Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Tennessee Department of Revenue details allowable business-tax deductions, recordkeeping rules in webinar

Summary

The Tennessee Department of Revenue hosted a webinar March 25, 2025, explaining which deductions are allowed on the state business tax return, documentation requirements, and examples for contractors, repossessions, interstate sales and bad debts.

The Tennessee Department of Revenue hosted an online webinar March 25, 2025, to explain which deductions businesses may claim on the state business tax return, how they must be reported on Schedule B (and Schedule C for certain contractors), and what records taxpayers must keep to substantiate those claims.

The webinar, presented by a taxpayer-education team and featuring audit-division subject-matter expert Katina Sykes, emphasized the distinction between Tennessee business tax rules and federal income-tax rules, the department’s $100,000 gross-receipts filing threshold, and several commonly claimed deductions — cash discounts, returned items, trade-in allowances, repossessed goods, subcontractor payments for class-4 contractors, sales shipped out of state, bad debts and certain excise taxes.

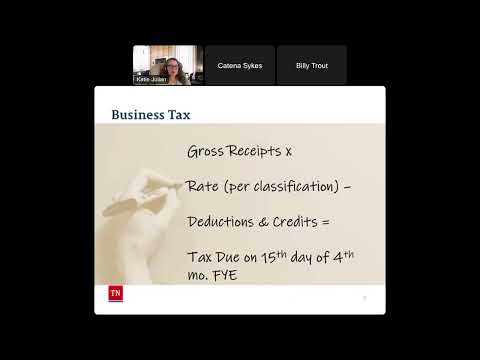

Why it matters: Because Tennessee business tax is assessed on gross receipts, deductions are limited and must be taken on the return in a specific order and on specific lines. Presenters cautioned that many federal business deductions do not apply to Tennessee business tax, and that unsupported claims will be disallowed in audit.

Key takeaways

- Filing threshold and basics: Katie, a presenter with the department’s taxpayer education team, said business tax is a state tax based on gross receipts and that businesses generally must file only if gross receipts exceed $100,000 for the tax year. The department is advising businesses that did not meet the threshold in prior years to contact Revenue so their accounts can be converted to “filing not required” or minimal-activity status.

- Gross receipts definition: Presenters defined gross receipts as the business’s taxable sales without deductions for overhead, wages or other operating costs. Exempt sales and certain excluded entities (for example, certain manufacturers) are not included in gross receipts.

- Where deductions are reported: All business-tax deductions are taken on Schedule B of the business tax return; subcontractor payments for class-4 contractors use a separate…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat