code language before any charge would be imposed.