Alpena County board receives unmodified fiscal 2024 audit; auditors flag internal-control items

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

External auditors issued an unmodified opinion on Alpena County's 2024 financial statements and presented required communications about internal-control items, proposed adjustments and pension liabilities; the board voted to receive and file the audit.

The Alpena County Board of Commissioners received and filed the county’s fiscal year 2024 audit after an external auditor presented the report at Tuesday’s meeting.

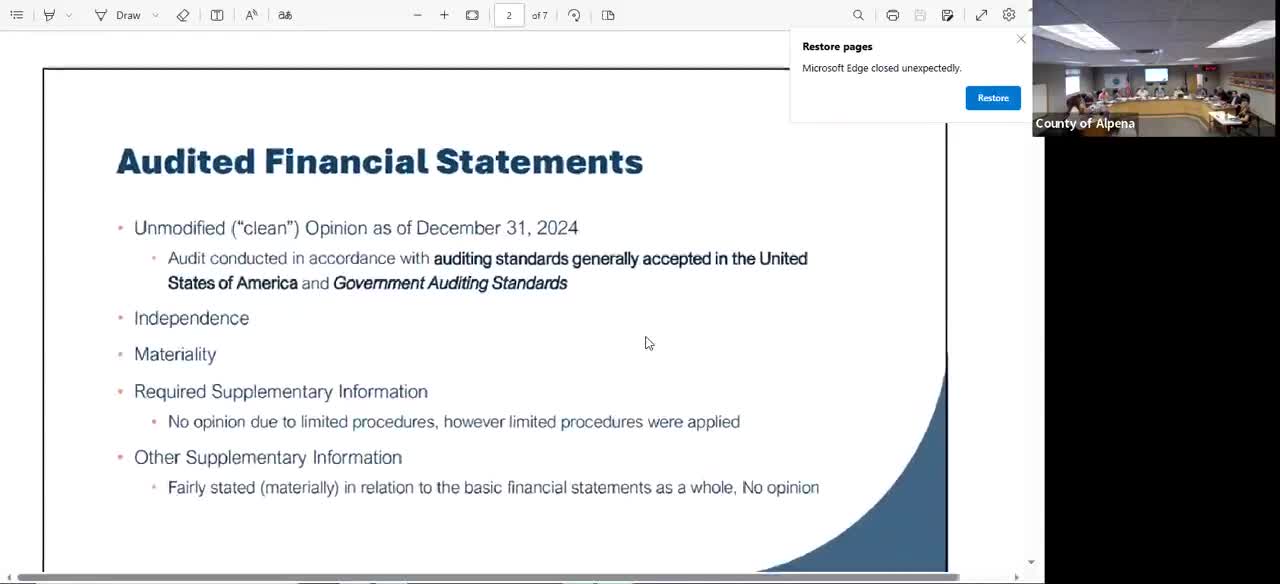

The auditor, identified in the meeting as Chelsea, said the audit included an unmodified opinion — the highest level of assurance auditors can give — meaning the financial statements were presented fairly in all material respects. “I am pleased to say that you were issued an unmodified opinion,” Chelsea told the board.

The auditor summarized key points from the report: assets increased by nearly $21.2 million, driven largely by capital additions tied to the airport runway rehabilitation project; liabilities decreased by about $1.2 million as previously unearned ARPA revenue was spent; and the county’s net position increased by roughly $22.8 million. On the modified-accrual (fund) basis, the general fund ended the year with a fund balance of about $4.3 million and an unassigned balance equating to roughly 108 days of expenditures, comfortably above GFOA guidance.

Auditors identified internal-control matters and required communications. They described concerns about oversight of accounts payable — invoices routed to multiple departments that might not reach the clerk’s office and therefore could affect accruals — and noted material audit adjustments that management accepted. The audit also highlighted common findings such as segregation of duties and financial statement preparation. The county’s pension net liability was reported at about $10.2 million as of Dec. 31, 2024.

The board moved to receive and file the audit; a roll-call vote approved the motion.

Why it matters: An unmodified opinion signals that auditors found the county’s financial statements reliable for the year ended Dec. 31, 2024, but the internal-control items and proposed adjustments identify areas for process improvement and oversight. The auditor advised continuing to make actuarially determined pension contributions as recommended by the retirement system fiduciary.