Finance committee hears tax-collection update and reviews bank agreement that limits interest on first $5 million

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

The finance committee reviewed current tax‑collection metrics and discussed the town's bank arrangement that does not pay interest on the first $5,000,000 in deposits; members requested a copy of the signed bank agreement and clarifications about interest and fees.

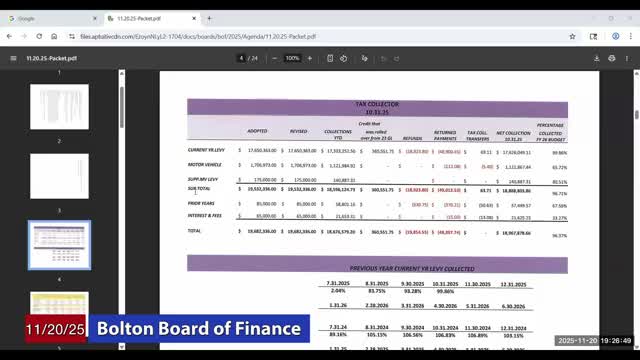

At the Nov. 20 finance committee meeting, Jill presented the town’s tax‑collection summary and explained changes in the motor‑vehicle supplemental levy and how collection timing affects interest revenue.

Jill reported the collection rates as recorded in the meeting packet: 99.86% for current property tax, about 65.72% for motor‑vehicle collections and 80.51% for the supplemental category, which the committee discussed is now being collected twice per year rather than once in January. Committee members noted that timing differences make direct year‑to‑year comparisons difficult.

Members questioned how the town’s banking arrangement affects interest income. Jill and others said the town’s bank does not pay interest on the first $5,000,000 of deposits but provides account services; interest is paid only on balances above that threshold. Chair Ross Lally noted the town earned substantial interest in the prior fiscal year and stressed the importance of understanding how collection timing and bank terms affect revenue.

Several members asked Jill to obtain and circulate the executed bank agreement so the committee can review exact terms, margins and fee exposures. The meeting record also highlighted that, because of combined federal grant spending for the town and school, the town must prepare for a single federal audit (see separate item) when federal expenditures exceed $750,000.

No formal vote was taken on the bank agreement; members directed staff to provide documentation and additional detail at a future meeting.