TRS outlines disability, survivor benefits, health coverage and post‑retirement work rules

Loading...

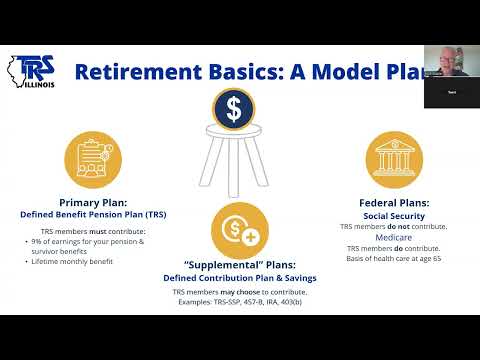

Summary

TRS explained eligibility for temporary disability benefits, how the 8%/1% contribution buckets fund retirement and survivor benefits, guidance on beneficiary designations, health insurance options (TRIP and TRAIL) and rules for returning to work after retirement.

TRS presenters summarized disability and survivor protections, health insurance options for retirees, and post‑retirement employment rules for members of the Teachers' Retirement System.

Disability: TRS’s disability benefit is available only to active members with at least three years of nonconcurrent service credit across TRS, state universities, SERS or IMRF. To qualify, two state‑licensed physicians must certify that the member cannot perform their job duties and must agree on a diagnosis (one physician suffices for pregnancy‑related bed‑rest cases). Temporary disability pays 40% of the contractual rate of pay while the member receives the benefit and TRS grants service credit for that period, TRS said.

Death and survivor benefits: TRS described how the member contribution is split: 8% goes to an 8% retirement bucket used to fund retirement checks, and 1% to a survivor bucket. The survivor designation (dependent vs nondependent) determines benefit type. A dependent spouse (married at least one year) or dependent child (under 22, unmarried and full‑time student; or adult disabled child) may receive half of the member’s monthly benefit under Tier 1 rules: spouses receive that monthly survivor benefit for life; dependent children receive it only while they meet dependency criteria. Nondependent beneficiaries receive a lump sum equal to the balance in the 1% bucket. TRS noted members may request a refund of their 1% survivor contributions during life (a taxable distribution), but doing so removes survivor payments for future beneficiaries unless the member returns to active service and repays the amounts.

Beneficiary designation: TRS encouraged members to complete beneficiary designation forms and described an option (checking Section 3) that directs TRS to pay dependent beneficiaries as determined at death rather than naming specific individuals now. Alternatively, members may name primary and alternate beneficiaries in sections 4 and 5.

Health insurance (TRIP and TRAIL): TRS explained two programs: TRIP (Teachers’ Retirement Insurance Program) provides retiree medical, prescription, dental and vision coverage for non‑Medicare retirees; TRAIL (Total Retiree Advantage Illinois) is the Medicare Advantage option for Medicare‑eligible beneficiaries. Enrollment in TRIP/TRAIL requires at least eight years of TRS service credit. TRIP premiums for non‑Medicare retirees were described (managed care example noted at $370.76 monthly for retiree coverage; PPO costs higher), and TRAIL Medicare‑secondary premiums were substantially lower (example shown $7.35 monthly for Medicare‑primary retiree coverage).

Post‑retirement work: TRS permits retirees to return to TRS‑covered work with limits: retirees may work up to 120 days per school year (TRS counts five hours as a day) with no negative impact on the pension if they received their first retirement check and observe a 30‑day separation from the last employer before returning there; prearranged employment with the last employer is prohibited. Working in non‑TRS covered jobs or outside Illinois public schools generally has no earnings limit.

Ending: TRS urged members to verify beneficiaries, confirm proof of birth date and mailing address in their online account, review annual TRS statements, and contact TRS benefits counselors or member services for personalized help.