OEA says Oregon avoiding recession for now; recent one‑time corporate payments lift near‑term revenue outlook

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

Office of Economic Analysis told the joint revenue committees that the Oregon and national economies are decelerating but not in recession, that a 2026 reacceleration is projected, and that a recent influx of corporate tax payments — largely settling prior years — accounts for most of a near‑term improvement in the revenue forecast.

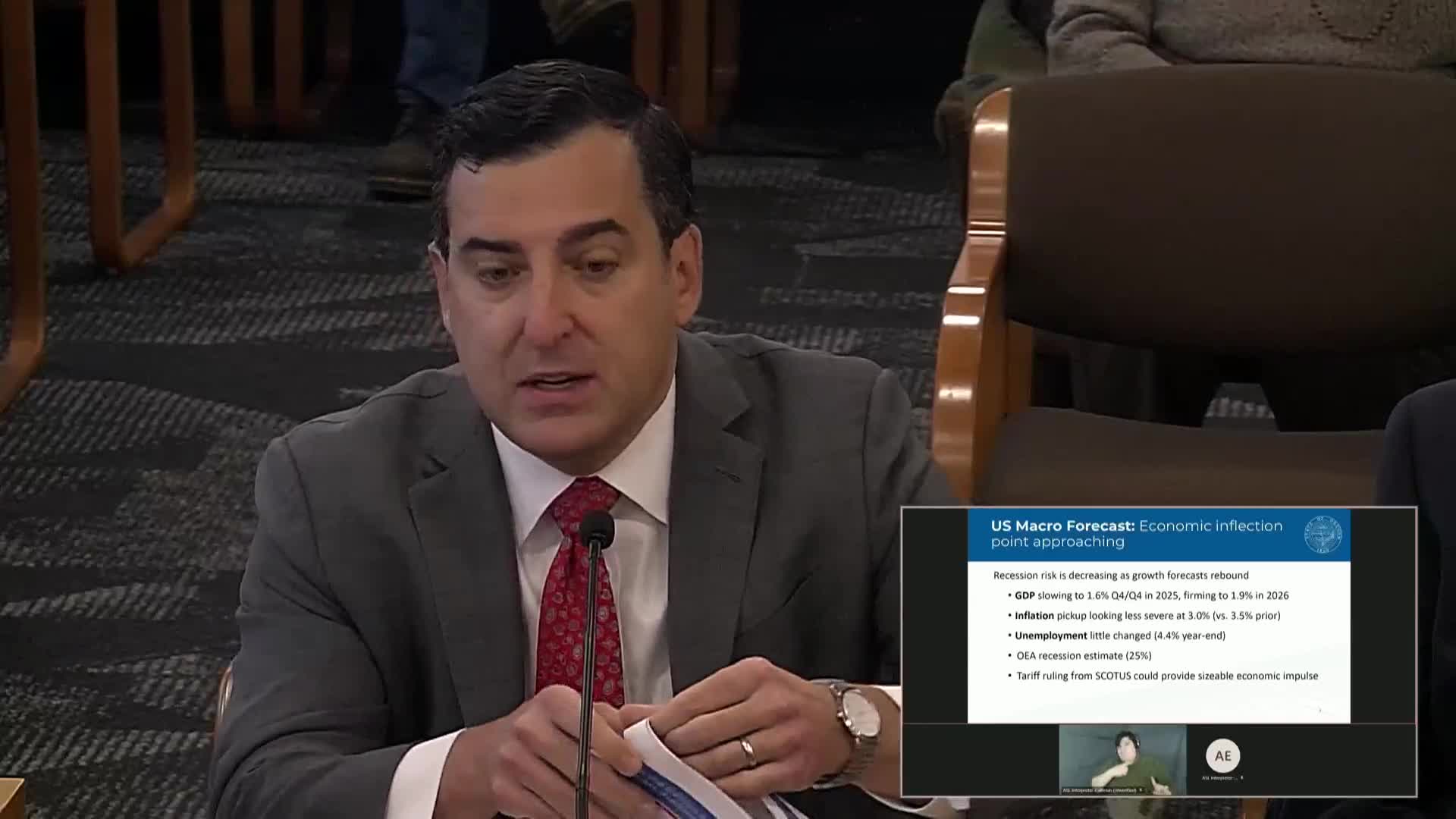

The Office of Economic Analysis told the House Interim Committee on Revenue and the Senate interim committee on finance and revenue that Oregon has continued to “steer clear of recession” even as economic growth slows, and that a modest reacceleration is expected in 2026 if current forecasts hold. Carl Riccadonna, Oregon’s chief economist, said the state’s outlook reflects a range of private and federal forecasts but remains exposed to several major risks, including a pending Supreme Court ruling on tariffs and missing federal data from a recent government shutdown.

The revenue outlook, Michael Kennedy of OEA said, improved largely because of a recent influx of corporate income tax payments. Kennedy described those corporate receipts as a settlement of prior tax years rather than a durable increase in current activity, calling the windfall “really like finding money out on the sidewalk” and saying OEA and the Department of Revenue had verified the payments are related to prior‑year accounts and therefore can be counted in the near‑term ending balance.

OEA emphasized three forces shaping the economic outlook: lower effective tariff pressure than early projections, expected Federal Reserve interest‑rate cuts that will work with a lag, and the effects of federal tax changes (HR 1) that include retroactive elements. Riccadonna also flagged distributional differences: a K‑shaped profile of wage and job outcomes that leaves lower‑income households and interest‑sensitive industries (housing, manufacturing) weaker than higher‑income households and technology sectors.

Committee members pressed OEA on confidence and timing. With many federal series delayed, Riccadonna said OEA has substituted private‑sector indicators (ADP employment, credit‑card spending, Indeed postings) and expects the missing federal releases to trickle in within weeks; OEA plans to incorporate those data into the February forecast if they materially change the outlook. Kennedy cautioned that some items in the current revenue estimate are timing effects: while the one‑time corporate receipts improve the near‑term ending balance, they are not a signal that recurring revenue measures have permanently strengthened.

OEA also reviewed downside scenarios and historical biennium patterns to illustrate uncertainty around the baseline. The agency noted it will continue to watch unemployment filings, WARN notices and upcoming tax‑season data, and that the larger reserve posture remains an important budgetary buffer as the biennium proceeds.

The committee did not vote on any measures during the meeting; OEA and LRO will return with updated forecasts after additional federal data and fourth‑quarter estimated payments are released.