Get Full Government Meeting Transcripts, Videos, & Alerts Forever!

Collin County budget workshop lays out revenue scenarios and tax-rate choices

Summary

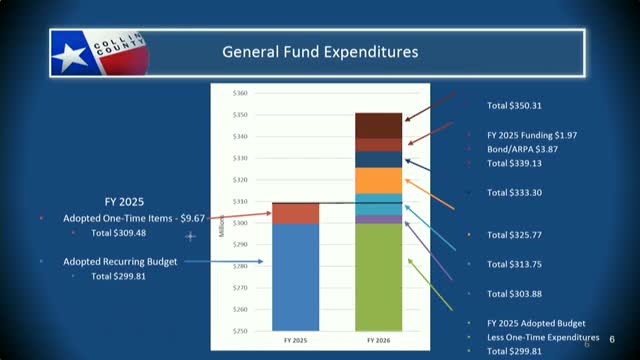

County budget director presented base-budget figures showing general-fund starting point near $299.8 million, insurance pressures needing roughly $4 million, and tax-rate options that would produce combined funds of roughly $575.8M–$595.9M depending on choices and legal caps.

Collin County’s budget team told the Commissioners Court during its annual workshop that a steady set of cost pressures — rising medical insurance bills, contractual obligations and public-safety needs — will shape the county’s tax-rate decision for 2026.

Monica Harris, the county’s budget finance director, said the county began the process from an adopted recurring general fund of $299.81 million and that medical insurance increases alone required about $4 million in additional funding. “Our base budget is the continuation of those existing programs,” Harris said, describing the base as covering ongoing programs, contractual obligations and…

Already have an account? Log in

Subscribe to keep reading

Unlock the rest of this article — and every article on Citizen Portal.

- Unlimited articles

- AI-powered breakdowns of topics, speakers, decisions, and budgets

- Instant alerts when your location has a new meeting

- Follow topics and more locations

- 1,000 AI Insights / month, plus AI Chat