Central staff warn of an expanding 2027 general fund deficit; underspend assumptions and jumpstart fund volatility highlighted

Loading...

Summary

Central staff delivered a detailed general fund health check, showing a growing projected deficit in 2027 and flagging reliance on underspend assumptions and volatility in payroll‑expense (jumpstart) forecasts as key risks to sustainability.

Central staff presented a detailed general fund balancing analysis on Oct. 15 that showed the city's multi‑year fiscal outlook has worsened since the endorsed budget, with a projected deficit materially growing in 2027 and beyond.

Tom Mike Sell, lead analyst for Central Staff, told the committee the review was "the full physical exam for the general fund," tracing how adjustments since last fall — including technical updates, changes to transfers from the payroll expense tax (jumpstart) fund, and the executive's new revenue proposals — alter the city's projected balances.

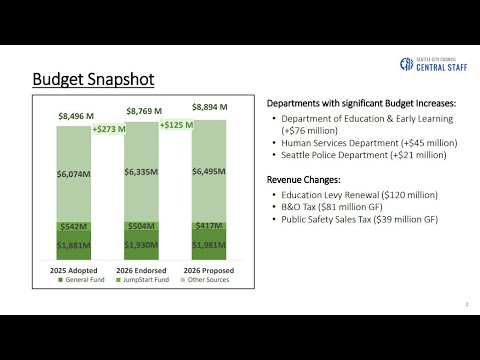

Key findings and risks - Starting balance changes: Central Staff said the 2026 starting point improved modestly due to year‑end technical adjustments, but those one‑time gains are already allocated in the proposed adjustments. - Jumpstart payroll expense tax risk: An August forecast downgrade sharply reduced payroll‑expense tax projections, forcing the mayor's team to reduce the planned transfer from the jumpstart fund to the general fund; that action protected programs in the jumpstart fund but contributed to a general fund shortfall early in the analysis. - New revenues partially offset shortfalls: Central Staff incorporated the B&O tax restructure and a public safety sales tax, which together provide substantial resources in 2026; after layering those in, the general fund returns to positive balance for 2026 in the proposed package but the out‑year picture weakens. - Underspend assumptions: Staff noted a long‑running practice of expecting departments to underspend adopted appropriations. Central Staff showed historical underspend exceeded prior assumptions in many years and warned that the proposed plan now relies on a $10,000,000 underspend assumption in out years. Central Staff suggested the council consider whether that practice should be formalized, revised or studied because it affects transparency and future flexibility. - Reserves and stabilization: The city's emergency fund is fully funded under policy rules; however Central Staff pointed out a discrepancy between the municipal code's guidance for the revenue stabilization deposit and the proposed transfer amount, leaving about $4.7 million less in the stabilization transfer than a stricter reading of code would indicate.

Multi‑year outlook and options Central Staff concluded the mayor's 2026 proposal is balanced for the upcoming year largely by using new revenues and one‑time technical adjustments, but that "the budget on a projected basis is deeply out of balance for 2027," language used by Director Ben Noble in the meeting. Staff framed several policy choices for council, including increasing reserves, formalizing or revising the underspend practice, reassigning one‑time vs. ongoing status for B&O‑backfill items, or reallocating new tax proceeds to shore up the 2027 deficit rather than fund new initiatives.

Ending: Central Staff will provide updated projections after next week's revenue forecast; the committee's upcoming amendment window and council proposals will determine whether the city reduces the projected 2027 deficit or postpones some spending items.