Lexington 01 receives clean audit; fund balance ~30% of annual expenditures

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

External auditors issued an unmodified opinion on Lexington 01—s 6/30/2025 financial statements and reported no material weaknesses; the district reported a June 30 fund balance of approximately $114.64 million (about 30% of annual expenditures) and unassigned balance roughly 25%.

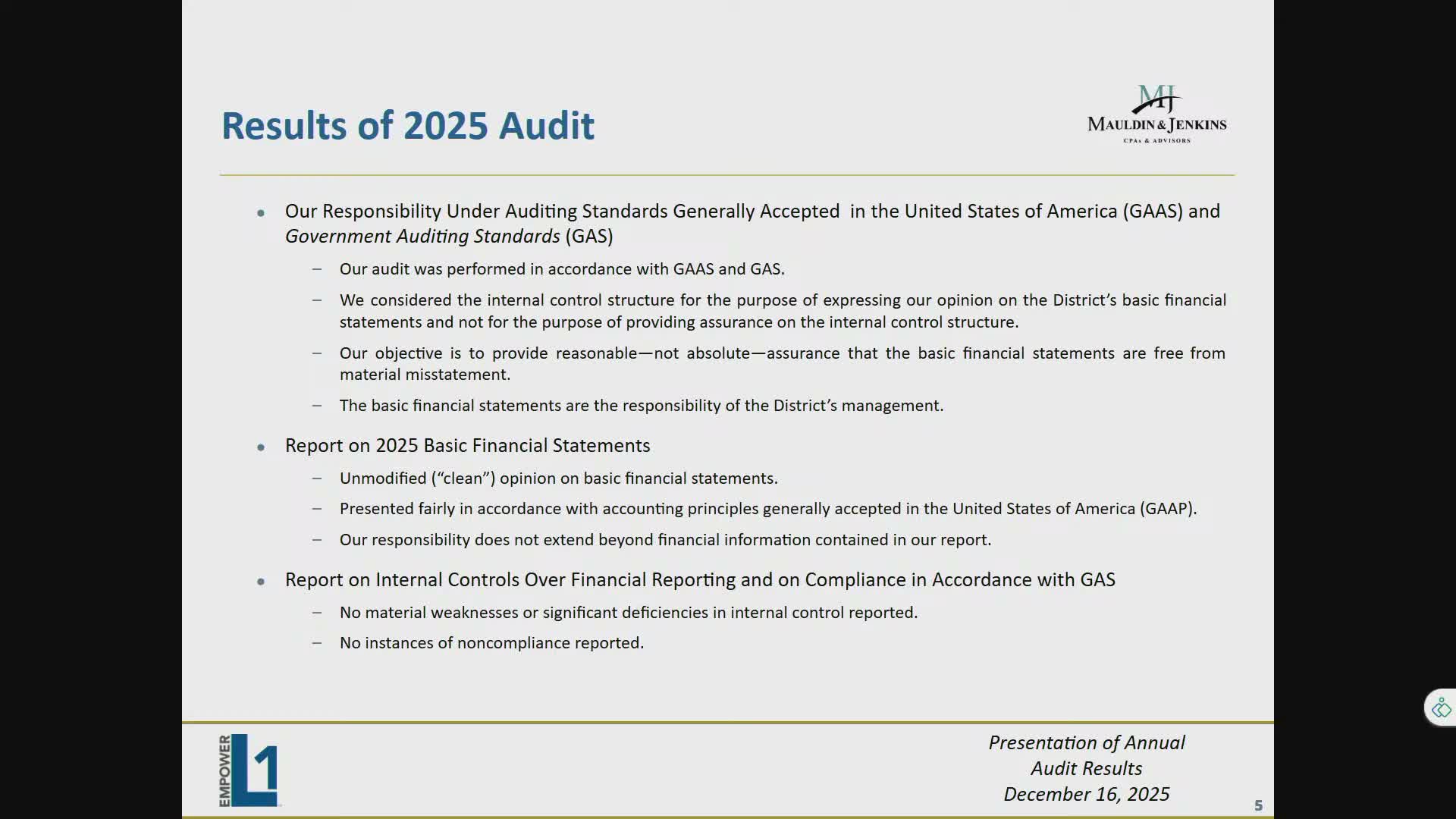

The Lexington County School District One board was presented with the district—s annual comprehensive financial report for the year ended June 30, 2025, and the audit team issued an unmodified (clean) opinion with no material weaknesses or significant deficiencies.

Brian Nevison of Malden Jenkins, the lead audit director, told trustees the audit was performed in accordance with generally accepted auditing standards and government auditing standards. He said the district received a "clean" opinion on the financial statements and a clean single-audit opinion for federal programs (required because federal expenditures exceeded $750,000). "We did issue an unmodified or cleaned opinion on the financial statements," Nevison said.

Key financial highlights presented by the audit and finance staff:

- The district—s total fund balance as of June 30, 2025, was reported at $114,636,000, which Nevison said is about 30% of annual expenditures and transfers. - Unassigned fund balance was reported at roughly 25% of annual expenditures, above the South Carolina statutory one-month minimum (8.3%) and near/exceeding GFOA recommendations (around 16.7%). - The audit required the implementation of GASB guidance related to compensated absences, which materially affected the statements and is described in footnote disclosures.

During board Q&A, trustees asked for a breakout of one-time versus recurring expenditures (one trustee referenced about $2.2 million in one-time items for a facility study, demographics study and IT warranties). Administration agreed to provide a more detailed breakout in follow-up materials.

What happens next: the district will incorporate audit findings into its financial reporting, provide the requested breakout of onetime vs. recurring items, and proceed with budget development for 2026–27 informed by priorities the board identified during a recent budget workshop.