New broker warns July 2026 renewal could raise Southborough’s health premium; GLP‑1 drug costs identified as a material driver

Summary

Bauerslaw Insurance presented a July 2026 renewal forecast for the town's Harvard Pilgrim plan, projecting a released renewal near 16% and an optimistic negotiation target of about 12%; the firm highlighted approximately $1.3 million in GLP‑1 weight‑loss drug spend (Jan–Oct 2025) and said removing GLP‑1 coverage could cut 2–4% off renewal, while adding a rider to keep coverage would add about 8–10% to premiums.

The Select Board heard a budget‑relevant briefing from new broker Bauerslaw Insurance about the town’s health‑insurance renewal outlook for July 2026.

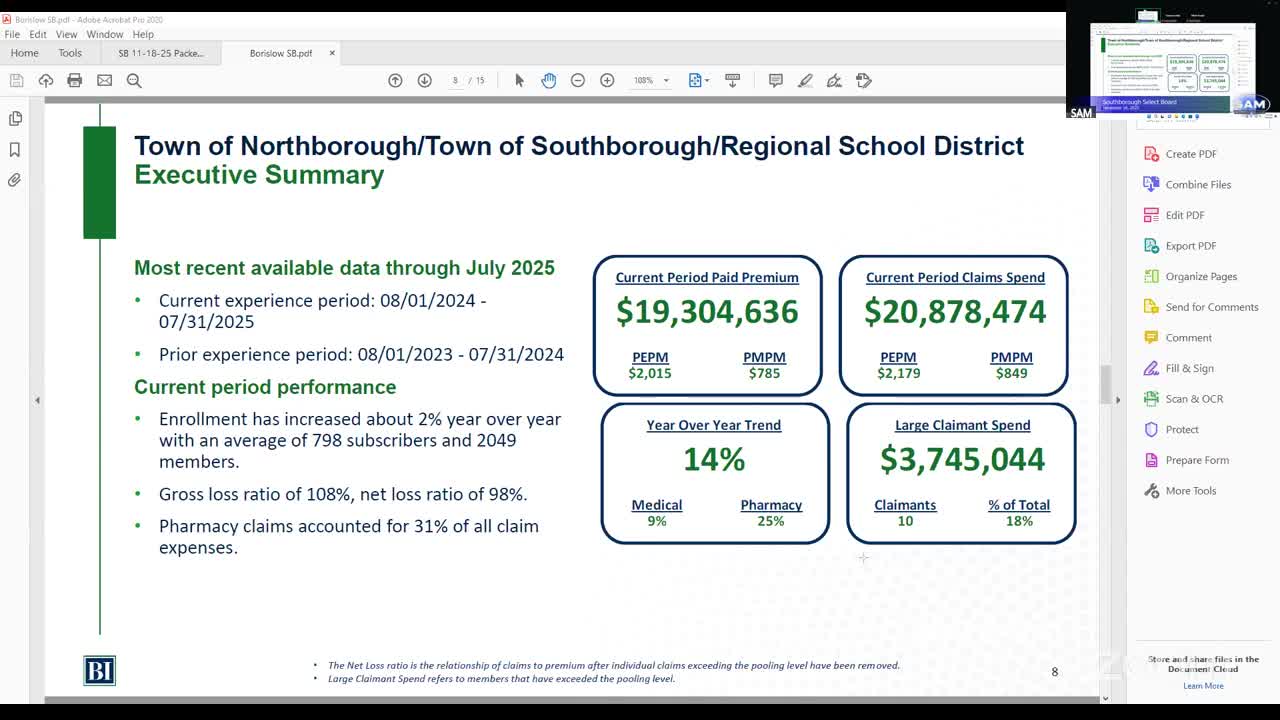

Susan Bauver and Deb Young of Bauerslaw described enrollment by plan tier, stop‑loss pooling ($170,000), and historic claims trends (a 24‑month rolling window through July 2025). They reported current premiums at about $19 million and claims at about $20 million, indicating a gross loss ratio above 1.0. Bauver said the July 2026 renewal was released at roughly a 16% increase but the broker hopes negotiation will bring that closer to 12%.

A key cost driver is GLP‑1 drugs used for weight loss: Bauver said the town’s spend for GLP‑1s from Jan. 1 through Oct. 31, 2025, was about $1.3 million. Bauver said Harvard Pilgrim will no longer cover GLP‑1 weight‑loss drugs effective with the plan renewal (they will continue to cover GLP‑1s for diabetes), and that the net impact of the carrier’s change is an estimated 2–4% reduction in the released renewal. Conversely, continuing GLP‑1 coverage via a town‑paid rider would be large — she estimated an additional 8–10% on top of a released renewal.

Board members discussed whether other carriers could produce better pricing and whether the school district’s contract differences alter premium splits. Bauerslaw advised that carriers are experience‑rated, so changing vendors is not a guaranteed long‑term shield from a town’s own claims experience. The broker also noted large claimants and the role of six additional months of claims data in finalizing renewal numbers.

Next steps: Town staff and the broker will continue negotiations with the carrier, review the claims cutoff date for renewals and bring more detailed premium‑share and budget impact figures back for the Select Board and budget planning.