Tennessee Department of Revenue details allowable business-tax deductions, recordkeeping rules in webinar

Loading...

Summary

The Tennessee Department of Revenue hosted a webinar March 25, 2025, explaining which deductions are allowed on the state business tax return, documentation requirements, and examples for contractors, repossessions, interstate sales and bad debts.

The Tennessee Department of Revenue hosted an online webinar March 25, 2025, to explain which deductions businesses may claim on the state business tax return, how they must be reported on Schedule B (and Schedule C for certain contractors), and what records taxpayers must keep to substantiate those claims.

The webinar, presented by a taxpayer-education team and featuring audit-division subject-matter expert Katina Sykes, emphasized the distinction between Tennessee business tax rules and federal income-tax rules, the department’s $100,000 gross-receipts filing threshold, and several commonly claimed deductions — cash discounts, returned items, trade-in allowances, repossessed goods, subcontractor payments for class-4 contractors, sales shipped out of state, bad debts and certain excise taxes.

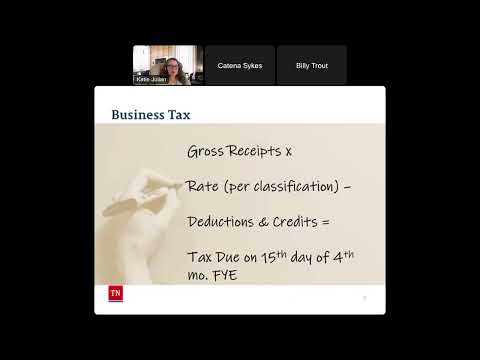

Why it matters: Because Tennessee business tax is assessed on gross receipts, deductions are limited and must be taken on the return in a specific order and on specific lines. Presenters cautioned that many federal business deductions do not apply to Tennessee business tax, and that unsupported claims will be disallowed in audit.

Key takeaways

- Filing threshold and basics: Katie, a presenter with the department’s taxpayer education team, said business tax is a state tax based on gross receipts and that businesses generally must file only if gross receipts exceed $100,000 for the tax year. The department is advising businesses that did not meet the threshold in prior years to contact Revenue so their accounts can be converted to “filing not required” or minimal-activity status.

- Gross receipts definition: Presenters defined gross receipts as the business’s taxable sales without deductions for overhead, wages or other operating costs. Exempt sales and certain excluded entities (for example, certain manufacturers) are not included in gross receipts.

- Where deductions are reported: All business-tax deductions are taken on Schedule B of the business tax return; subcontractor payments for class-4 contractors use a separate Schedule C (payment-to-subcontractor worksheet). Online filers answer whether they have deductions; an affirmative response expands Schedule B in the e-file system.

- Common allowable deductions and examples explained by the presenters: - Cash discounts: Deductions for cash discounts taken by customers are entered on Schedule B (cash-discounts line). Example used: a $5,000 credit sale with a 2% cash discount results in a $100 cash-discount deduction and a $4,900 net taxable amount. - Returned items: Refunds for returned goods can be deducted on Schedule B; the amount should match sales-tax reporting for returned items. - Trade-in allowances: If a trade-in is of “like kind and character,” the trade-in allowance is reported on Schedule B (trade-in line). Example used: a $30,000 vehicle sale with a $9,000 trade-in—$30,000 is included in gross receipts and $9,000 is reported as the trade-in deduction. Presenters said trades should be documented (model/serial number) on invoices. - Repossessed goods: Dealers that repossess property can deduct principal unpaid in excess of $500 on Schedule B (repo line); presenters noted the calculation can be complex and directed dealers to related sales-tax worksheets used to compute the amount. - Subcontractor payments (class 4 contractors only): Class 4 contractors (those who construct or improve real property) may deduct amounts paid to subcontractors who hold the required business or contractor license. The Schedule C must be completed fully with subcontractor name, address, business-license or contractor-license number, county/city of license, description of activity, amount paid and date paid. Presenters emphasized that materials or supplier deliveries are not eligible as subcontractor payments. - Sales of services and of tangible personal property in interstate commerce: Sales of services delivered to locations outside Tennessee and sales of tangible personal property where the purchaser takes possession outside the state can be deducted on Schedule B. Presenters used examples: a Tennessee computer repair shop that ships the repaired computer to an out-of-state customer is deductible; a Tennessee mechanic repairing an out-of-state truck where the customer took possession in Tennessee is not deductible. The presenters noted a statutory change tied to a recent Revenue Modernization Act affecting deductions for sales of services delivered outside Tennessee for periods after Jan. 1, 2026. - Bad debts: Taxpayers may deduct bad debts that were previously included in gross receipts and for which business tax was paid; the debt must be written off as uncollectible and taken as a deduction in the period it is written off. Audit guidance: Katina Sykes said, “It has to be written off on the federal tax return, so I would I would start there.” If a previously written-off debt is later collected, that recovery is subject to business tax when received. - Miscellaneous excise taxes: Certain federal and state excise taxes paid directly by the taxpayer (for example, federal excise on fuels or state motor-fuel taxes) may be deductible if claimed by the taxpayer who paid them. Sales taxes and liquor-by-the-drink taxes collected from customers should generally not be included in gross receipts; if they are included, they should be deducted on Schedule B.

- Documentation and audit risk: Presenters repeatedly stressed the requirement to retain invoices, ledgers and other supporting documentation for any deduction; the audit-division representative warned that unsupported deductions will be disallowed. Billy Trout, a department host, noted the department sees many returns with zero deductions and explained that in many cases a business’s activities simply do not qualify for the limited list of state deductions.

- Contractor and license issues: Presenters said that to claim the subcontractor payment deduction, the subcontractor must have either a business license or contractor license number; if the subcontractor’s work is not class-4 contracting activity (for example, pure materials delivery or non-contracting landscaping), the payment will not qualify. Presenters suggested taxpayers who want to claim the deduction ask subcontractors to obtain a minimal local license (the presenters said a minimal activity license is typically available for a small fee, often cited as $15 by the panel).

- Credits: The panel clarified that personal tangible-property tax paid by a business (the local tax on business equipment/inventory) is a credit on the business tax return, not a deduction, and is limited to amounts actually paid and to statutory caps (presenters noted the credit may offset up to half of the tax liability but is limited by the amount paid).

Q&A highlights

The presenters answered numerous audience questions, including whether discounted sales lower gross receipts (yes—the taxable amount is the actual transacted price), how interstate sales are sourced and when a sale is treated as interstate commerce, whether a concrete-pumping company’s fee can qualify as a subcontractor payment (the panel agreed pumping into foundations or repairing/improving real property would typically be contracting activity), and how bad-debt documentation is evaluated by auditors.

Next steps and resources

Presenters directed listeners to the department’s business-tax manual (chapter 9 covers deductions), the business-tax help articles on the department website, the webinar-video library where the recording and PDF slides will be posted, and the department’s general tax email and phone line for account-specific questions. The panel urged taxpayers to contact Revenue if they believe their account should be converted to minimal-activity licensing because their gross receipts are below the $100,000 threshold.

Ending

The webinar closed with the department encouraging attendees to complete the exit survey (needed to request continuing professional education credit), announcing upcoming webinars and reminding taxpayers that claims for deductions must be supported by documentation and reported on the correct schedule on the business tax return.