Budget staff outline non‑tax revenue projections; sales tax timing, DMV reimbursements and airport impact fees flagged

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Staff presented a tentative approach to non‑tax general fund revenues for 2026, noting sales tax distributions were still pending, the county is revising how interest is allocated, and that potential new revenue could come from DMV service adjustments and airport hangar impact fees — both needing follow‑up and written agreements.

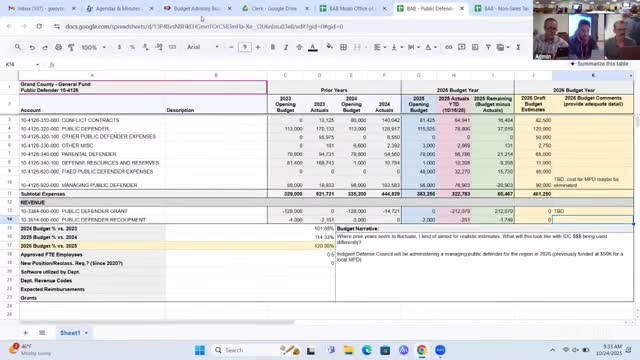

County budget staff reviewed non‑tax general fund revenue categories and described several items requiring follow up before the tentative 2026 budget is finalized.

Sales tax timing and method: Staff said they are awaiting the next sales tax distribution before finalizing sales tax projections and the tentative budget. For property tax projections, Treasurer Kaufman said he uses the tax commission’s final budgeted revenue as a base and adds new growth based on a multi‑year average. For other tax categories staff generally apply a recent multi‑year average unless there is a clear trend.

Interest and miscellaneous revenue: Budget staff said the county recently adopted an interest allocation policy; interest recorded in the general fund will reflect that policy rather than pooling interest across funds. Staff proposed a placeholder of $75,000 for miscellaneous/expense reimbursement revenue that has been irregular but historically appeared in prior years.

DMV reimbursements and intergovernmental revenue: Kaufman and others said the Utah Association of Counties is working with county staff and the assessor on a review of Department of Motor Vehicle revenues and related costs; staff noted a bill affecting out‑of‑county users could alter county DMV revenue shares and that any change would need confirmation.

Dispatch and interagency service lines: Commissioners asked about City of Moab dispatch revenue and partner agencies’ use of county dispatch. Staff said those revenue lines remain under review and that some partner arrangements (including some National Park Service dispatch decisions) have changed; staff recommended continued follow up with partner agencies to confirm 2026 contributions.

Airport hangars and impact fees: Commissioners noted the county provided an upfront contribution to airport paving/hangar work and asked whether impact fees or repayments from hangar developers or tenants should be expected as a dedicated revenue line. Staff and commissioners agreed it would be appropriate to document the expectation in writing (an MOU or loan agreement) and to create a dedicated revenue line to track any repayments or impact fees; staff will contact Airport Director Steven (Steve) and produce written documentation.

Building permits and inspections: Commissioners raised contractor complaints that building permit fees are charged but inspections and inspection capacity are limited; one commissioner suggested evaluating whether a portion of permit fees should be refunded if required inspections are not provided or to otherwise address inspection capacity. Staff noted planning and inspection staffing shortages have affected permit volumes and will include updated permit revenue projections based on recent four‑year averages.

TRT mitigations and museum payments: Commissioners discussed whether restricted transient room tax (TRT) funds should be used as grants to outside nonprofits (for example museum funding) or whether such ongoing expenditures should come from the general fund so the county retains audit and oversight; staff said they had not included a museum allocation in the tentative budget and would leave such discretionary distributions for commission decision.

Next steps: Budget staff said they will update the tentative budget after the pending sales tax distribution arrives, confirm DMV and IDC/grant timing, request written agreements for airport repayment expectations, and provide a working tentative budget to the budget advisory board early next week for review.

Ending: Staff emphasized the tentative budget will be a working document and that some lines (sales tax, intergovernmental revenue, airport impact receipts and grant timing) will be updated as additional data arrive.