Equalization director details $983,000 annual tax revenue loss from development capture districts

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The county's equalization director presented a downtown development authority (DDA) and local development financing authority (LDFA) capture report showing roughly $983,000 in annual lost tax revenue countywide from incremental capture, with specific figures by municipality.

Equalization staff presented the county's DDA/LDFA capture (tax-increment financing) report and quantified revenue the county no longer receives because incremental growth is captured by local development authorities.

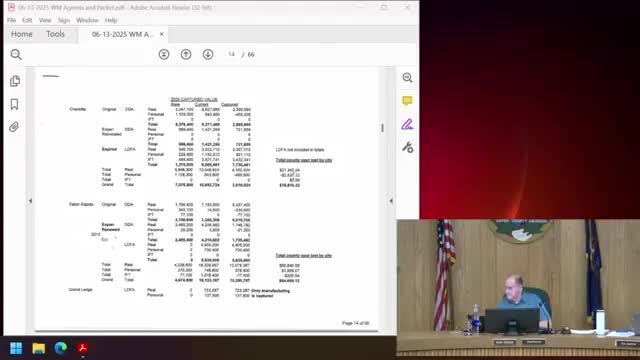

Equalization director Tim (first name only in the transcript) described how tax-increment financing districts establish a base year tax value and then capture increases attributable to new construction or inflation for local development projects. Tim reported current annual capture figures by municipality: Charlotte ($18,816); Eaton Rapids ($64,609 for DDA and LDFA); Grand Ledge ($277,009); Potterville ($56,688); Bellevue Village ($9,504); and Delta Township ($95,749). He said the total countywide captured amount is $516,008 in real (tax) revenue and $523,003 in total revenue; when additional voted millages are included the county's annual loss is about $983,000.

Tim and commissioners discussed the origin and permanence of many districts, noting most were created in the mid-1990s and that the county often cannot alter those captures because they are governed by state rules and the original agreements. He said some agreements are contract-limited and are monitored by the equalization department.

Commissioners asked about high-profile local development (battery plant and General Motors) and why the county receives little or no property-tax revenue from certain projects: Tim explained the battery plant is inside a state Renaissance Zone (a state-level incentive) and that some manufacturing projects use industrial facilities tax exemptions (IFTs) that reduce taxes for a set period (commonly 12 years), while certain intergovernmental (425) agreements route some tax and income-tax benefits to Lansing or other jurisdictions.

The presentation closed with staff offering to continue monitoring and reporting capture figures each year.