TRS details Tier 1 retirement eligibility, benefit formula and timing options

Loading...

Summary

Teachers' Retirement System (TRS) staff reviewed Tier 1 eligibility, how service credit and final average salary determine pension amounts, early‑retirement reductions, the 75% maximum, and the Accelerated Annual Increase (AAI) option for members retiring by June 30, 2026.

Nick Stabler, a presenter for the Teachers' Retirement System (TRS), outlined Tier 1 retirement rules, how benefits are calculated and choices members can make about timing and optional purchases of service credit.

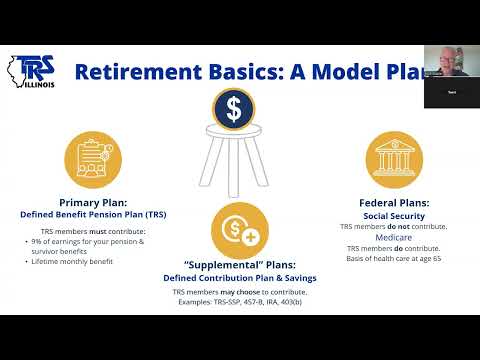

Tier 1 membership applies to educators who established public service in Illinois before Jan. 1, 2011. TRS is a state agency administered by a 15‑member board of trustees that administers benefits set in the Illinois pension code and invests member and state contributions in a trust fund, Stabler said. “We are a state agency. We are a public pension system. We are a defined benefit pension plan,” Stabler said.

The nut of the Tier 1 benefit calculation is: years of service credit × a factor (2.2% for service after July 1, 1998) × final average salary (the highest four consecutive salaries in the last 10 years). For example, a 60‑year‑old member with 30 years of service and an $85,000 final average salary would receive about 66% of that salary annually, or roughly $4,675 per month, the TRS example showed.

Service credit includes paid work (a full year equals 170 paid days), unused uncompensated sick leave conversions (maximum 340 days), optional purchased service (out‑of‑state teaching, leaves, military credit, refunded service repayment, and up to two years of recognized Illinois nonpublic service if verified by June 30, 2028) and reciprocal service from other Illinois public retirement systems when rules are met. “Every single day that you work has value,” Stabler said.

Members who retire before age 60 face a permanent reduction of 6% of the earned benefit for each year under age 60, unless they have attained 35 years of service credit. Members with 35 years of service can receive an unreduced benefit before age 60. TRS said the program’s maximum benefit is 75% of final average salary, ordinarily reached at 34 years of service (rounded up) if the member is age 60; 35 years can also satisfy the threshold for an unreduced benefit if under 60.

TRS recommended members run benefit estimates to see how choices (buying service credit, taking extra duties in a final four‑year window, or changing salary lanes) affect benefits. Stabler described an online benefit estimator available at trsil.org and said members can also request an estimate over the phone; TRS will mail an estimate and store it in the member’s account for follow‑up.

For members retiring by June 30, 2026, TRS described the Accelerated Annual Increase (AAI) option: exchange the 3% compounded annual post‑retirement increase for an upfront lump sum at retirement and a smaller non‑compounded annual increase (1.5%) beginning at age 67. Stabler advised members eligible for AAI to get an estimate that includes that option.

Ending: TRS urged members to (1) verify online statements annually, (2) consider buying optional service credit before retirement to reduce costs, (3) use the benefit estimator or speak with a counselor as retirement approaches, and (4) attend the "It's Time to Retire" webinar in the last year before retirement.