Lifetime Citizen Portal Access — AI Briefings, Alerts & Unlimited Follows

DC CFO outlines FY26 spending cuts, IT and tax initiatives as reserves are drawn down

Loading...

Summary

The Committee on Business and Economic Development heard from Lehi Lee, Chief Financial Officer for the Government of the District of Columbia, on June 11 during the committee’s FY26 budget oversight hearing. Lee said the OCFO’s proposed FY26 operating budget is about $213.7 million — a 7.8% reduction from FY25 — and said the agency is shifting final implementation costs for a major finance system from capital into the operating budget while maintaining reserves to handle cash‑flow timing.

The Committee on Business and Economic Development heard from Lehi Lee, Chief Financial Officer for the Government of the District of Columbia, on June 11 during the committee’s FY26 budget oversight hearing. Lee said the OCFO’s proposed FY26 operating budget is about $213.7 million — a 7.8% reduction from FY25 — and said the agency is shifting final implementation costs for a major finance system from capital into the operating budget while maintaining reserves to handle cash‑flow timing.

Why it matters: The OCFO manages tax administration, central collections and the District’s treasury and accounting systems. Changes it makes to staffing, IT and estimates for collections affect the District’s ability to pay bills across the fiscal year and the accuracy of revenue forecasts that underpin other agencies’ budgets.

Lee said the OCFO budget is “people and systems,” and that about two‑thirds of the office’s costs are personnel. He told the committee the proposed budget includes roughly $177.6 million in local funds and $34.4 million in special‑purpose revenue, and that the office is budgeted for 1,079 full‑time equivalents — an increase of 22 FTEs over FY25 driven largely by moving capital‑funded positions into operating status to maintain a recently stabilized main financial system (known internally as “DIFS”).

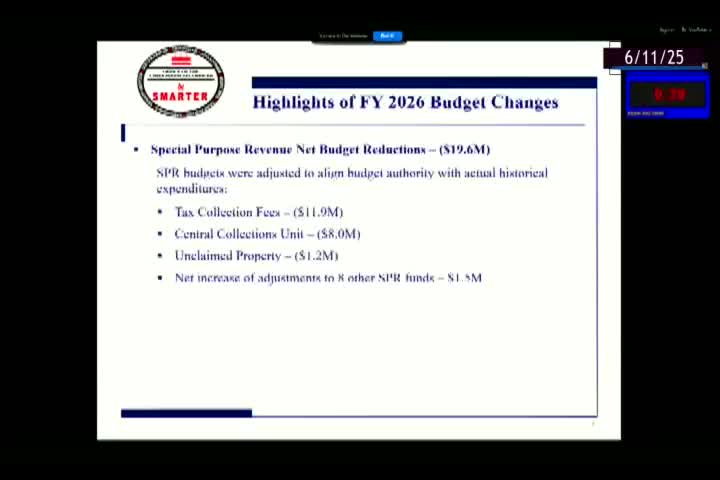

The OCFO director described several FY26 changes: a roughly $4.5 million ongoing operating cost to finish system stabilization, a one‑time $140,000 cost to program the property tax system for a new Class V tax rate, and a $19.6 million reduction in special‑purpose appropriations tied to expected lower vendor‑share payments in central collections. Lee said the latter change removes what he called “hollow budget authority” that had been included to accommodate historically high collection vendor payments but is unlikely to be needed at the same level going forward.

On tax policy issues the committee raised, Lee said the office has not yet prepared a full implementation plan for the business activity tax that some public witnesses advocated. He described the major steps needed before a new business tax could be executed — rulemaking to define taxable activity, system development, taxpayer education and audit and collection capacity — and said the OCFO would need pro forma or information returns, voluntary surveys or other outreach to collect the data necessary to design and administer a new tax. "We would need to receive that, right. Some sort of information. Lots of input," he told the committee.

Lee also addressed questions about the Qualified High Technology Company (QHTC) incentives, saying OCFO’s 2018 evaluation found $184 million in forgone franchise tax revenue and recommended tighter targeting and clawback provisions; he was not aware whether prior OCFO recommendations had been incorporated into the draft FY26 subtitle that would restore or amend the incentive and said the OCFO would follow up in writing.

The committee pressed the OCFO on reserves and cash‑flow risk. Lee explained the District has two locally mandated reserves (cash flow and fiscal stabilization) and two federally mandated reserves; the local reserves are being used intra‑year as intended and are projected to be around the same combined level at fiscal year‑end as the prior year (roughly $1.07 billion), although the office expects to draw on those reserves to meet timing shortfalls in FY26 and FY27. He said the FY26–29 financial plan relies on spending accumulated surpluses in the 2010s and early pandemic recovery (about $2.3 billion of planned use across several years) and that those surplus cushions have largely been spent, increasing reliance on reserves and tighter cash management techniques.

On debt and capital, Lee confirmed the six‑year capital plan keeps the debt‑service ratio well below the legislated 12 percent cap: about 10.4% in FY26 and roughly 11.7% in FY27–29 under current assumptions. He also told the committee events outside the District’s control — including a recent Moody’s downgrade and volatile national markets — can affect borrowing costs, though a recent bond sale was “very strong” and within budget parameters.

Committee members pushed for more follow‑up on several items Lee promised to research and return in writing: whether the combined reporting (Finnegan) corporate tax change generated additional revenue after implementation; which OCFO prior recommendations informed any proposed QHTC restoration; and more detail on the mechanics and cash‑flow implications of defeasing stadium or Wharf bonds early.

Lee closed by reiterating the office’s priorities: protect core financial operations, stabilize and maintain modern IT systems, and prepare the District to collect and account for tax changes in a way that avoids surprises. "Our budget is people and systems," Lee said during his presentation.

What happens next: The committee recorded the OCFO testimony for follow‑up. Council staff will receive requested written clarifications from OCFO on tax implementation options, prior QHTC recommendations and bond defeasance mechanics.

Ending note: The OCFO presentation framed FY26 as a year of managing system conversions, tighter operating authority and heavier reliance on financial‑plan assumptions and reserves to bridge timing gaps while the District continues to contend with constrained revenue growth.