Mineola board adopts expanded senior property-tax exemption, citing modest shift for other homeowners

Get AI-powered insights, summaries, and transcripts

Subscribe

Summary

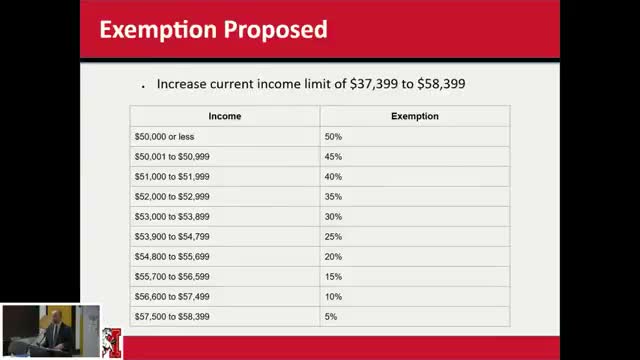

After a public hearing, the Mineola Union Free School District Board on Dec. 18 adopted Resolution 52 to raise the school-tax income threshold for the senior 50% exemption from $37,399 to $58,399; the town estimates about 59 additional households will qualify for the full exemption, shifting an average $22 increase to other Class 1 homeowners.

The Mineola Union Free School District Board of Education voted Dec. 18 to adopt Resolution 52, approving a sliding-income schedule that raises the income ceiling for the district’s senior real-property tax exemption from $37,399 to $58,399.

Assistant Superintendent Will Herman presented the Town of North Hempstead’s proposal in a public-hearing format and walked trustees through eligibility rules — applicants must be at least 65, own the home at least one year and use it as their primary residence — and what the town counts as income. "What the Town of North Hempstead is proposing for the district's consideration is increasing that limit to $58,399," Herman said, adding the town worked with the Nassau County Comptroller’s office to prepare the impact estimates.

Town estimates cited by the district project about 59 additional households would become fully exempt at the 50% level, increasing the number of full exemptions from 118 to roughly 177. Herman said the change would not reduce the overall tax burden for the community but would shift it inside Class 1 (residential homeowners). The town’s analysis projects an average $22 increase on the school-tax bill for other Class 1 homeowners if the board recognizes the change before Jan. 2, 2026, in time for the 2026–27 school-tax year.

Board members asked procedural and policy questions during the hearing. Herman confirmed the exemption requires an annual application to the town and that, if recognized by the district, the higher income threshold would remain in place until the board later reconsidered it. Trustees also clarified that certain receipts — for example, inheritances and Supplemental Security Income — are excluded from income for this exemption, while Social Security counts as income under the town’s rules.

After the presentation and a period for board clarifications, Trustee Margaret Ballentine moved to adopt Resolution 52; the motion was seconded and approved by voice vote. The resolution invokes state real-property tax law to allow school districts to adopt a sliding-scale exemption and directs the exemption to take effect in the 2026–27 tax year if recognized in time.

The board did not record a roll-call vote in the public record; the motion passed by voice and the district clerk announced that Resolution 52 "passes." The board also noted that town and county shares of property taxes are outside the district’s discretion and that the hearing addressed only the school-tax portion.

What’s next: The district will publish the resolution text and the town will administer individual applications; any family interested in the exemption must apply to the Town of North Hempstead under the rules described by Herman.

Resolution details and authorities cited in the meeting include section 467 of the Real Property Tax Law and the district’s Board Policy 1510 on public comments and meeting conduct.