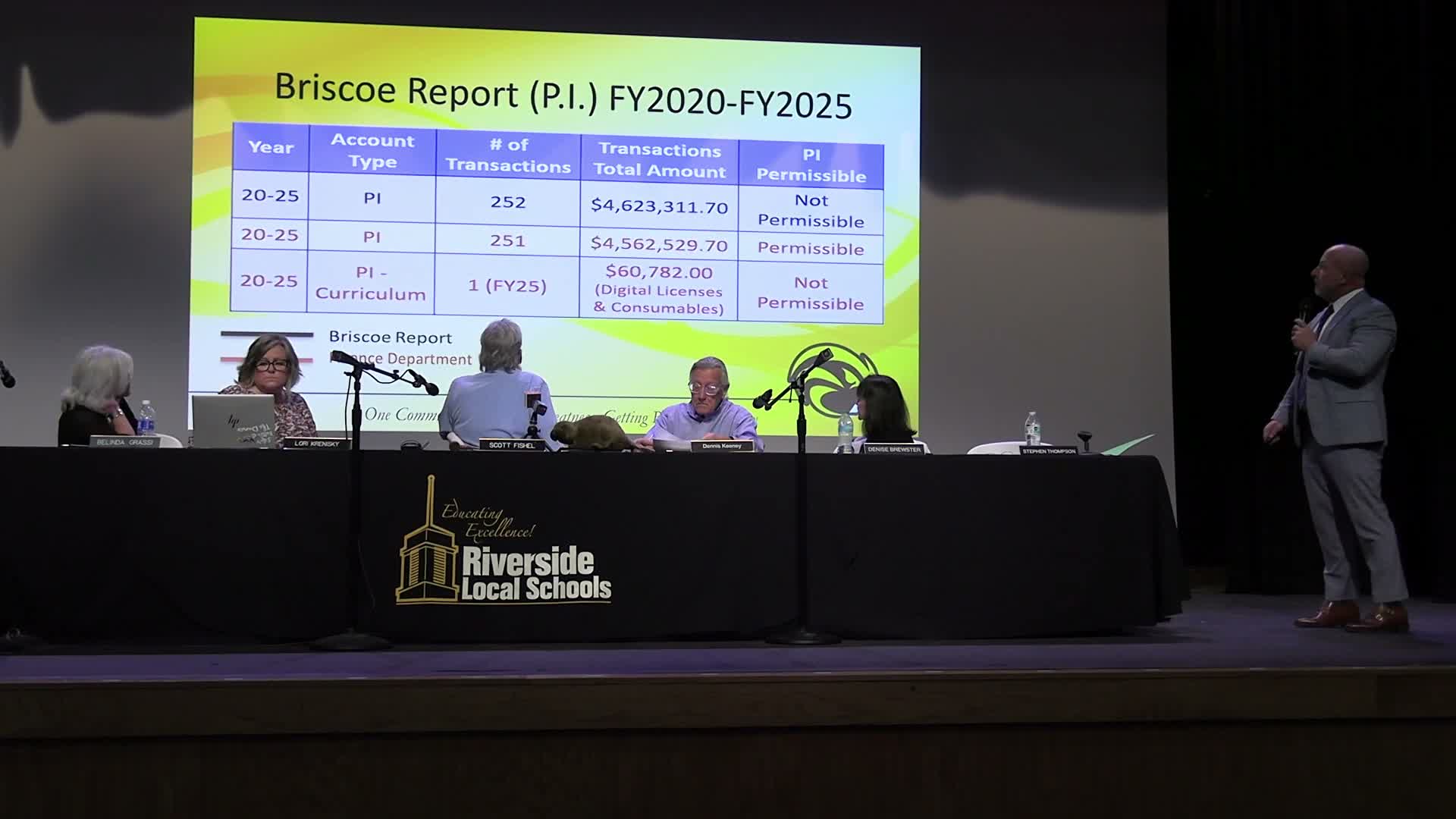

District audit contrasts with outside consultant; $60,782 in PI spending flagged and one-time transfer recommended

Get AI-powered insights, summaries, and transcripts

Sign Up Free

Summary

The board reviewed conflicting audit findings: Briscoe Consulting reported $4.6 million in potentially impermissible PI transactions while the district audit found $4.5 million permissible; the treasurer recommended a one-time $60,782 transfer to correct digital-license charges and informed the board of a pending legal notice.

The Riverside Local School District Board of Education heard competing audit findings and a recommendation for a corrective fund transfer during its special meeting. The district’s finance representative said the outside Briscoe Consulting Group identified 252 transactions totaling $4,600,000 it characterized as not permissible, while the district audit found 251 transactions equaling $4,500,000 that it considered permissible. The treasurer recommended a one-time transfer of $60,782 from the general fund back into the Permanent Improvement (PI) account to cover digital licenses and consumables the audit deemed impermissible.

Why it matters: The PI account is restricted to capital and certain improvement expenditures; using it for operating items can trigger remedial transfers and, in some circumstances, legal action. Board members were told the Briscoe invoice for the review is $20,482 and the district had received notice of pending legal action by FedEx on the same day as the meeting.

Details: The finance report—presented by the district treasurer—said the disputed items date from fiscal year 2020 through 2025 and included several large purchases (for example, bus leases, laptops and facility work). The treasurer credited assistant treasurer Patrese for pulling every purchase order during the review and said the PI findings included more than $100,000 line items such as generator work and materials testing. The treasurer characterized the district’s reconciled audit numbers as lower than Briscoe’s total and proposed the $60,782 corrective transfer to make the PI account whole.

Board reaction and next steps: Board counsel was copied in the reading of the executive-session resolution earlier in the meeting, and the treasurer told the board it had received notice of pending legal action. No formal vote on the transfer was recorded during the open session; the treasurer said they would provide follow-up documentation. The board did not adopt a policy change at this meeting; members asked for clarification on vetting of Briscoe Consulting and on specific questioned transactions.