Oxnard staff recommend 2025–26 public-safety pension property tax rate of 5.0615 cents per $100

Loading...

Summary

City of Oxnard finance staff recommended the Oxnard City Council adopt a resolution setting the fiscal year 2025–26 property tax rate to pay voter-approved public safety pension obligations, proposing 5.0615 cents per $100 of assessed value (about $50.62 per $100,000).

Jim Costello, an administrative services analyst with the City of Oxnard finance department, recommended that the Oxnard City Council adopt a resolution establishing the fiscal year 2025–26 property tax rate to pay voter‑approved obligations for public‑safety pension expenses. "The recommendation is that the city council adopt a resolution establishing the fiscal year 2025–26 tax rates on property in the City of Oxnard for the payment of voter approved obligations related to eligible public safety personnel pension expenses," Costello said during a presentation to the council.

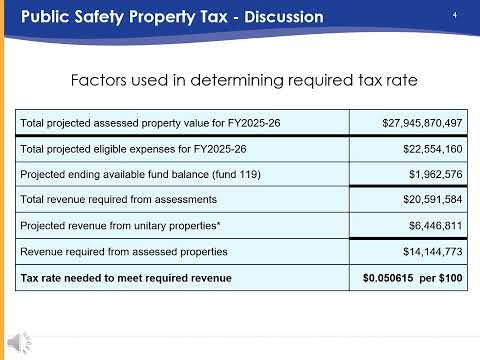

Costello said the proposed tax rate to raise the needed revenue is 5.0615 cents per $100 of assessed property value — about $50.62 for each $100,000 of assessed value. The proposed rate, he said, is a 7% increase over the current year’s rate but remains below Oxnard’s maximum allowable override rate of 7.6637 cents per $100 and about 7.6% lower than the city’s 10‑year average for this levy.

City staff described the history and legal limits for the levy. Costello said Oxnard voters in 1951 authorized enrolling the city’s fire and police public‑safety employees in the California Public Employees' Retirement System (CalPERS) and obligated the city to pay the annual cost of participation via a property tax levy. The presentation cited Proposition 13 (1978) and a California Supreme Court case identified in the transcript as "Carmen v. Alverd" as grounds for treating that levy as voter‑approved indebtedness and exempting it from Proposition 13’s 1% general rate cap. The presentation also cited Assembly Bill 13 (1985) as setting maximum override rates based on rates in effect in fiscal year 1983–84 and referenced a 2002 court ruling that limits the levy to paying benefits that were in effect on July 1, 1978.

For 2025–26, Costello said the city’s actuarial work (contracted to Foster and Foster, per the presentation) identified eligible pension costs and that the proposed budget assumes approximately 137 public‑safety fire positions and 242 public‑safety police positions. Total estimated public‑safety retirement costs for those positions were presented as $31,283,920, with $22,554,160 identified as eligible for funding from this voter‑approved levy.

Costello and staff described offsets used to reduce the levy. The presentation said the city projects an available fund balance of $1,962,576 at the end of the current fiscal year that would be applied to eligible expenses, and that the city’s property‑tax consultant (named in the transcript as HDL Corin and Cone) projected unitary property tax revenue of $6,446,811 to be allocated to the Public Safety Retirement Fund. After applying those offsets, staff said $14,144,773 would need to be raised from assessed parcels, based on a projected assessed value for the city of about $27.9 billion.

Staff explained unitary property tax revenue to the council: such revenue comes from statewide taxation of large properties owned by railroads and utilities, then allocated back to cities and counties. The presentation said Oxnard began receiving unitary property revenue into the Public Safety Retirement Fund in fiscal years 2020 and 2021 after an audit initiated by the city’s property tax consultants.

The presentation concluded with the recommendation that the council adopt the resolution setting the FY 2025–26 rate; the transcript records the presentation and says staff will be available at the meeting to answer questions but does not record a council vote or formal action on the recommendation.

Staff will be available at the council meeting to address questions about the actuarial analysis, the calculation of eligible expenses, and the use of unitary property revenue.