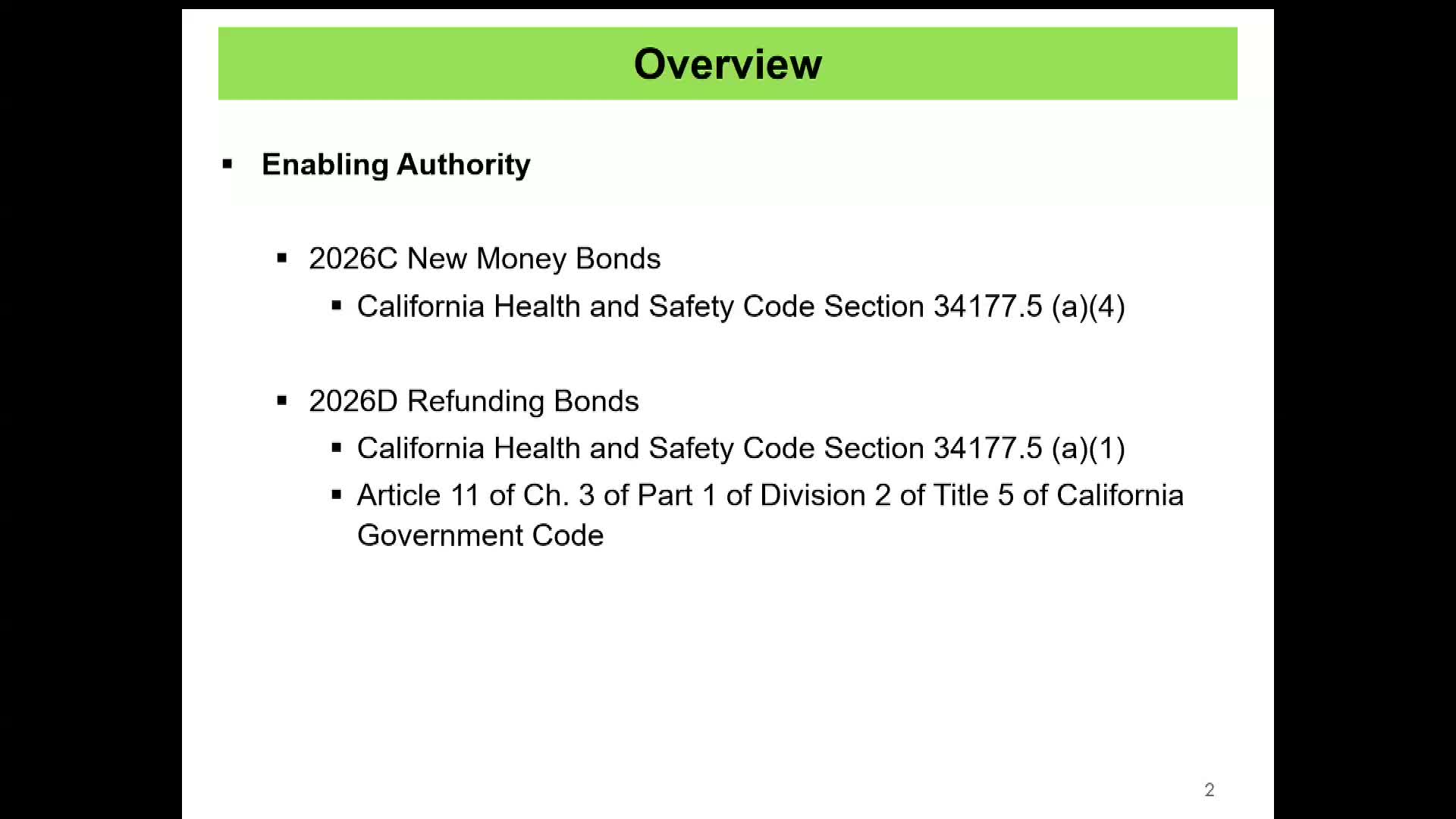

Commission and Financing Authority approve up to $48M in new bonds and $170M refunding for Mission Bay South

Loading...

Summary

On Jan. 6 the San Francisco Commission on Community Investment and Infrastructure and its Financing Authority authorized issuance of two bond series — up to $48 million in new-money tax-allocation bonds and up to $170 million in refunding bonds — to reimburse developer infrastructure in Mission Bay South and lock in projected debt-service savings.

The San Francisco Commission on Community Investment and Infrastructure on Jan. 6 authorized the issuance of up to $48 million in new-money tax-allocation bonds and up to $170 million in refunding tax-allocation bonds to fund and refinance infrastructure in the Mission Bay South redevelopment area. The commission approved the action by roll call and the separate Financing Authority later approved the negotiated-sale step needed for part of the transaction.

The bond package would reimburse the developer for completed but not yet city-accepted infrastructure in Mission Bay South and refund earlier OCII bonds to produce interest savings. "It looks like we're going to be saving nearly $15,000,000 over the term of the bonds," Vice Chair Miller said during the discussion. OCII staff estimated annual debt service would fall from about $11.9 million to about $11.1 million, producing roughly $800,000 in annual savings and an estimated $14.8 million total life-of-bonds savings through Aug. 1, 2043, based on assumptions in the municipal-adviser exhibit.

Why it matters: the 2026 C series is proposed as new-money tax-allocation bonds (not to exceed $48,000,000) to reimburse developer costs for specified Mission Bay South infrastructure (parks, stormwater pump station No. 3, Bridgeview Way mid-block, the Mission Creek extension and a school play yard). The 2026 D series (refunding, not to exceed $170,000,000) would refund OCII series 2014A, 2016B and 2016C to lock in savings at lower market rates. Nick Jones, presenting for OCII finance, said the refunding assumes an estimated interest rate of about 4.5% versus an assumed current rate of about 5% on refunded bonds.

Transaction mechanics and next steps: staff described the exhibits to the resolution (a third supplemental indenture of trust, irrevocable refunding instructions and a bond purchase contract). OCII reported it selected Morgan Stanley as lead underwriter, with Stifel and Wells Fargo as co-managers, after an RFP process. The oversight board is scheduled to consider the issuance next week; OCII will then submit materials to the California Department of Finance, which has up to 65 days to review. OCII is targeting bond pricing in August and a closing in September, at which point project funds would be received and refunded bonds paid off.

Questions and dissent: Commissioner Lim pressed staff on small-business-enterprise (SBE) performance for a contractor on the school play-yard portion of the project, saying she would not support reimbursing the developer for that playground item if contracting goals were not met. Staff responded that the contracting requirement on that work was framed as the contractor's "best faith efforts," that the school-district pass-through arrangement complicates direct enforcement in this forum, and that OCII will provide a small-business contracting performance update later this year. Mark Slutskin, deputy director, clarified that "unaccepted infrastructure" refers to work that has been built but not yet formally accepted by the city through Department of Public Works inspections and legislative action.

Public comment: Francisco DeCosta, representing Bayview residents in public comment, said community leaders had not been sufficiently involved in past allocations and urged greater outreach and accountability. "We the people, we, the citizens, we, the constituents of the Bayview, have never seen this person before," DeCosta said, arguing that distribution of funds had not been fair to the Bayview.

Outcome: The commission voted to approve item 5B. Later the Financing Authority convened, elected officers, and approved the authority-level actions necessary to permit a negotiated sale; that financing-authority vote passed with three ayes and one abstention. The oversight-board review and Department of Finance review remain required before the bonds are priced and sold.