Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

LSA outlines Iowa property tax system and recent legislative changes

Summary

Michael Peters of the Legislative Services Agency summarized how Iowa determines assessed and taxable values, the rollback (assessment-limitation) system, exemptions and credits, tax increment financing, school funding links, and the effects of recent laws including House File 718 and Senate File 2442.

Michael Peters of the Legislative Services Agency summarized Iowa’s property tax system and recent legislative changes in an LSA presentation that reviewed how properties are assessed, how taxable values are calculated, and how recent laws alter levy limits and exemptions.

Peters said the presentation was intended as a high-level educational overview and walked through the full property-tax process from local assessment through bill issuance, with examples focused on residential property. “These are meant for educational purposes only and are not meant as LSA recommendations,” he told attendees.

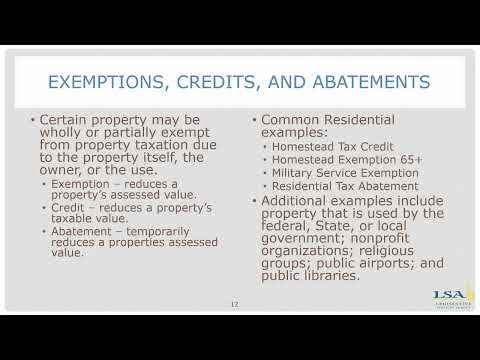

The presentation explained three core concepts: property classes, the difference between assessed value and taxable value, and the two-year lag between assessment year and the fiscal year when taxes are due. Peters noted Iowa groups properties into nine classes, including residential, agricultural land, commercial, industrial and utilities, and said assessed value reflects market value while taxable value is the result after rollbacks and exemptions.

Peters outlined the typical property tax timeline: local and county assessors set assessed values; taxpayers may protest to local boards of review; the Iowa Department of Revenue performs equalization to ensure statewide consistency; assessment limitation (commonly called the rollback) adjusts taxable values; local governments set levy rates; and tax bills are issued. He emphasized assessors typically set values every two years (annually for utilities) and identified three valuing authorities depending on…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat