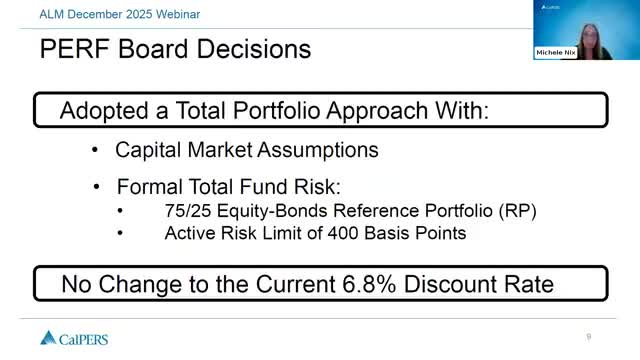

CalPERS board adopts total-portfolio approach, sets 75/25 reference portfolio and 400-basis-point active-risk limit

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

CalPERS staff told stakeholders the board in November adopted a total-portfolio approach (TPA) that uses a single 75% equity / 25% bond reference portfolio and an initial 400-basis-point active-risk limit; staff expect to operate nearer 250–350 bps and project roughly 60 bps of extra return from active risk.

The California Public Employees Retirement System said its board in November adopted a new asset-liability management framework that moves governance from multiple asset-class benchmarks to a single total-portfolio approach, staff told stakeholders in a webinar.

"The board adopted our ALM recommendations," Simone Parker, stakeholder-relations lead, said during the webinar announcing the change. Chief Investment Officer Steven Gilmore described the new reference portfolio as a simple, transparent benchmark: "that reference portfolio . . . was 75% equities and 25% bonds." The board also approved an initial active-risk limit of 400 basis points to give management flexibility to pursue active strategies beyond the reference mix.

Steven said the reference portfolio lets observers judge whole-fund performance against a clear standard rather than many separate benchmarks. "Rather than having lots and lots of benchmarks, we have people focusing on, okay, what's the overall portfolio? Is it achieving the objectives that we set?" he said. Staff said the fund currently operates at roughly 230 basis points of active risk and expects to move toward an operating range of 250–350 bps (a working assumption of about 300 bps), with staff projecting roughly 60 basis points of incremental return from that active risk.

Supporters of the change said TPA can increase transparency and accountability by making deviations from the reference portfolio clear. Steven said the shift is more evolutionary than revolutionary and will not change the board's authority over investment risk and governance.

Implementation steps described during the webinar include revised dashboards and risk metrics for quarterly reporting, annual projected portfolios shared with the board, and a redraft of investment policies to be presented to the board in March as a first reading and voted in June.

CalPERS said the change aims to align portfolio construction more directly with the system’s long-term objective of sustaining benefit payments, while keeping existing ALM cadence (four‑year cycle with a two‑year midpoint review).