Rock County presents balanced 2026 recommended budget with 2.5% COLA and larger capital plan

Loading...

Summary

County staff presented a balanced 2026 recommended budget that includes a 2.5% COLA, a 7.05% levy increase, $3.2 million of sales tax assigned to highway fund to repay an advance, and proposed borrowing for highway and park projects; timelines for appeals and adoption were given.

County staff and officials presented the Rock County recommended budget for 2026 and outlined its broad components, including operating levy, debt strategy and next steps in the review process.

Key points of the recommendation: Presenters said the recommended budget is balanced and includes a 2.5% cost-of-living adjustment for employees. The presentation cited a levy increase of 7.05% and listed components described by staff: “just over $69,000,000 in our operating levy,” a figure the presenter said was accompanied by “about 9.7 attributed to our debt service portion of the levy.” The recommended budget also includes a $289,000 limited levy item and $1,400,000 for the Prairie Lakes Library System (both described as limited-levy amounts by staff).

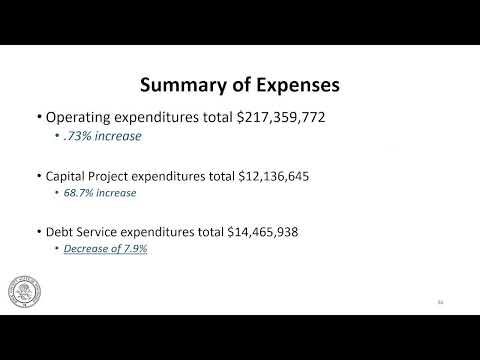

Debt and capital: Staff said they are assigning $3,200,000 of sales-tax receipts to the highway fund to begin repaying an advance from the general fund, and recommended about $4,700,000 in borrowing for highway and park projects. The presenters described recent uses of one-time funds to offset debt levy in prior years and said the 2026 recommended budget uses about $2,700,000 of one-time debt-fund balances to reduce near-term levy pressure, but noted the underlying debt levy gap remains a structural issue.

Revenue, inflation and staffing: Presenters showed that equalized value in Rock County rose by about 7% year over year (which staff broke into roughly 5% valuation appreciation and 2% new construction). Staff said overall operating expenses in the proposed budget increase about 2.45% and they compared that to a published inflation figure of 2.7% for the year-over-year period cited. The recommended budget also reports a modest net headcount change (presenters described net position growth of 0.3%). Presenters emphasized that the county receives a substantial share of revenue from intergovernmental sources (they cited roughly 46% of revenues coming from intergovernmental sources) and noted sales tax is a major revenue source.

Timing and process: Staff outlined the review schedule: the board will take questions and the county will post the full recommended budget online. Important dates stated in the presentation included a detailed review meeting on September 30, committee budget reviews in October, the public hearing on the 2026 budget on October 30, the finance-committee appeals process on November 6, and a tentative final budget adoption on November 12.

What was not decided: The presentation described the administrator’s recommended budget and provided information; the Board did not adopt the budget during the meeting. The recommended budget contains assumptions and recommended actions (for example, borrowing for capital and sales-tax assignments) that would require subsequent committee review and final approval by the County Board.

Ending: Staff left printed copies and said the electronic document would be posted with hyperlinks. They also provided written instructions for filing budget appeals and emphasized transparency by including department requests and capital plans in the document the board will review in coming weeks.