Retirement trust approves small‑cap manager swap, rebalances fixed income

Loading...

Summary

The St. Mary's County Retirement Benefit Trust Committee voted this October to move $1.2 million from a John Hancock small‑cap fund into the American Beacon small‑cap growth fund and to reallocate $1.5 million of fixed‑income assets to broaden duration and credit exposure.

The St. Mary's County Retirement Benefit Trust Committee voted this October in the Chesapeake Building to replace its John Hancock small‑cap allocation and to adjust fixed‑income managers, moving $1.2 million from the John Hancock Small Cap Dynamic Growth Fund into the American Beacon small‑cap growth fund and shifting $1.5 million out of the Lord Abbott short‑duration sleeve into two core investment‑grade managers.

The swap and rebalancing were presented by Patrick Wing, presenter, who led the committee through a manager search that produced two finalists for the small‑cap growth sleeve: Emerald Growth Fund and American Beacon (sub‑advised by Stevens Investment Management). Wing summarized the choice by contrasting strategy and recent performance, and noted the committee’s existing investment was a John Hancock fund that had been closed and rolled into a different John Hancock product with a sub‑advisor the investment team has not fully vetted. "From a fiduciary perspective, I'm just gonna come out and say we would not recommend it because we don't know enough to recommend it to you," Wing said of the rolled‑into John Hancock fund.

Why it matters: the committee’s small‑cap sleeve represents a tactical part of the U.S. equity allocation and the committee agreed the change should be a straight swap rather than an asset‑allocation shift. The fixed‑income rebalancing increases exposure to broader investment‑grade strategies and modestly lengthens duration, positioning the trust to benefit more if market yields decline.

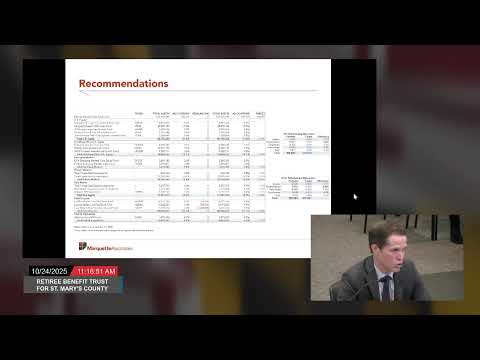

Key details from the consultant's presentation: - Manager choices: Emerald Growth Fund (more concentrated, higher recent returns, about 78 basis points fee reported in the presentation) and American Beacon (positioned as a blend of "core growth" and "earnings catalyst" stocks, 97 basis points fee in the presentation). Wing described Emerald as the more aggressive option and American Beacon as more defensive and closer to the Russell-style exposures the trust has historically used. "If this environment continues, Emerald is probably gonna do the best," Wing said. "If we get a more discerning market environment, then I would expect the flip side of that." - Fees and scale: presentation materials cited Emerald's expense ratio near 78 basis points and American Beacon near 97 basis points; materials also noted differences in assets under management and portfolio concentration. - Rationale to remove John Hancock: the existing John Hancock vehicle had been closed and its assets rolled into a different John Hancock fund sub‑advised by a firm the consultant had not completed due diligence on; Wing said the team could not recommend that sub‑advised product without more work.

Committee action and implementation: Commissioner Scott Ostrow moved to "accept the market's report and approve the recommendation as presented with the addition of moving the 1,200,000.0 from John Hancock's small cap dynamic to the American Beacon." The motion was seconded by Catherine Pratzen, director of human resources and board member, and passed by voice vote. The recommendation calls for a full liquidation of the John Hancock position and for the $1.2 million to be invested in American Beacon; any sale proceeds beyond $1.2 million were described as expected to flow to cash pending final settlement.

Separately, the consultant recommended and the committee approved rebalancing within fixed income: $1.5 million to be removed from Lord Abbott and split equally ($750,000 each) into the Grilling and Reams fund and into Loomis sales (as named in the meeting materials). Wing explained the change shifts assets from a 1–3 year focused sleeve into core investment‑grade managers to gain modestly more duration and better position the portfolio for anticipated Fed rate moves.

The committee discussed whether to choose the more aggressive Emerald fund or the more defensive American Beacon. Several trustees expressed a preference for staying closer to the trust’s historic risk profile given ongoing health‑care disbursements; Commissioner Ostrow and others favored American Beacon as a middle ground. Wing said the allocation being moved represents roughly 1% of the total trust and can be changed in the future if the committee chooses.

The committee's motion recorded the decision and directed staff to execute the liquidations and purchases through customary custodial and trading processes. No change to the plan's overall strategic asset allocation targets was made; the actions were swaps within existing sleeves.

The meeting also included routine portfolio updates on legacy private markets and summary performance figures for the trust’s private real estate, private equity and private debt holdings through the second quarter; those accounting‑style data points were presented as context for the allocation discussion but did not change policy.

The committee voted unanimously on the motion to approve the manager swap and rebalancing. The plan administrator noted the next scheduled meeting for 2025 is Dec. 5, 2025.